Most investors will experience three to four significant bear markets throughout their lifetime. For baby boomers, these periods include:

- The 1987 crash

- The dot-com bubble burst (2000-02)

- The global financial crisis (2007-09)

While each downturn was challenging, the bear market of 2022 might have been the most unsettling for many investors, especially retirees, as the average 60/40 portfolio fell 17.5%.1

Why Was 2022 More Concerning for Retirees?

Even though the S&P 500 fell nearly 50% from 2007-09, most baby boomers were still working, allowing time for retirement portfolios to recover.2 By 2022, however, most baby boomers had entered retirement. Watching a portfolio decline by 17.5% while making withdrawals can make even the most confident retirees question their financial stability.

The Rise of Annuities for Downside Protection

In 2024, the annuity industry saw record sales of $432.6 billion.3 Notably, 80% of total annuity sales were in solutions offering downside protection, including3:

- Fixed annuities

- Fixed indexed annuities (FIAs)

- Structured annuities

Compare that to 2014, when these three annuity types accounted for merely 34% of total annuity sales.4

Why Are Risk-Managed Annuities Gaining Popularity?

In retirement, investors seek protection. Avoiding losses is often more important than achieving an additional 20% return. The questions advisors should contemplate are:

- How much protection suffices?

- How much additional upside can we expect if we move from a known return with 100% protection (fixed annuity) to an unknown return tied to an index with 100% protection (FIA) to an unknown return tied to an index with some protection (structured annuity)?

- How do we quantify these trade-offs to best match the annuity with each client’s risk profile?

Comparing Annuity Options

Let’s examine three annuity strategies5 an advisor might consider for a client:

