The goal of any retirement solution is to support long‑term retirement income outcomes for participants. That principle has anchored this series (see “Series in brief” sidebar) from the outset, challenging the industry to reconsider default assumptions and evaluate private markets in defined contribution (DC) plans through a disciplined, participant‑first framework.

With the release of the Department of Labor’s (DOL) proposed updates to “Fiduciary Duties in Selecting Designated Investment Alternatives” (the “Investment Selection Rule”)i, the evaluative framework governing investment selection in participant‑directed DC plans has been clarified. The proposal addresses how fiduciaries assess designated investment alternatives—the investment options selected by plan fiduciaries and made available to participants—by reaffirming a process‑based approach grounded in ERISA’s long‑standing principles of prudence, context, and portfolio‑level analysis. In this final paper, we examine what the proposed guidance does and does not change, why it is rooted in first principles of fiduciary law and likely to endure across administrations, and how it reframes fiduciary evaluation of investment options in a modern DC environment.

Over the past two decades, fiduciaries overseeing DC plans have had to balance a range of considerations, including regulatory uncertainty, operational constraints, participant outcomes, and the growing influence of a small number of high‑profile fiduciary cases. In practice, these forces often encouraged a preference for investment choices perceived as defensible in a litigation-conscious environment, sometimes at the expense of broader diversification or long‑term outcomes. The proposed rule provides important clarity on how those tradeoffs should be evaluated going forward.

Against that backdrop, the most important question is how the proposed Investment Selection Rule clarifies fiduciary evaluation in practice. Significantly, the proposal does not introduce new fiduciary duties, mandate specific investments, or endorse particular asset classes. Instead, it articulates a process‑based, asset‑neutral framework for evaluating designated investment alternatives grounded in ERISA’s long‑standing principles of prudence, context, and portfolio‑level analysis. With that evaluative framework established (summarized in the Investment Selection Rule summary sidebar), the key issue becomes what the proposed guidance does and does not change for fiduciaries navigating today’s DC environment.

Summary of the Investment Selection Rule

Context from the Executive Order (EO) on “Democratizing Access to Alternative Assets for 401(k) Investors”ii

The EO emphasized reducing litigation risk by directing the development of a clear, process‑based framework to promote consistent application of ERISA principles and reduce ambiguity in investment evaluation.

- Defines alternative investments broadly, including but not limited to private equity, private credit, and real assets.

- Directs the DOL to review and clarify fiduciary processes related to investment selection in retirement plans.

- Encourages coordination with other regulatory agencies to promote consistency in guidance.

Key fiduciary considerations emphasized in the proposal

The proposed rule establishes a process‑based safe harbor: when fiduciaries follow a reasonable, well‑documented decision‑making process, prudence is assessed at the time of the decision, not in hindsight, using a non‑exhaustive set of considerations.

- Performance: Evaluate expected risk‑adjusted returns over an appropriate time horizon, relative to comparable alternatives and in the context of participant outcomes.

- Fees and expenses: Assess whether fees are reasonable in relation to expected returns, services provided, and diversification benefits, rather than focusing on cost in isolation.

- Liquidity: Determine whether liquidity aligns with participant‑ and plan‑level needs, recognizing that certain liquidity constraints may be prudent if understood, managed, and justified.

- Valuation: Ensure investments can be valued accurately and on a timely basis using robust, independent, and well‑documented methodologies.

- Benchmarking: Use benchmarks that reflect an investment’s strategy, risks, and objectives; custom or composite benchmarks may be appropriate where standard comparisons are insufficient.

- Complexity and expertise: Consider whether fiduciaries have, or can reasonably obtain, the expertise necessary to evaluate and monitor the investment prudently.

Sources: White House, Executive Order on Democratizing Access to Alternative Assets for 401(k) Investors (August 2025); U.S. Department of Labor, “Fiduciary Duties in Selecting Designated Investment Alternatives” (proposed).

Why this guidance was needed

To interpret the Investment Selection Rule appropriately, it is important to understand the environment in which fiduciaries have been operating. The guidance does not emerge in a vacuum; it responds to structural, legal, and behavioral dynamics that shaped how investment decisions were made in practice, often in ways that prioritized defensibility over long‑term outcomes.

