The markets have an obsession right now – the recession obsession. And for most market observers, the question is not if it’s coming, but when. There doesn’t seem to be a strong consensus on this. The latest release of 2023 outlooks shows that some anticipate a recession in the second half of 2023 or sooner and yet others say we might have to wait till 2024.1

Whether it ends up being called a recession or not, the slowdown we’ve all been waiting for might happen in the next two quarters. This means that the first half of 2023 might be the entry point back into risk(ier) assets.

1. The recipe for a slowdown is ready to be fully baked. Typically, there is a period that passes when the Fed stops hiking rates, yield curve inverts, and recession onsets (if it does) around 15 months after.2 But then again, the Fed generally doesn’t hike rates in a weakening economy. What might make it different this time around is that the Fed has been hiking at an aggressive pace since the summer (+75bps per meeting), all while the economy, as measured by the manufacturing, service, and housing slowdown, has been weakening.3

In fact, we did print two consecutive quarters of negative GDP growth in 2022 already.4 Looking ahead, consensus expects GDP in the first and second quarter of 2023 to be slightly negative at -0.1%,5 while 1-year recession probabilities continue to be elevated on most metrics (Exhibit 1).6 Jobless claims have started to inch up, tech layoffs are starting to accumulate, and other industries may follow suit.7 And yet the Fed still plans to hike the fed funds rate up to 5%, further restricting the economy. All in, the economy should be poised to slow meaningfully in the months ahead, given all this pressure.

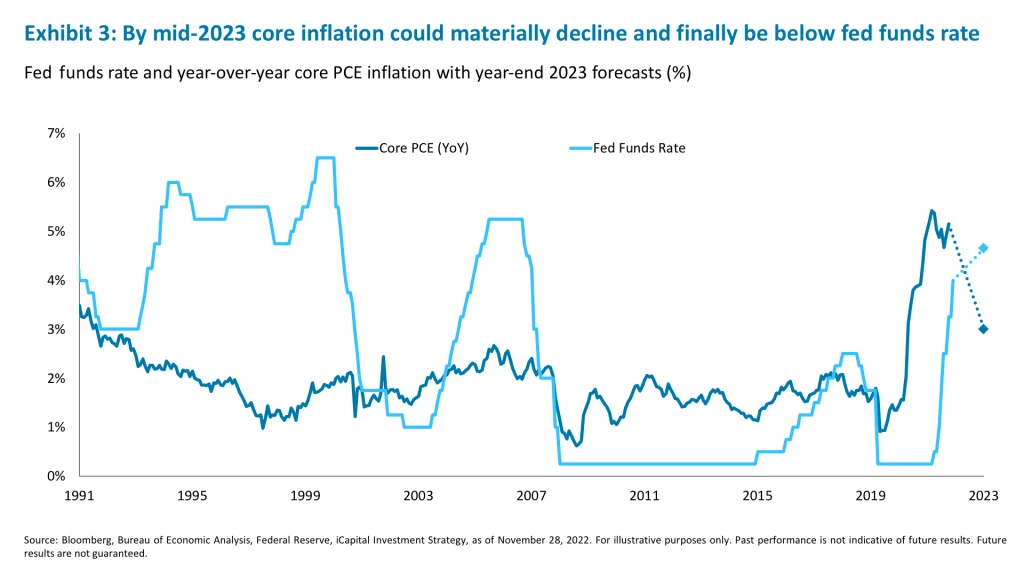

2. The silver lining is that this economic slowdown will likely bring inflation under control. More and more measures of inflation are already showing that it may finally be turning a corner. The supply chain bottlenecks are gone (latest China news non-withstanding). The retail markdowns were meaningful this past weekend. Food and fuel prices have eased up and durable goods CPI is clearly off its peak.8 As a result, the latest 3-month annualized CPI inflation rate has come down considerably and is currently at 3.8% compared to the peak of 10.8% seen in the first half of 2022.9 Of course, service inflation is stickier, but there are signs that shelter and wage inflation may be easing up as well. The Zillow U.S. rent inflation index increased a modest 0.3% month-over-month in October 2022 versus the 2% month-over-month clip from a year ago.10 There is talk of concessions again amongst residential REIT operators. Intentions to raise wages have moderated. And as job openings and the pace of job creation decline, this should slow wage increases as well. As a result, core Personal Consumption Expenditures (“PCE”) inflation is expected to fall to 3.8% by the end of the second quarter of 2023, from 4.8% in the fourth quarter of 2022.11 This will ease pressures on consumers, and also the Fed.

