Investment Outlook

Early-stage venture capital includes investments in companies to fund product development, build the employee base or implement customer acquisition strategies. Given that early-stage venture companies are smaller and less mature compared to late-stage, investments can be more speculative and typically involve long holding periods. Returns in early-stage venture strategies are often based on a small number of highly successful investments that can influence returns across an entire portfolio.

For early-stage strategies, the velocity of deal flow and exits are an indicator of health, leading to consistent flow of returns to investors. One measure – distribution yield as a share of net asset value – is 6.5%, or near its 20-year low of 4.1% and far short of it’s 20-year average of 17.7%.1 Distributions likely need to exceed historic averages for an extended period (one to two years) before venture fundraising sees a sustainable uptick from recent lows.

On a positive note, exit activity increased in 2024. However, the data is mixed. Smaller deals led to the recovery, yet these deals are unlikely to generate the level of returns that investors expect. And the time between rounds is creeping higher, at 1.4 years for early-stage companies, seen in Exhibit 1.

The growing time between rounds indicates a backlog of companies that may be eager for a liquidity event – whether an acquisition, additional venture investment or shutdown.

The growing time between rounds indicates a backlog of companies that may be eager for a liquidity event – whether an acquisition, additional venture investment or shutdown.

At a macro level, economic uncertainty makes for a more difficult backdrop for deal activity. Yet early-stage venture is more protected relative to late-stage venture: 43% of disclosed venture exits in 2024 were $100 million or less and 73% of all exits were acquisitions.2 Said another way, early-stage venture is not reliant on larger or mega transactions which are more greatly impacted by an economic slowdown.

Please see Additional Information at the bottom of this report for definition of early and late-stage venture capital.

Recent Market Trends

The biggest hurdle for the venture industry from 2021 to 2023 was slow deal activity. Venture funds operate on a cycle. They raise capital, make investments, exit investments, and then return capital to investors. When one of these steps slows down, it creates friction throughout the system – a slowdown in exits means less capital returned to investors and then hesitancy from these investors in committing to the next venture capital fundraising.

The sluggish deal environment comes from high valuation marks set in 2021 – 2022, leaving venture capital firms and start-up companies hesitant to raise additional capital or sell at a lower valuation and face possible employee and shareholder dilution.

In fact, 25% of all deals in 2024 were done at flat and down valuations.3 This was arguably inevitable, and a rightsizing of valuations is a positive for deal activity ahead. In looking at just early-stage deals in Exhibit 3, a modest valuation step-up – from 1.7x to 1.8x in 2024 – suggests a recovery is underway, but it could be a slow recovery.

With a wait and see mode, it’s an investor friendly environment. There is a backlog of early-stage companies that face capital constraints. At the same time, venture funds are sitting on near-record levels of dry powder. New commitments made in the current period will be allocated over the next three-plus years allowing venture firms to be selective.

Industry Focus: Technology

The straightforward reason to include venture capital exposure in a portfolio is because it’s the closest proxy to innovation. Early-stage companies are at a point where they’re developing products or technologies and identifying product-market-fit. Venture capital plays a role by enabling these companies to scale innovation in their formative years.

Technology is the largest industry for venture investment. There are many reasons for this. For starters, advancements in technology have created a secular shift where business predominantly occurs online. And many areas of technology can scale quickly with smaller amounts of required capital, potentially providing greater return on investment opportunity.

Technology companies also tend to have financial attributes such as recurring revenue and high cash margins which venture investors favor. Lastly, technology – once focused on hardware, software and networking – now covers a wide field including healthtech, climatetech and fintech companies, amongst others.

Most recently, the technology world has been almost solely focused on artificial intelligence (AI), which represented 44% of all venture capital investment (early and late-stage) in 2024, according to Crunchbase and EY. AI is likely to continue to drive outsized deal value and measuring the health of venture overall likely requires separating these blue-bird transactions.