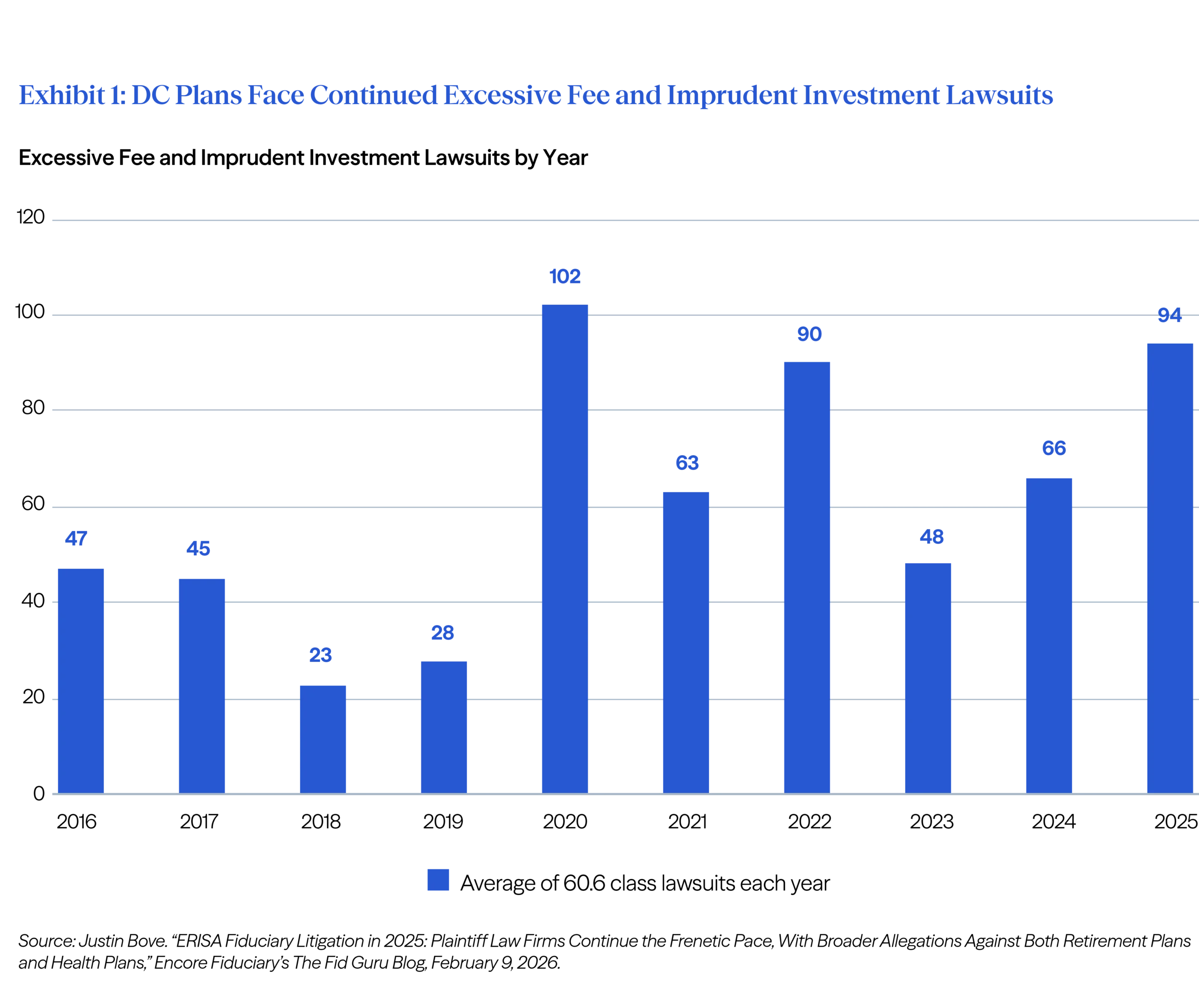

Over the past two decades, litigation risk—or the perception of litigation risk—has been a powerful factor behind constraining innovation in DC plan design. Since 2016, plan sponsors have faced hundreds of excessive fee and imprudent investment lawsuits, with the majority tied to 401(k) plans (Exhibit 1).iii Because those cases are highly visible and often costly, plan sponsors openly acknowledge this litigation risk has had a negative impact on plan innovation and design.iv

Empirical research reinforces this dynamic. An analysis of more than 35,000 employee retirement plans, representing over $5 trillion in assets, indicates that plans most exposed to ERISA litigation are 2%–3% less likely to include a given asset class in their investment menus.v That same research estimates that excluding these asset classes reduced participants’ retirement wealth by 9%–14%. Together, these findings suggest that a system designed to protect participants may have unintentionally constrained the long‑term outcomes it was intended to support.

