Professionally managed solutions that incorporate private market investments can help achieve long term retirement income outcomes, as explained in our first paper, Zero Is Not the Answer. Our second paper, Rethinking Private Markets Liquidity in DC Plans, examined the role liquidity plays in defined contribution (DC) plans and how to evaluate it in the context of portfolio diversification. Now, we shift to the responsibilities of the fiduciary and the process they must undertake to determine what role, if any, private market allocations should play in DC plans.

Fiduciaries have long been obligated to act solely in their plan participants’ best interests, apply a consistent and well-reasoned decision framework, and thoroughly document their process. Fiduciary duties include assessing the role and risk of each asset class, understanding the implications for diversification and liquidity, bringing in outside expertise to address gaps in knowledge, determining the reasonableness of fees in a total portfolio context, and recording the rationale behind decisions, both adopted and/or deferred. These responsibilities do not change as DC investment menus evolve or as private market allocations become more accessible; rather, the same prudent process is applied to a broader opportunity set.

A fiduciary must first go through this process (see the Fiduciary’s Roles & Responsibilities sidebar) before determining whether a zero allocation to private markets within their participant’s DC plan is appropriate. After completing a thorough and well‑documented review, a fiduciary may reasonably conclude that private market allocations are not currently in the best interest of their plan participants at this time. As with any allocation decision, the role of each asset class should be periodically reviewed—at least annually, in our view—with the goal of improving retirement outcomes for participants.

The fiduciary’s role and responsibilities

The role of a fiduciary is critical in ensuring plan participants’ best interests are considered within a DC plan. The prudent expert standard outlined in section 404(a)(1)(B) of the U.S. Department of Labor’s (DOL) Employee Retirement Income Security Act (ERISA), requires that a “fiduciary shall discharge that person’s duties with respect to the plan solely in the interests of the participants and beneficiaries; for the exclusive purpose of providing benefits to participants and their beneficiaries and defraying reasonable expenses of administering the plan; and with the care, skill, prudence, and diligence under the circumstances then prevailing that a prudent person acting in a like capacity and familiar with such matters would use in the conduct of an enterprise of a like character and with like aims.”1 Put simply, fiduciaries must follow a thoughtful, well-documented process when evaluating the role an asset class may play in the plan.

A practical framework may include:

- Define objectives: Clarify intended outcomes (return enhancement, risk mitigation, diversification, inflation sensitivity), liquidity needs, and average participant profile.

- Engage qualified experts: Identify gaps in knowledge and partner with internal staff and external partners, such as consultants or advisors, asset managers, and legal counsel, with relevant DC and private markets experience.

- Compare implementation routes: Evaluate structures like collective investment trusts (CITs), separate accounts, and evergreen vehicles for suitability, operational readiness, transparency, and governance.

- Stress test allocations: Assess portfolio behavior across market environments and within a managed account or target date fund (TDF) glide path; evaluate liquidity under rebalancing, contribution flows, redemptions, loans, vesting cliffs, and reenrollment.

- Adopt guardrails: Consider allocation caps, explicit opt in vs. default allocations, rebalancing rules, and contingency plans for liquidity or valuation stress.

- Document the reasoning: Record key assumptions, analysis methods, data sources, expert inputs, alternatives considered, and the rationale for the decision (including “not now”).

Applying fiduciary principles to private market allocations

Recent survey data underscores why a thoughtful fiduciary process matters. In Mercer’s 2025 Voices of the Plan Sponsor survey of 225 U.S. DC plan sponsors representing more than US$77 billion in assets, nearly 60% stated that the primary objective of their retirement program is to help employees achieve their retirement and financial goals (see Exhibit 1).2 To meet this objective, fiduciaries must evaluate how each component of the investment lineup contributes to long-term outcomes, including whether private market assets may play a role.

Private markets are not “new” investments, but they may be new to DC plan menus. As with any unfamiliar asset class, fiduciaries may need additional education or support from external experts. Still, evaluating private markets does not require a new fiduciary framework; it simply extends long‑standing practices to a broader set of investment options.

Private markets are not “new” investments, but they may be new to DC plan menus. As with any unfamiliar asset class, fiduciaries may need additional education or support from external experts. Still, evaluating private markets does not require a new fiduciary framework; it simply extends long‑standing practices to a broader set of investment options.

When determining whether and how to incorporate private markets, fiduciaries should apply the same core responsibilities that guide decisions for public market allocations. This includes assessing how an allocation fits within the plan’s overall investment strategy, how it may influence liquidity needs and fee structures, and how differences in manager selection can impact results. The process should document how decisions were made, what alternatives were considered, and why specific choices were adopted or deferred.