- A Multi-Year Guaranteed Annuity (MYGA) with a fixed 5% rate for five years

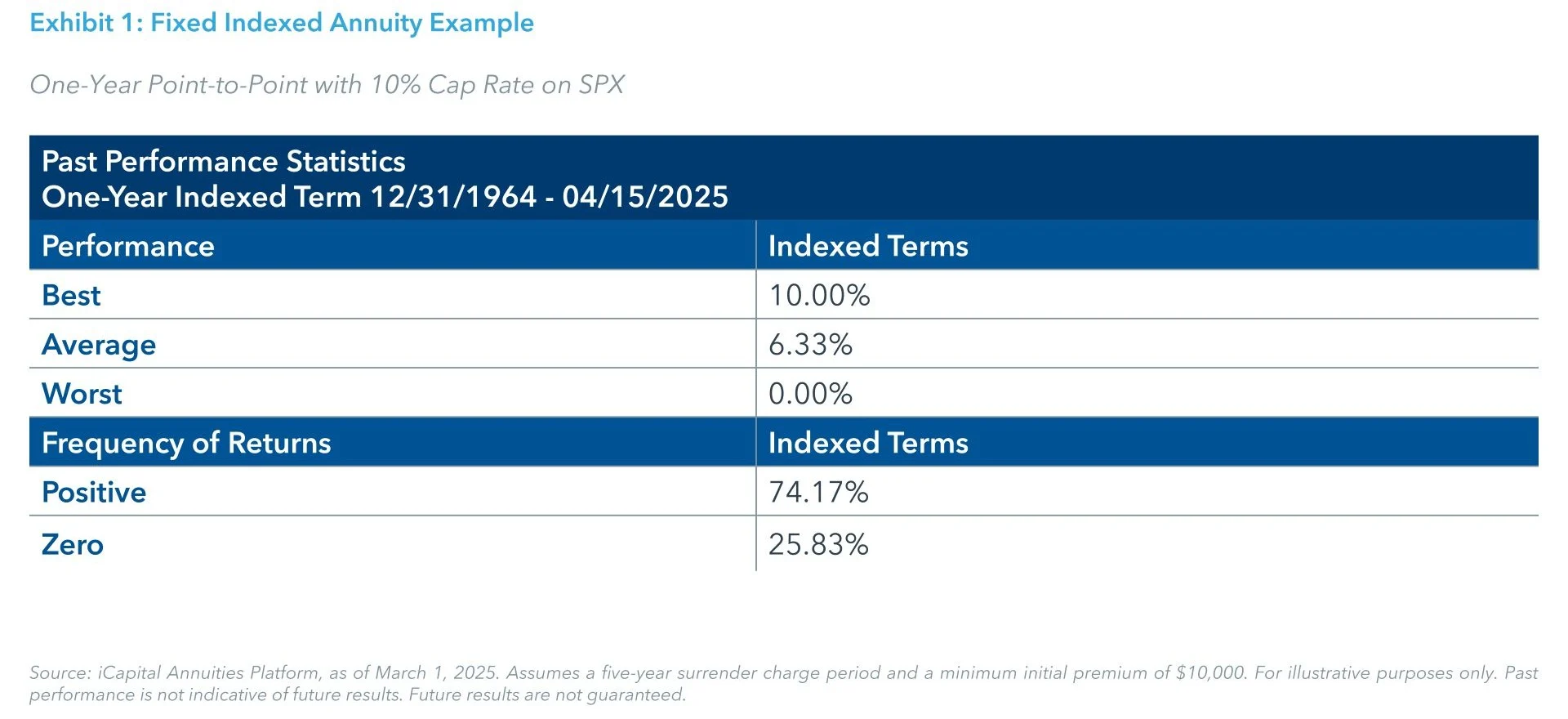

- A FIA with a one-year point-to-point on the S&P 500 with a 10% cap

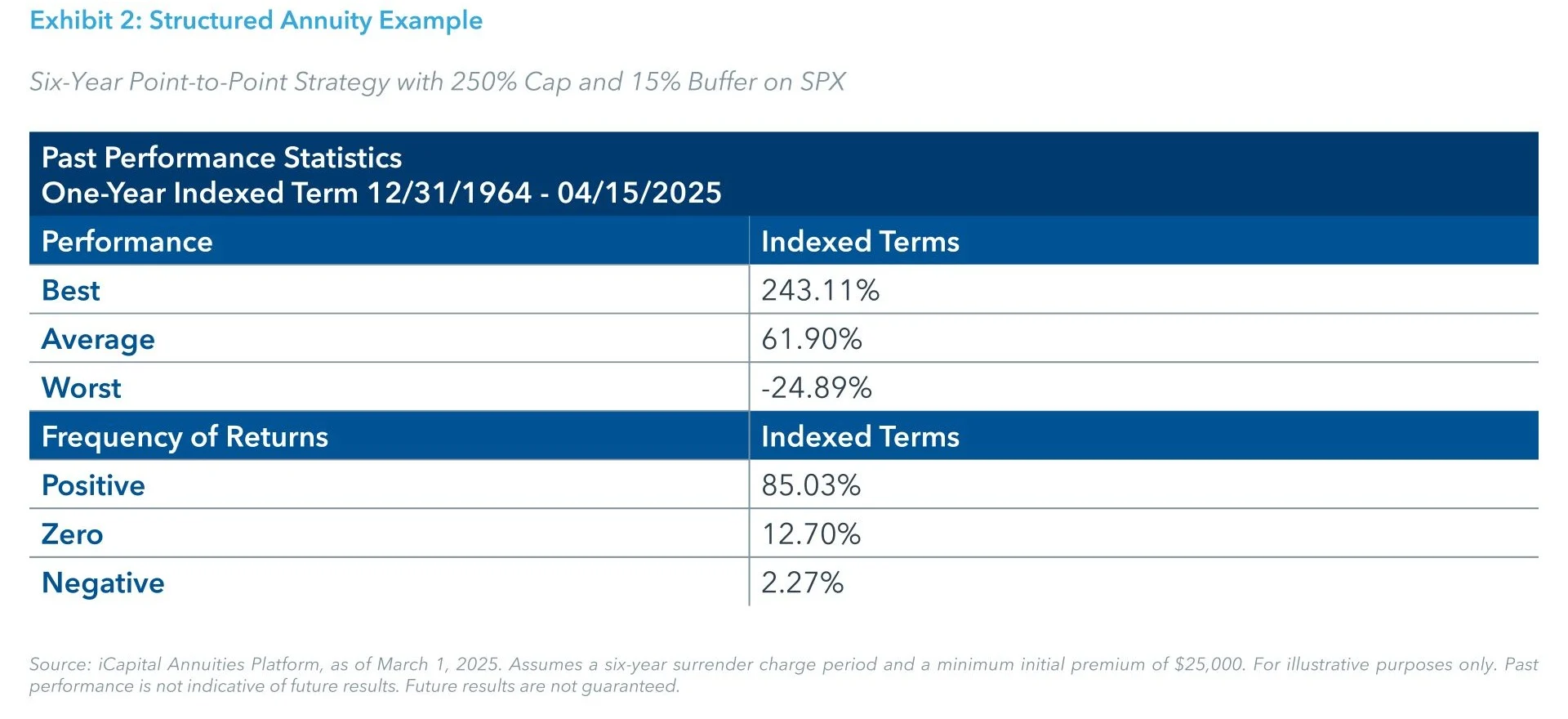

- A structured annuity with a six-year point-to-point on the S&P 500 with a 250% cap and a 15% buffer

The MYGA offers a fixed interest rate, guaranteed for the term, and so a client knows how their investment will grow. A FIA also has 100% downside protection, though its return each year is contingent upon the price change of the S&P 500 and the renewal rate of the cap. While these two factors make the future return impossible to determine, iCapital’s annuity analytics can calculate hypothetical historical returns by applying a 10% cap to every one-year period over the last 60 years.

Key Insights

Key Insights

This analysis informs us that the average return of these thousands of possible one-year periods would have been 6.33%. The client would have received a positive return up to the 10% cap, 74.17% of the time. The advisor can now better assess whether the potential additional return over the 5% MYGA would justify taking on unpredictable returns.

What about the implications of the structured annuity choice? Here, we have introduced the potential to lose money. If the price of the S&P falls more than 15% over the six-year crediting period, the client will suffer a loss equal to the percentage drop in excess of that amount. How often has that happened over a six-year period? How much extra return could we have earned by accepting this additional risk? When we run this strategy on iCapital’s platform for annuities, tool, analyzing every six year-period over the last 60 years, the average return of this strategy would have been 61.9%, or 8.36% compounded per year.

Key Insights

Key Insights

The 15% buffer would not have fully protected the downside just 2.27% of the time, and the maximum loss would have been 24.89% back in 1968-1974. The strategy would have resulted in a 0% return (where the price of the index declined but by no more than 15%) 12.7% of the time.

Aligning Annuities with Client Risk Profiles