Empirical research reinforces this dynamic. An analysis of more than 35,000 employee retirement plans, representing over $5 trillion in assets, indicates that plans most exposed to ERISA litigation are 2%–3% less likely to include a given asset class in their investment menus.v That same research estimates that excluding these asset classes reduced participants’ retirement wealth by 9%–14%. Together, these findings suggest that a system designed to protect participants may have unintentionally constrained the long‑term outcomes it was intended to support.

At the same time, the structure and governance of DC plans were evolving in ways that challenged prevailing default approaches. The modern DC landscape was fundamentally reshaped by the Pension Protection Act (PPA) of 2006.vi Prior to the PPA, auto‑enrollment and diversified default options were uncommon, and many plans defaulted participants into capital‑preservation vehicles due to concerns about fiduciary exposure if participants experienced losses.

By designating target‑date funds (TDFs) as qualified default investment alternatives (QDIAs) and encouraging auto‑enrollment, the PPA marked a shift away from defaults shaped primarily by perceived fiduciary defensibility toward approaches grounded in diversification, professional management, and long‑term outcomes.vii Although QDIAs are now a common category of designated investment alternatives used when participants do not make an affirmative election, their adoption was initially controversial. Critics argued that defaulting participants into professionally managed, equity‑exposed portfolios reduced individual choice, imposed one‑size‑fits‑all solutions, and exposed participants—and fiduciaries—to the possibility of market losses.