Because these areas require particular attention when evaluating private markets, we briefly expand on four key considerations in the sections that follow: liquidity management, valuation and audit practices, fee evaluation, and manager selection and access.

Evaluating private markets does not require a new fiduciary framework; it simply extends long‑standing practices to a broader set of investment options.

Managing liquidity

Liquidity is a fundamental, and often misunderstood, operational consideration in DC plans, and fiduciaries must understand how any allocation—with daily or periodic liquidity—supports the plan’s ongoing cash‑flow needs. As outlined in our previous paper, most plan‑level liquidity demands are predictable and can often be managed within a diversified portfolio that includes private market investments.3 As Exhibit 2 illustrates, TDF net flows tend to follow consistent, demographic‑driven patterns along the glidepath, reinforcing why plan‑level cash‑flow needs are generally predictable and can be incorporated into a well‑supported liquidity analysis.

For fiduciaries, the key requirement is not to become experts in every liquidity model, but to conduct appropriate due diligence: assessing whether a vehicle’s liquidity features align with plan operations, reviewing how liquidity is monitored and stress‑tested, and ensuring contingency plans are in place. The focus is on confirming that the plan can meet participant activity reliably and that the documentation clearly supports this conclusion.

For fiduciaries, the key requirement is not to become experts in every liquidity model, but to conduct appropriate due diligence: assessing whether a vehicle’s liquidity features align with plan operations, reviewing how liquidity is monitored and stress‑tested, and ensuring contingency plans are in place. The focus is on confirming that the plan can meet participant activity reliably and that the documentation clearly supports this conclusion.

Readers seeking a deeper technical discussion of liquidity structures, operational flows, and stress‑testing frameworks can refer back to Rethinking Private Markets Liquidity in DC Plans, which explores these topics in detail.

Independent valuation and manager audits

Establishing fair value4 and accurate valuations for assets is a core fiduciary responsibility, regardless of whether the underlying assets are public or private. Fiduciaries do not need to become valuation specialists, but they should be familiar with how private market vehicles determine net asset value (NAV), including the role of independent third party valuation agents and the audit processes that validate results.5

A critical distinction is that daily valuation does not require daily liquidity. Private market vehicles can participate in daily‑priced structures even when the underlying assets are not bought or sold each day. What matters is the consistency, governance, and reliability of the valuation methodology, not the liquidity profile of the underlying investments. Reviewing valuation frequency, direct versus indirect approaches, and established reconciliation procedures helps ensure the plan can rely on the information used for participant reporting and operational needs.6

Valuation lag and methodological differences may also influence how private market investments appear within daily valued structures, such as target date funds. Recent regulatory discussions reinforce the need for consistent, predictable valuation models to support daily pricing frameworks.7 Fiduciaries should document how these considerations were evaluated and whether the vehicle’s valuation practices align with the plan’s governance standards. Clear communication is also important so participants understand, in simple terms, that private asset valuations may not move in lockstep with public markets.

Ultimately, the fiduciary responsibility is not to eliminate every complexity, but to ensure that appropriate valuation and audit controls exist in accordance with established accounting and reporting standards,8 that independent oversight is incorporated where needed, and that the rationale for accepting these practices is well documented.

Fees

Fees are often cited as a reason to avoid including private market investments in DC plans, but fee evaluation is not new—and it is already a central part of fiduciary oversight. A common misconception is that fees can be “hidden” within collective investment trusts (CITs). In practice, this is not the case: ERISA 408(b)(2) requires all covered service providers—including those offering CIT‑based TDFs—to disclose clear, upfront information about all plan‑level fees. Fiduciaries are responsible for determining whether those fees are reasonable relative to the services provided.

As Fred Reish, one of the foremost experts on ERISA and fiduciary issues, notes, “a practical definition is that reasonableness is what an informed investor, operating in a competitive marketplace and with knowledge of the material facts, would agree to.”9 This principle has long guided fee assessments in DC plans and continues to apply as investment menus evolve.

