Key Takeaways

Capital markets activity, trade policy, and the path of U.S. Federal Reserve policy were the overarching inputs that went into our rating analysis. The second half of 2025 ended with more momentum than it started, with deal activity rebounding and exit volumes climbing. Overall, we remain constructive on select private equity and real assets strategies, while downgrading private credit to Neutral given lower base rates, rising BDC redemption pressure, and heightened focus on new deployment.

PRIVATE EQUITY

Exit activity re-accelerates

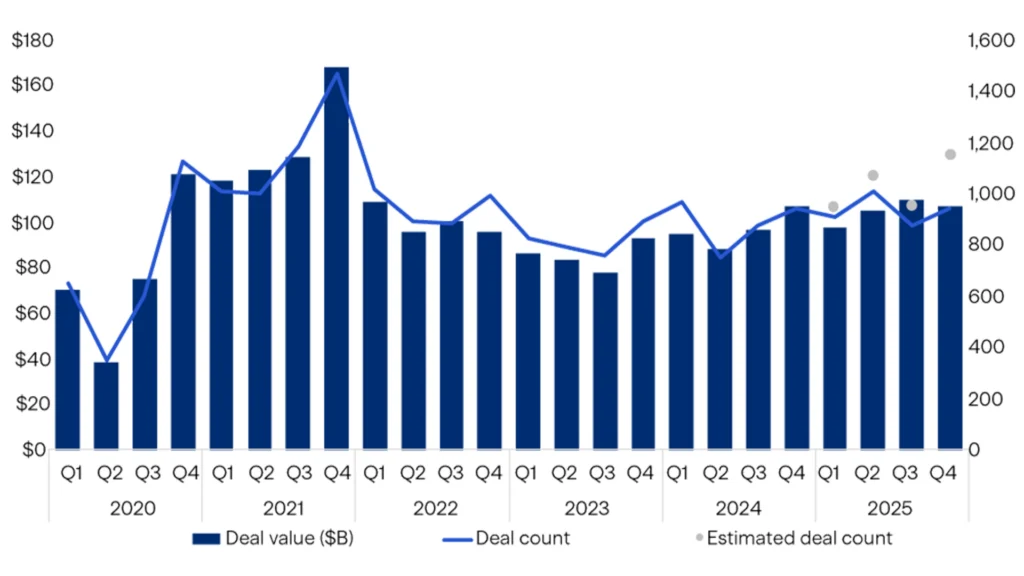

U.S. PE deal activity reached $1.2 trillion in 2025 — only the second time it has exceeded $1 trillion — with nearly 900 middle market transactions closing in Q3 alone2. Venture deal value hit $339 billion, the second-highest on record, with AI accounting for approximately 65% of all U.S. venture deal value.3

Deal Activity

U.S. Middle Market PE Deal Value and Activity

Source: PitchBook, 2025 Annual U.S. Middle Market Private Equity Report, as of March 13, 2026. For illustrative purposes only.

PRIVATE CREDIT

Mixed signals emerge

Private credit performance remained resilient, but lower base rates, spread compression, and rising BDC redemption pressure lead us to downgrade our outlook to Neutral. We believe lenders can still achieve attractive gross yields — a premium to high yield and investment grade credit — with default rates remaining in the 2–3% range.

REAL ASSETS

Structural tailwinds persist

Infrastructure

Infrastructure fundraising reached record highs in 2025, supported by digital transformation and energy transition themes, with electricity demand projected to increase 40% by 2035.

Real Estate

In Real Estate, Value-add Real Estate remains our top idea, with NOI growing faster than inflation over the past decade.

Hedge Funds

Versatility shines

Hedge funds saw over $116 billion in net inflows in 2025 — the most since 20076. A growing list of global market dislocations and monetary policy divergence creates a rich backdrop for multi-strategy, macro, and event-driven funds.

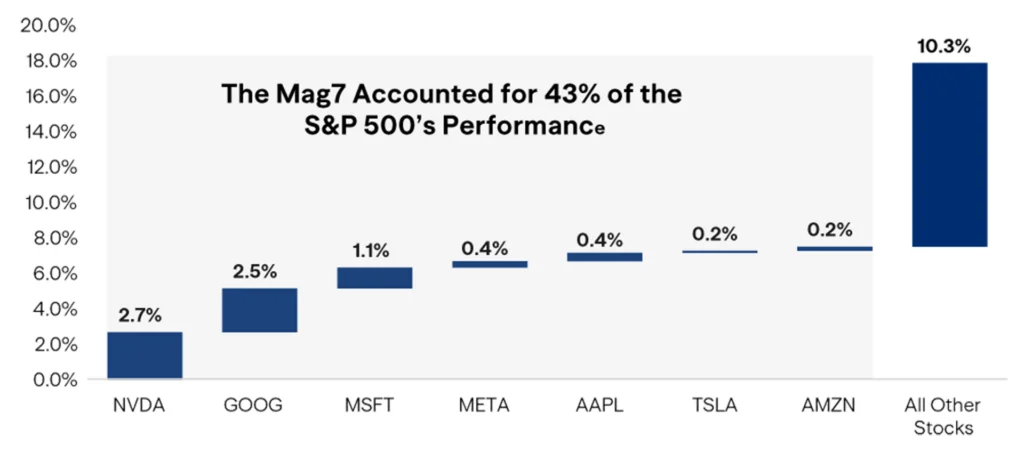

The S&P 500 Index is Heavily Weighted Towards a Small Number of Stocks

S&P 500 index return attribution (% data for CY 2025)

Source: Bloomberg, First Trust Advisors, February 2026. For illustrative purposes only. Past performance is not indicative of future results. Future results are not guaranteed.

Private Markets & Hedge Fund Strategy Ratings

1H 2026

Explanation of iCapital’s Ratings Framework

iCapital’s basis for assigning ratings is the research team’s view of how the investment strategy will perform over the next three years relative to its respective category. For this purpose, the “category” is the asset class associated with investment strategies for which the research team provides coverage. For example, a rating for Growth Equity is relative to other strategies within the Private Equity category.

Strategy ratings are reevaluated at least semiannually with an emphasis on whether the outlook is materially different to affect how the investment strategy may perform over the next three years relative to its category.

Strategy Ratings:

- Positive: Investment strategies expected to outperform the category over the next three years.

- Neutral: Investment strategies expected to perform in line with the category over the next three years.

- Negative: Investment strategies expected to underperform the category over the next three years.

We use a three-year time horizon as it is roughly the average holding period for a private market asset. For Hedge Funds, we use the same strategy rating method but consider a 12-to-24-month performance outlook because of the higher mix of liquid assets that a typical hedge fund may own.

Related Articles

1. Bain Private Equity Outlook 2026: Gaining Traction. (for 717b)

2. Pitchbook, PE Breakdown, published January 13, 2026.

3. PitchBook Q4 2025 NVCA Venture Monitor, as of December 31, 2025

4. IEA’s 2025 World Energy Outlook, published November 12, 2025

5. Barclays Investment Banking Global Shareholder Advisory Group analysis, January 9, 2026

6. HFRI, December 2025

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax, and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit from an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection, or forecast on the economy, stock market, bond market, or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third-party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2026 Institutional Capital Network, Inc. All Rights Reserved.