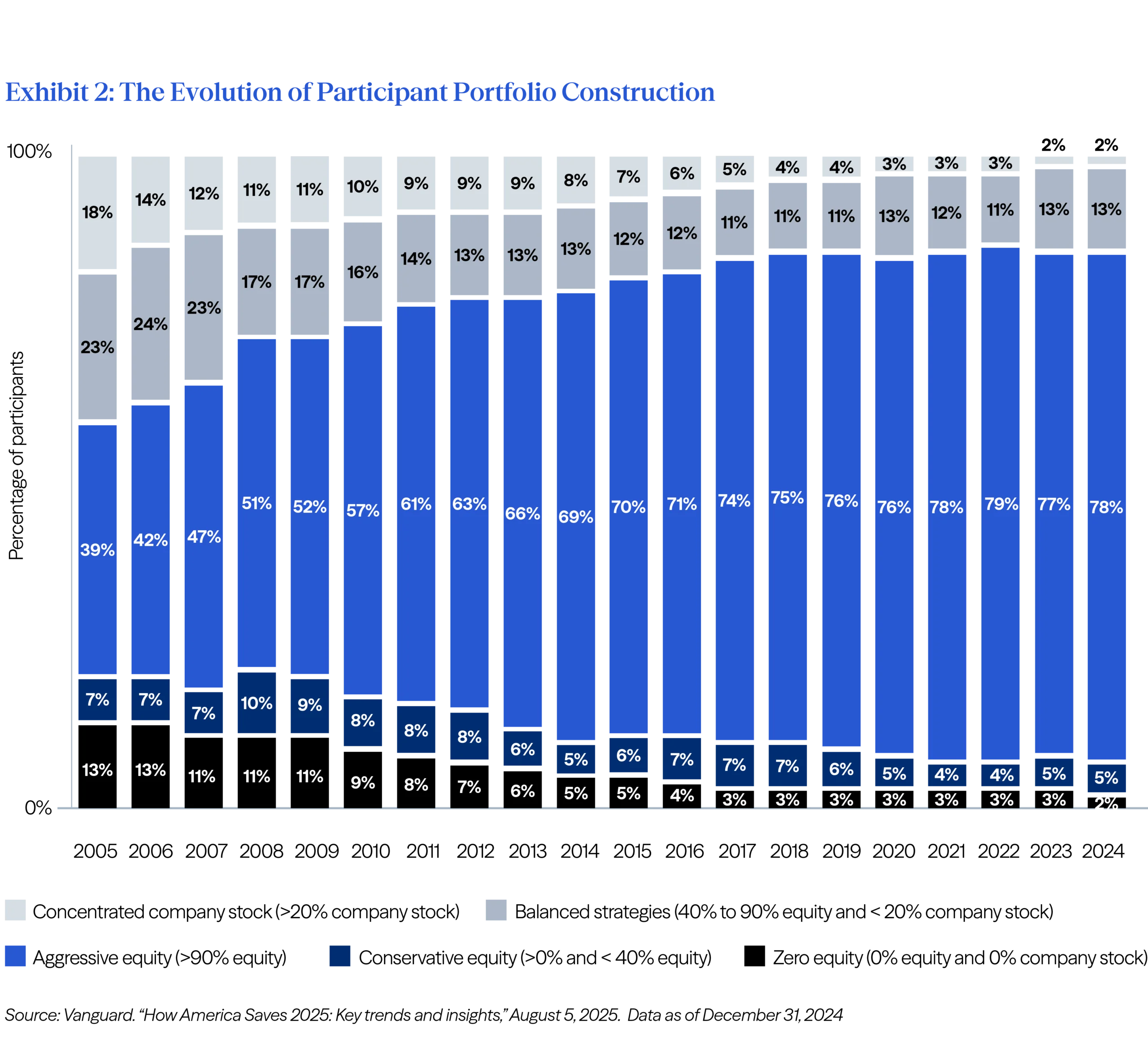

With the benefit of hindsight, those concerns have largely proved unfounded. As illustrated in Exhibit 2, nearly half of DC participants in 2005 were invested either in highly concentrated company stock or in very conservative fixed income and money market funds—allocations that exposed participants to either outsized risk or chronically low returns.viii ix By 2024, these high‑risk and low‑return allocations had moved to the margins, while nearly 80% of participants were invested in diversified, balanced strategies. This shift reflects not a reduction in choice, but an evolution in plan design that better aligns investment structure, governance, and participant outcomes.