2. The silver lining is that this economic slowdown will likely bring inflation under control. More and more measures of inflation are already showing that it may finally be turning a corner. The supply chain bottlenecks are gone (latest China news non-withstanding). The retail markdowns were meaningful this past weekend. Food and fuel prices have eased up and durable goods CPI is clearly off its peak.8 As a result, the latest 3-month annualized CPI inflation rate has come down considerably and is currently at 3.8% compared to the peak of 10.8% seen in the first half of 2022.9 Of course, service inflation is stickier, but there are signs that shelter and wage inflation may be easing up as well. The Zillow U.S. rent inflation index increased a modest 0.3% month-over-month in October 2022 versus the 2% month-over-month clip from a year ago.10 There is talk of concessions again amongst residential REIT operators. Intentions to raise wages have moderated. And as job openings and the pace of job creation decline, this should slow wage increases as well. As a result, core Personal Consumption Expenditures (“PCE”) inflation is expected to fall to 3.8% by the end of the second quarter of 2023, from 4.8% in the fourth quarter of 2022.11 This will ease pressures on consumers, and also the Fed.

3. This fall in inflation will allow the Fed wiggle room to cut if needed. The Fed is finally on track to get the fed funds rate in line with core inflation. But if core PCE inflation falls as expected to 3.8% by the middle of next year, and rates are still at 5%, a gap will open where nominal rates are above inflation.12 This is the point at which – along with weakness in economic activity – the Fed might be justified to finally talk about cutting rates.

What does this all mean for markets?

What does this all mean for markets?

We would expect the first quarter of next year to be the toughest for markets, with growth slowing or at a standstill while the Fed may still be hiking. Elsewhere, in China, more near-term mobility restrictions are likely given rising COVID cases and escalating tensions.

The second quarter may still be lackluster as growth is weak in the U.S. and the Fed is holding rates to 5%, but perhaps towards the tail end of the second quarter of 2023, as inflation subsides, conversations about rate cuts are likely to heat up, and that would-be market positive. We should also have better news elsewhere – re-opening in China is our base case for the second quarter of 2023. We believe an eventual exit from zero-COVID in 2023 is the path of least resistance given the human toll and economic toll of current COVID restrictions. This will require medical preparations such as more treatments, more vaccines, and less testing, but recent announcements suggest that the path to phasing out the stringent restrictions is in the making. If realized, China re-opening impulse could help support global economic growth.

Thus, the first half of 2023 is likely to present a buying opportunity for investors looking to the second half of 2023 and beyond.

Playbook for a Patient Investor

1. Start to accumulate a position in long-term Treasuries (or munis). As growth slows and inflation eases, there should be much less duration risk ahead. Recent flows data shows that investors are already buying fixed income as it recently saw its largest inflows in 15 weeks.13

2. Patience is a virtue in a market where you can get paid to wait. We like a barbell of short-duration U.S. Treasuries/munis and credits like high yield and private credit. Stick with high quality dividend payers. Cash is an option too. More on this here: iCapital Market Pulse: We have a ways to go, but the next stop is 5%

3. Buy optionality for easing inflation in 2023. Within equities, the consumer services and retail industries should benefit given that the real wage growth picture is likely to improve on the back of easing inflation. Additionally, the semiconductor space has tended to outperform the broader market during periods of high and falling (easing) inflation.14 Given the reset in their forward price-to-earnings (P/E) multiples and downward earnings revisions since the start of the year, we also view this sector as an inexpensive call option on a potential risk re-rating in the back half of 2023.

4. Buy optionality for China re-opening in 2023. The preferred way to position for this would be staying bullish energy equities. If China does begin to truly re-open in the second quarter of 202315, the country’s traffic congestion, airline bookings and flights, and overall mobility should recovery meaningfully, supporting more demand for oil in an otherwise constrained supply environment. We note that despite the sell-off in Brent crude this month, energy equities have been outperforming the underlying commodity. We attribute this to the fact that investors are likely looking through the near-term weakness in China’s oil demand and looking forward to the re-opening. As a result, the 12-month forward strip on Brent is averaging roughly $84 – more than good enough given energy companies’ breakeven price on oil is around the $50 mark.16 At the same time, the energy sector pays a 4% dividend and has the lowest valuation within the S&P 500 – the average company’s NTM P/E is in the 24%-tile over a 5-year lookback period.17

1. Bloomberg, Bank of America, Goldman Sachs. JPMorgan, Morgan Stanley, iCapital Investment Strategy, as of November 29, 2022.

2. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

3. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

4. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

5. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

6. JPMorgan Research, as of November 28, 2022

7. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

8. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

9. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

10. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

11. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

12. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

13. BofA Research, EPFR, as of November 23, 2022.

14. BofA Research, as of November 23, 2022.

15. Bloomberg, Goldman Sachs, iCapital Investment Strategy, as of November 29, 2022.

16. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

17. Bloomberg, iCapital Investment Strategy, as of November 29, 2022.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by iCapital, Inc. (“iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer to sell, a solicitation of an offer to purchase or a recommendation of any interest in any fund or security. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation. This material does not intend to address the financial objectives, situation or specific needs of any individual investor. Alternative investments are complex, speculative investment vehicles and are not suitable for all investors.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2023 Institutional Capital Network, Inc. All Rights Reserved.