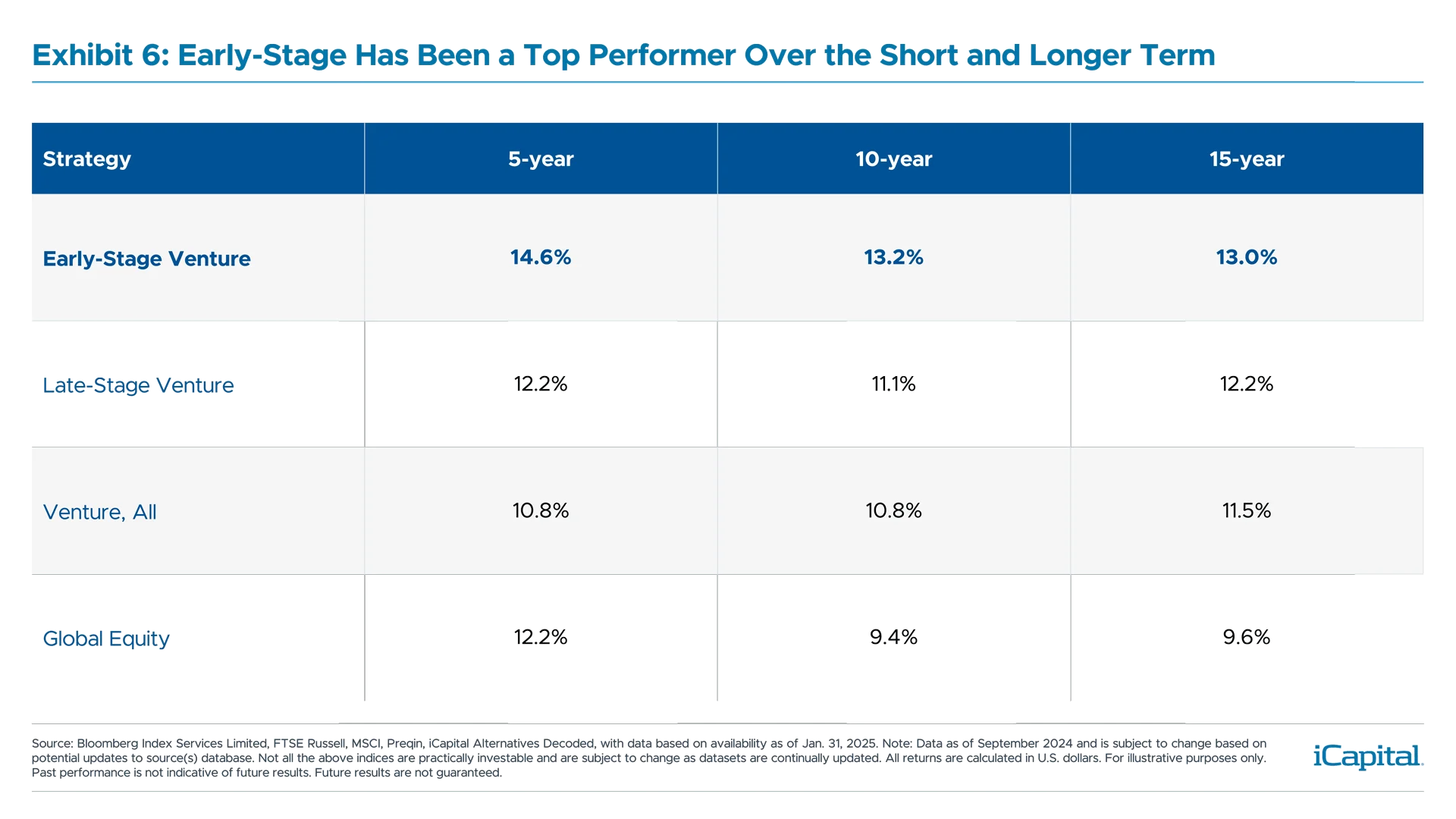

Performance Snapshot

Endnotes

- PitchBook, “Q4 2024 PitchBook-NVCA Venture Monitor”, January 13, 2025.

- PitchBook, “Q4 2024 PitchBook-NVCA Venture Monitor”, January 13, 2025.

- PitchBook, “2024 Annual US VC Valuations Report”, February 10, 2025.

Additional Information:

We define Early-Stage Venture as companies in Series A or B of financing; and Late-Stage as Series C or D.

Performance Snapshot, Exhibit 6: Venture - All proxied by Preqin Venture Capital Index. Late-Stage Venture proxied by Preqin Venture Capital Late-Stage Index. Early-Stage Venture proxied by Preqin Venture Capital Early-Stage Index. Global Equity proxied by MSCI ACWI Total Return Index.