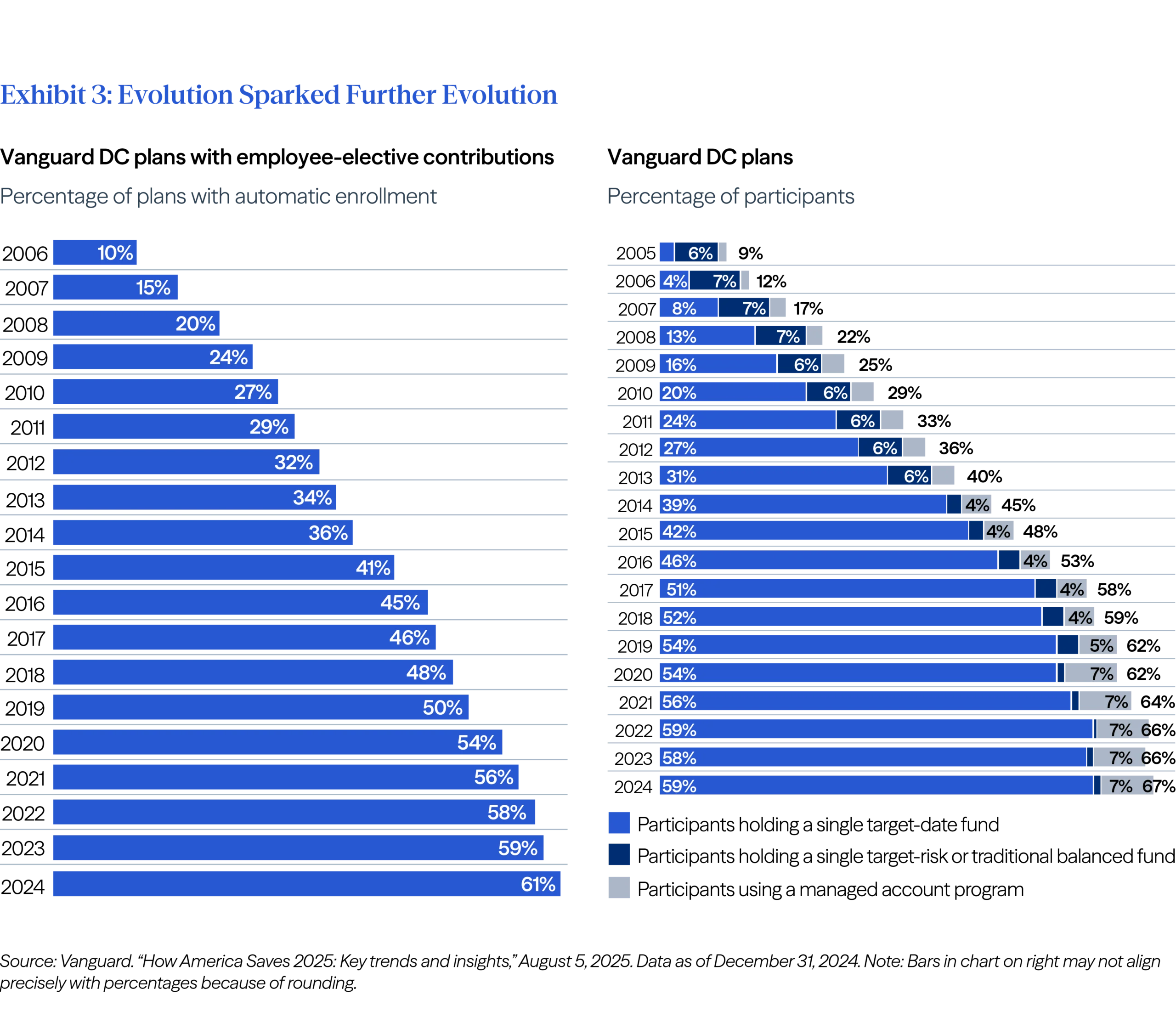

Over the same period, DC plan features continued to evolve. Auto‑enrollment expanded significantly (Exhibit 3, left), professionally managed accounts gained traction (Exhibit 3, right), QDIAs broadened to include collective investment trusts (CITs), auto‑enrollment gave rise to auto‑escalation, and plan lineups expanded to include additional tools such as self‑directed brokerage windows. These developments reflect a DC system that is materially more sophisticated, operationally and from a governance perspective, than it was two decades ago.

Over the same period, DC plan features continued to evolve. Auto‑enrollment expanded significantly (Exhibit 3, left), professionally managed accounts gained traction (Exhibit 3, right), QDIAs broadened to include collective investment trusts (CITs), auto‑enrollment gave rise to auto‑escalation, and plan lineups expanded to include additional tools such as self‑directed brokerage windows. These developments reflect a DC system that is materially more sophisticated, operationally and from a governance perspective, than it was two decades ago.

This evolution has not occurred at the expense of fiduciary oversight, though. Today’s DC plans are better equipped to evaluate, implement, and monitor a wider range of investment structures than they were pre‑PPA. Fiduciaries continue to assess plan demographics, governance capabilities, and participant needs when determining whether particular investment approaches are appropriate. In some cases, zero allocation to some strategies may be the right choice, but it cannot be the default based on assumption of complexity alone.

This evolution has not occurred at the expense of fiduciary oversight, though. Today’s DC plans are better equipped to evaluate, implement, and monitor a wider range of investment structures than they were pre‑PPA. Fiduciaries continue to assess plan demographics, governance capabilities, and participant needs when determining whether particular investment approaches are appropriate. In some cases, zero allocation to some strategies may be the right choice, but it cannot be the default based on assumption of complexity alone.

Participant expectations have also evolved alongside these structural changes. While a “set‑it‑and‑forget‑it” approach remains appropriate for many participants, it no longer reflects the full range of behaviors observed in today’s DC system. Participants are often described as falling into one of two categories—those who want investment decisions made for them and those who prefer to manage their own portfolios—but in practice, those preferences are not static.

As participants age, balances grow, household finances become more complex, and confidence increases; investment behavior often evolves. Many participants who begin their careers invested entirely in target‑date funds gradually supplement that default allocation with additional “do‑it‑yourself” choices, including core menu options or brokerage windows, while still retaining a professionally managed foundation. Investment needs and engagement tend to change along the glidepath of an investor’s lifecycle, rather than following a single, permanent path.