Evaluating fees for private market exposures should follow a similar process. Fiduciaries should understand how the vehicle’s fees are structured, how they compare with peer strategies, and how they influence expected net, risk‑adjusted returns at the portfolio level. Notably, Executive Order 14330, “Democratizing Access to Alternative Assets for 401(k) Investors,” underscores that fee assessments should move beyond headline expenses and consider net outcomes within a diversified portfolio.10 Benchmarking total plan costs—including investment management, recordkeeping, and advisory services—is already common practice for most sponsors. PLANSPONSOR’s 2025 DC Plan Benchmarking Survey reinforces this point, noting that the majority of sponsors regularly review and benchmark fees as part of their ongoing governance processes.11

Recent legal developments underscore the importance of this analysis being clearly documented. The U.S. Supreme Court’s decision to hear Anderson v. Intel has raised the possibility that ERISA fee litigation may move toward a “meaningful benchmark” requirement—essentially a legal articulation of the process Reish describes. Whether or not the Court formalizes this standard, the implication is the same: fiduciaries must demonstrate a prudent, consistent, and well‑supported approach to evaluating plan fees, particularly when considering new asset classes such as private markets.

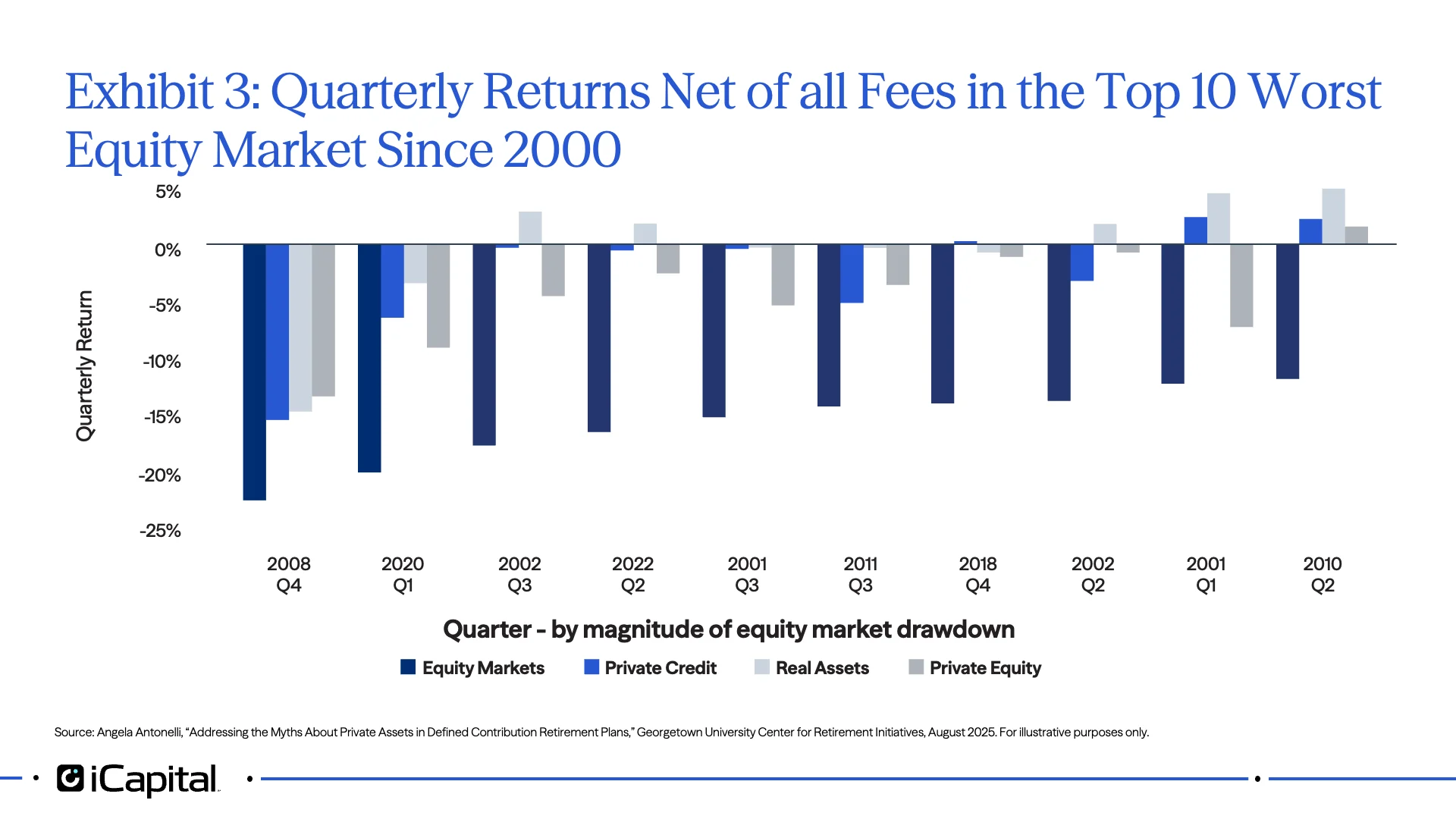

A modest private market allocation that enhances diversification or improves expected net, risk‑adjusted returns may carry higher line‑item fees, but fiduciaries must assess fees in the context of their potential contribution to participant outcomes—not in isolation. Higher fees alone are not a justification for excluding an asset class. What matters is whether the fiduciary’s analysis supports that the allocation is appropriate for the plan’s objectives and is fully documented within the plan’s governance framework. As Exhibit 3 illustrates, fiduciaries should weigh fees alongside expected net outcomes—especially during periods of market volatility—as part of a well supported evaluation.