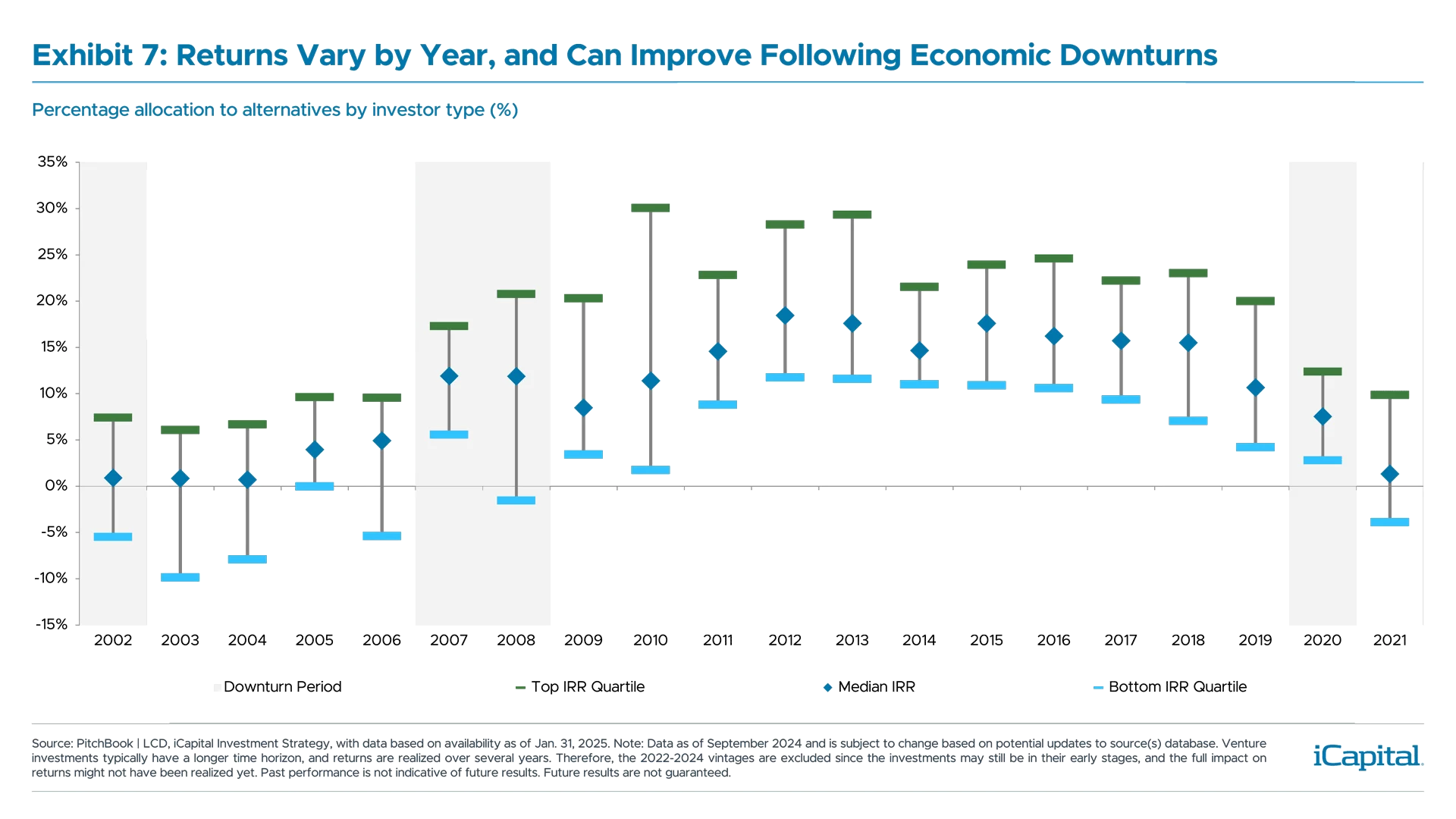

IRR Dispersion Exhibit, Exhibit 7: Venture proxied by Preqin Venture Capital Index

AngelList is a platform that connects startups with angel investors and also offers data and various services for fundraising, hiring, and launching products.

The National Venture Capital Association (NVCA) is an organization that represents the US venture capital community and advocates for public policy that supports the VC ecosystem. The PitchBook-NVCA Venture Monitor, is produced jointly by NVCA and PitchBook.

Index Definitions

MSCI ACWI Index: MSCI’s flagship global equity index is designed to represent performance of the full opportunity set of large- and mid-cap companies from developed and emerging markets around the world.

Preqin Venture Capital Index: The index covers over 14,000 closed-end funds captured in the broader Private Capital index including funds/strategies listed as Early Stage, Early Stage: Seed, Early Stage: Start-up, Expansion/Late Stage, Venture (general), as defined by Preqin

Preqin Venture Capital Early-Stage Index: The index covers closed-end funds captured in the broader Private Capital index including funds/strategies that invests only in the early stage of a company’s life defined either as Seed or Start-up, as defined by Preqin.

Preqin Venture Capital Late-Stage Index: The index covers closed-end funds captured in the broader Private Capital index including funds/strategies that invests in companies towards the end of the venture stage cycle, as defined by Preqin.

IMPORTANT INFORMAITON

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax, and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit from an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection, or forecast on the economy, stock market, bond market, or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third-party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2025 Institutional Capital Network, Inc. All Rights Reserved.