The goal is to match the right annuity product with the right strategy within that product for each client’s risk profile. In efficient markets, as risk and uncertainty increase, expected returns should rise accordingly. Some clients may prefer the 5% guarantee. Others may be comfortable with an uncertain annual return, knowing they are likely to exceed 5% on average while still fully protecting the downside. And, based on 2024’s record structured annuity sales, many clients will accept the possibility of losing money over the term in exchange for hoping to achieve 8%+ per year.

The Importance of Data in Annuity Decisions

As retirement strategies evolve, advisors can benefit from robust analytics to evaluate annuity trade-offs effectively. Fortunately, today’s data-driven tools make it easier than ever to optimize product selection.

Endnotes

- Morgan Stanley: Big Picture, Return of the 60/40, April 2024.

- Investopedia: The Stock Market Crash of 2008, November 2024.

- LIMRA: 2024 Retail Annuity Sales Grow 12% to a Record $432.6 Billion.

- LIMRA: US Individual Annuity Yearbook 2023.

- Source: iCapital annuities platform, as of March 1, 2025. For illustrative purposes only. Past performance is not indicative of future results. Future results are not guaranteed.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ANNUITIES ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. The information is not intended as investment advice and is not a recommendation about managing or investing retirement savings. Actual annuity contracts may differ materially from the general overview provided. Prior to making any decision with respect to an annuity contract, purchasers must review, as applicable, the offering document, the disclosure document, and the buyer’s guide which contain detailed and additional information about the annuity. Any annuity contract is subject in its entirety is to the terms and conditions imposed by the carrier under the contract. Withdrawals or surrenders may be subject to surrender charges, and/or market value adjustments, which can reduce the owner’s contract value or the actual withdrawal amount received. Withdrawals and distributions of taxable amounts are subject to ordinary income tax and, if made prior to age 591⁄2, may be subject to an additional 10% federal income tax penalty. Annuities are not FDIC-insured. All references to guarantees arising under an annuity contract are subject to the financial strength and claims-paying ability of the carrier. iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2025 Institutional Capital Network, Inc. All Rights Reserved. | 2025.05