Manager Selection and Access

Manager Selection and Access

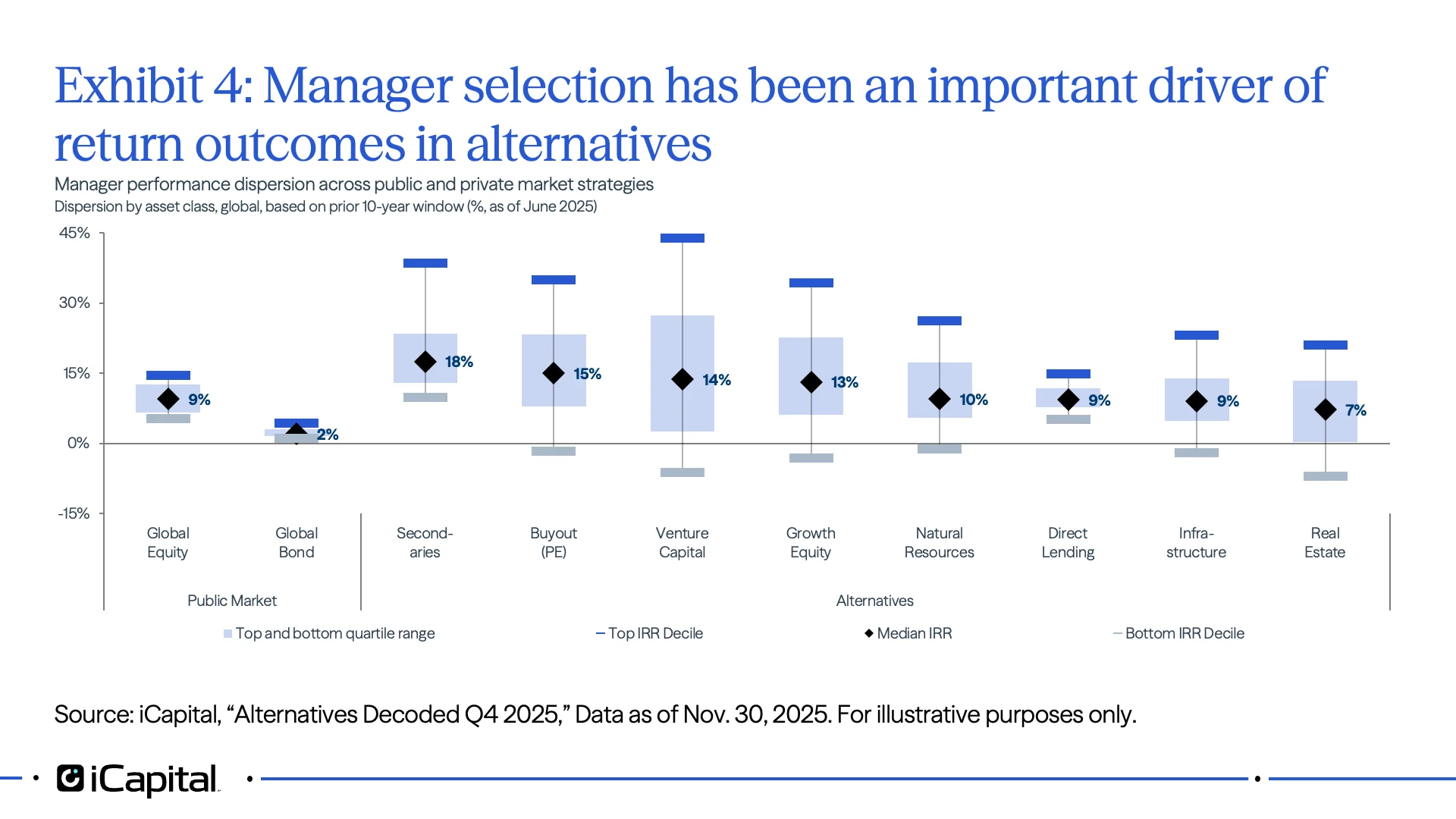

Manager selection is a critical fiduciary consideration for any asset class, but it carries added weight in private markets, where performance dispersion across managers is significantly wider than in public markets (see Exhibit 4). Evaluating whether a private market allocation is appropriate therefore begins with understanding how return expectations compare with public market alternatives and how fees and portfolio fit influence expected net, risk‑adjusted outcomes.