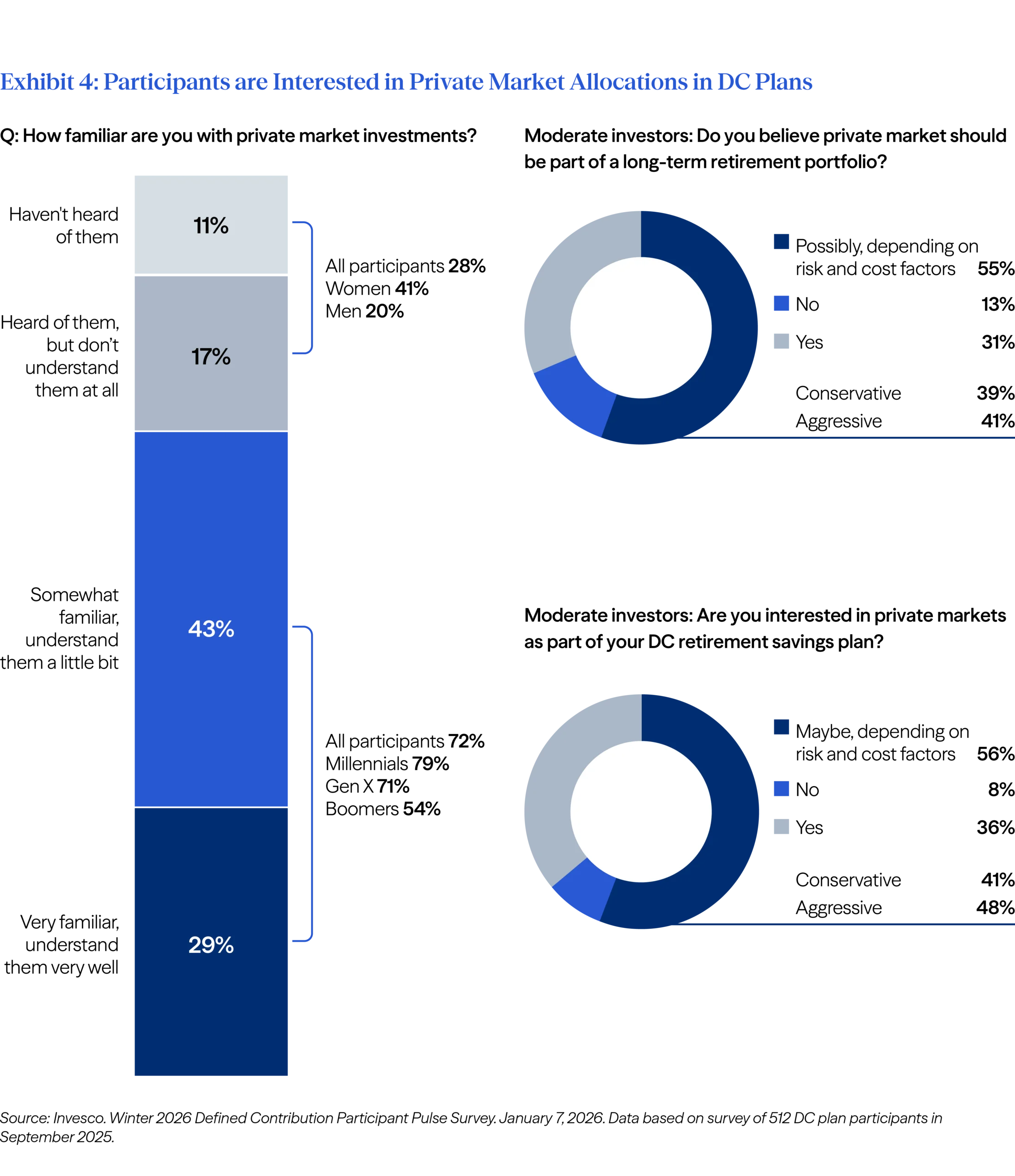

Recent survey data reflect this growing desire for involvement. More than 70% of DC participants want some level of involvement in retirement investment decisions.x Many— particularly Millennials and Gen X — report familiarity with private market investments and believe they should at least be considered within long‑horizon retirement portfolios (Exhibit 4).

These preferences are consistent with broader research on retirement outcomes. Studies examining “401(k) millionaires,” alongside coverage of record‑high participant balances, highlight a consistent set of behaviors: early and sustained participation, relatively high contribution rates (often in the low‑ to mid‑teens), and diversified asset allocations maintained over long horizons.xi At the same time, over half of recent retirees express regret about their accumulation phase strategy, citing not starting early and not contributing enough to retirement as the two biggest reasons for their sentiment.xii

These preferences are consistent with broader research on retirement outcomes. Studies examining “401(k) millionaires,” alongside coverage of record‑high participant balances, highlight a consistent set of behaviors: early and sustained participation, relatively high contribution rates (often in the low‑ to mid‑teens), and diversified asset allocations maintained over long horizons.xi At the same time, over half of recent retirees express regret about their accumulation phase strategy, citing not starting early and not contributing enough to retirement as the two biggest reasons for their sentiment.xii

Taken together, these dynamics created the need for clearer guidance on how fiduciaries should apply ERISA’s principles in a modern context, setting the stage for the clarification provided by the Investment Selection Rule.

A return to first principles

The Investment Selection Rule fits squarely within the broader evolution of DC plans. The PPA recognized that defaults, diversification, and professional management could improve participant outcomes when thoughtfully implemented. The proposed rule builds on that foundation by clarifying how fiduciaries should evaluate increasingly sophisticated investment solutions within participant‑directed plans. It reflects a DC framework that has moved beyond simple choice architecture toward one centered on outcomes, grounded in ERISA’s core principles of prudence and fiduciary discretion.

At its foundation, ERISA has always emphasized process over prediction. It does not demand risk avoidance or market foresight; it requires a prudent, well‑documented decision‑making process grounded in the facts and circumstances of each plan. The Investment Selection Rule reinforces this approach by clarifying how those principles apply as DC plans, investment vehicles, and participant needs have evolved.

A defining feature of the proposed framework is its asset neutrality. The factors emphasized in the rule—expected risk‑adjusted returns over appropriate time horizons, fees in relation to value, liquidity aligned with plan needs, valuation, benchmarking, and fiduciary expertise—apply broadly to designated investment alternatives, including asset‑allocation vehicles such as TDFs. This aligns regulatory guidance with how fiduciaries already evaluate widely used DC structures and extends that same evaluative discipline across a broader set of potential investments.

The rule also moves fiduciary evaluation away from assessing investment characteristics in isolation. As DC plans have shifted from self‑directed menus toward professionally managed portfolios, evaluation has increasingly occurred at the portfolio level, where diversification, time horizon, liquidity management, and participant behavior intersect. By framing prudence in context rather than relying on categorical assumptions about complexity, structure or cost, the Investment Selection Rule brings regulatory clarity to how modern DC plans are designed and managed.

The durability of this guidance stems from that same first‑principles approach. Rather than relying on informal statements or narrow interpretations, the DOL has proposed a formal notice‑and‑comment regulation anchored in ERISA’s statutory text and longstanding interpretive history. By emphasizing prudence, process, and fiduciary discretion, rather than endorsing or discouraging particular investments, the rule establishes a framework that is both flexible and resilient. Meaningful reversal would likely involve a departure from ERISA’s foundational concepts, rather than a change in policy emphasis alone.

Applying the framework

Across this series, we have argued for a more deliberate, outcome‑oriented approach to DC plan design—one that moves beyond default assumptions and evaluates investment solutions through the lens of participant needs, fiduciary process, and long‑term retirement outcomes. Each installment addressed a different dimension of that challenge: questioning zero allocation as a default, clarifying the role of liquidity, reinforcing the centrality of fiduciary process, and now situating the Investment Selection Rule within the broader evolution of the DC system.

The proposed guidance brings needed clarity to how fiduciaries should approach investment evaluation in practice. It does not mandate change, nor does it prescribe specific solutions. Instead, it articulates a principles‑based, asset‑neutral framework that aligns regulatory expectations with how modern DC plans are designed, governed, and managed. By grounding fiduciary evaluation in process, documentation, and portfolio context, the rule reinforces long‑standing ERISA principles while providing greater confidence for fiduciaries navigating an increasingly complex investment landscape.

Importantly, this clarification arrives at a moment when DC plans are better equipped—operationally, structurally, and from a governance perspective—to apply it thoughtfully. The question for fiduciaries is no longer whether complexity should be avoided by default, but how different investment approaches should be evaluated in light of plan design, participant demographics, and long‑term objectives. In some cases, maintaining existing structures may remain appropriate. In others, thoughtful change may be warranted. The proposed framework supports both outcomes, provided the decision is grounded in a prudent and well‑documented process.

As the DOL’s proposal moves through the notice‑and‑comment process, fiduciaries and industry participants have an opportunity to engage constructively, drawing on experience, evidence, and first principles to help shape guidance that reflects the realities of today’s DC system. With greater clarity now in place, the conversation can move from whether fiduciaries can engage to how they should engage. What remains is a collective challenge: to apply education, diligence, and prudent judgment in a way that meaningfully improves long‑term retirement outcomes for participants.

Series in brief

- Part 1: Zero Is Not the Answer

We challenged the assumption that zero allocation is inherently safer or more prudent, reframing decision-making around process rather than avoidance. - Part 2: Rethinking Private Market Liquidity in DC Plans

We addressed common structural concerns (liquidity, valuation, fees, and complexity) and how DC plans evaluate and manage these factors in practice. - Part 3: Applying Fiduciary Principles to Private Market Allocations in DC Plans

We reframed fiduciary duty around disciplined process, documentation, and portfolio-level evaluation, emphasizing context-specific judgment over categorical avoidance.