Because private market performance can vary widely based on strategy execution and access to quality deal flow, fiduciaries should have a clear framework for how managers are evaluated and monitored. This typically includes reviewing long‑term capital market assumptions, assessing whether relevant vintage‑year and strategy‑specific benchmarks are used, and determining whether performance appears attributable to manager skill rather than market conditions.

Some private market strategies—such as private credit or infrastructure—may require additional scrutiny of a manager’s underwriting and oversight capabilities. In cases where fiduciaries do not have deep expertise in these areas, engaging external specialists is fully consistent with the prudent expert standard and may be necessary to ensure an informed evaluation.

A well‑documented comparison of available options may support a targeted allocation with clear guardrails—or may lead to a “not now” decision. Either outcome can be prudent. What matters is that the fiduciary process is rigorous, comparative, and aligned with the plan’s objectives and participant needs.

Conclusion

Conclusion

Fiduciaries have long been responsible for applying a thoughtful, well‑documented, and comparative process to every investment decision in a DC plan. As private markets become more accessible through professionally managed solutions, that responsibility does not change — but the opportunity set does. The question is not whether fiduciaries must evaluate private markets, but how they do so: through education, expert input, appropriate guardrails, and a consistent framework that considers liquidity, valuation, fees, and manager selection in the context of long‑term participant outcomes.

Importantly, prudence does not require simplicity or avoidance. As this paper demonstrates, private market exposures can be evaluated using the same foundational principles already applied to public market allocations. When fiduciaries follow a rigorous process — one that incorporates objective analysis, stress‑tested assumptions, transparent documentation, and periodic review — either outcome can be prudent: a targeted allocation with clear rationale, or a well‑supported “not now.” What is not prudent is defaulting to zero based on unfamiliarity or perceived complexity alone.

As the DC landscape continues to evolve, fiduciaries who ground their decisions in process rather than preconceptions will be best positioned to serve participants’ long‑term interests. This includes remaining informed about emerging structures, regulatory developments, and industry best practices that further support responsible integration of private market assets. In that spirit, the next paper in this series will explore the rapidly developing regulatory environment.

The question is not whether fiduciaries must evaluate private markets, but how they do so: through education, expert input, appropriate guardrails, and a consistent framework that considers liquidity, valuation, fees, and manager selection in the context of long‑term participant outcomes.

ENDNOTES

- Source: National Archives and Records Administration. Code of Federal Regulations, Title 29—Labor, §2550.404a‑1, “Investment Duties.” Accessed via the Electronic Code of Federal Regulations (eCFR):

https://www.ecfr.gov/current/title-29/subtitle-B/chapter-XXV/subchapter-F/part-2550/section-2550.404a-1 - Source: Mercer. Voice of the Plan Sponsor: 2025 DC Practices Survey. November 12, 2025. Note: Survey data as of July 2025.

- See: Drew Carrington. Rethinking Private Markets Liquidity in DC Plans. iCapital. January 12, 2026.

- Fair Value is generally defined as: The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

- See: Defined Contribution Alternatives Association (DCALTA). Daily Valuation of Alternative Assets in DC Plans: A Framework for Plan Sponsors and Industry Stakeholders. February 2021.

- See: Standard Board for Alternative Investments (SBai). Private Market Valuations: Governance, Transparency, & Disclosure Guidelines: A Guide for Allocators and Investment Managers. January 2025.

- See: Joshua A. Lichtenstein, Sharon Remmer, Jonathan M. Reinstein. “Planning to Take Advantage of Executive Order on Alternatives in 401(k)s: Five Key Takeaways and Five Action Items for Managers.” Ropes & Gray. August 11, 2025.

- For example: U.S. Generally Accepted Accounting Principals (GAAP) or the International Financial Reporting Standards (IFRS).

- See: Fred Reish. “The New Fiduciary Rule (15): Reasonable Costs and Reasonable Compensation.” January 17, 2024.

- See: The White House, “Democratizing Access to Alternative Assets for 401(k) Investors,” Executive Order, August 7, 2025.

- See: PLANSPONSOR. 2025 PLANSPONSOR DC Survey: Plan Benchmarking. January 7, 2025.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Market LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2026 Institutional Capital Network, Inc. All Rights Reserved.