- See: U.S. Department of Labor, Employee Benefits Security Administration (EBSA), Fiduciary Duties in Selecting Designated Investment Alternatives,” March 2026. Available at: Federal Register :: Fiduciary Duties in Selecting Designated Investment Alternatives.

- See: White House, “Democratizing Access to Alternative Assets for 401(k) Investors,” Executive Order, August 2025. Available at: Democratizing Access to Alternative Assets for 401(K) Investors – The White House.

- Note: Of the 155 ERISA fiduciary class lawsuits in 2025, 98 were focused on DC plans. Source: Justin Bove. “ERISA Fiduciary Litigation in 2025: Plaintiff Law Firms Continue the Frenetic Pace, With Broader Allegations Against Both Retirement Plans and Health Plans,” Encore Fiduciary’s The Fid Guru Blog, February 9, 2026.

- Source: Ted Godbout. “ERISA Litigation ‘Powerful Disincentive’ Against Retirement Plan Innovation,” National Association of Plan Sponsors. December 2, 2025.

- ibid. Note: Gropper’s estimate is based on a loss in utility induced by limited choice and assumes plan participants invest on a mean-variance efficient frontier.

- See: U.S. Department of Labor, Employee Benefits Security Administration (EBSA). Pension Protection Act of 2006.

- In 2000, roughly US$8 billion in assets were invested in TDFs. That number grew to around US$130B at the eve of the PPA but accounted for only ~5% of 401(k) assets. At the end of 2024, over US$4T was invested in TDFs and were offered by 98% of funds. Sources: ICI. Quick Facts on Target Date Fund Use in Retirement Plans. December 8, 2025. Data as of December 31, 2024; ICI. “The U.S. Retirement Market, Third Quarter 2025,” (January) Quarterly Data Tables, www.ici.org/statistical-report/ret_25_q3_data.xls. All data as of September 20, 2025; Vanguard. How America Saves 2025. Data as of December 31, 2024, and based on Vanguard DC plan participants.

- For data on the pitfalls of overallocation to employee stock, see: Brennan, M.J., and W.N. Torous. (1999) Individual Decision Making and Investor Welfare, Economic Notes, 28, 119-143; Benartzi, S. (2001). Excessive Extrapolation and the Allocation of 401(k) Accounts to Company Stock. Journal of Finance, 56, 1747-1764.

- Source: Jonathan Reuter. Plan Design and Participant Behavior in Defined Contribution Retirement Plans: Past, Present, and Future. Pension Research Council Working Paper, PRC WP2024-16. October 3, 2024.

- Source: Invesco. Winter 2026 Defined Contribution Participant Pulse Survey. January 7, 2026. Data based on survey of 512 DC plan participants in September 2025.

- See, for example: David Blanchett and Drew Carrington. Why Qualified Retirement Assets Should be Included in the “Accredited Investor” Definition. Retirement Research Center. August 2025; Empower Retirement. “Becoming the 401(k) millionaire next door,” The Currency, November 7, 2025; Jessica Hall. “The number of 401(k) millionaires just hit a record high: ‘People are staying the course,’” MarketWatch, November 22, 2025.

- Source: Nationwide Retirement Institute. Eleventh Annual Advisor Authority Study. February 2026. Note: The research was conducted online in the U.S. by The Harris Poll on behalf of Nationwide among 510 advisors and financial professionals and 2007 investors age 18+ with investable assets (IA) of $10K+. Advisors and financial professionals included 267 RIAs, 210 broker-dealers, 106 wirehouse and 40 other financial professionals. Among the investors, there were 500 Mass Affluent (IA of $100K-$499K), 487 Emerging High Net Worth (IA of $500K-$999K), 307 High Net Worth (IA of $1M-$4.99M) and 208 Ultra High Net Worth (IA of $5M+), as well as 505 investors with $10K to less than $100K investable assets (“Less affluent”). Investors included a subset of 257 “pre-retirees” age 55-65 who are not retired. The survey was conducted 8/19- 9/2/2025. Among the investors, there were 180 recent retirees (those who retired 5 years ago or less) and 274 longer term retirees (those who retired more than 5 years ago).

Important Information

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a

substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Market LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2026 Institutional Capital Network, Inc. All Rights Reserved.