LIMRA recently reported that total U.S. annuity sales climbed to a record $216.6 billion during the first half of 2024, up 20% from the previous year.1 Not surprisingly, after hearing this stat, I witnessed a positive mood from the attendees associated with the annuity industry at the recently concluded LIMRA Annual Conference in Nashville.

After almost 20 years of no growth, annuity sales finally broke out of their narrow range and topped $300 billion for the first time in 2022. And now that it appears as though $400 billion is the new benchmark, how much longer will it be until $500 billion is eclipsed? In my view, annual annuity sales could get there sooner than expected.

With fixed, indexed, and registered index-linked annuities prices tend to get better when interest rates rise, and the opposite happens when interest rates fall. Ten-year treasuries peaked recently around 5% but now that the Federal Reserve has started cutting interest rates, because of this positive correlation, logic would suggest we should see a decline in sales in all three of these annuity product types as rates decline. The bigger question is when could this decline potentially happen?

The last time we witnessed ten-year treasuries at these peak levels was the summer of 2007. As interest rates started to fall, fixed annuity sales actually increased by over 52% from 2007 to 2009. This is because insurance companies don’t typically reduce the rates on their products overnight, they typically give 2-3 weeks’ notice. This gave advisors time to talk to their clients about locking in today’s annuity rates before the next rate cut.

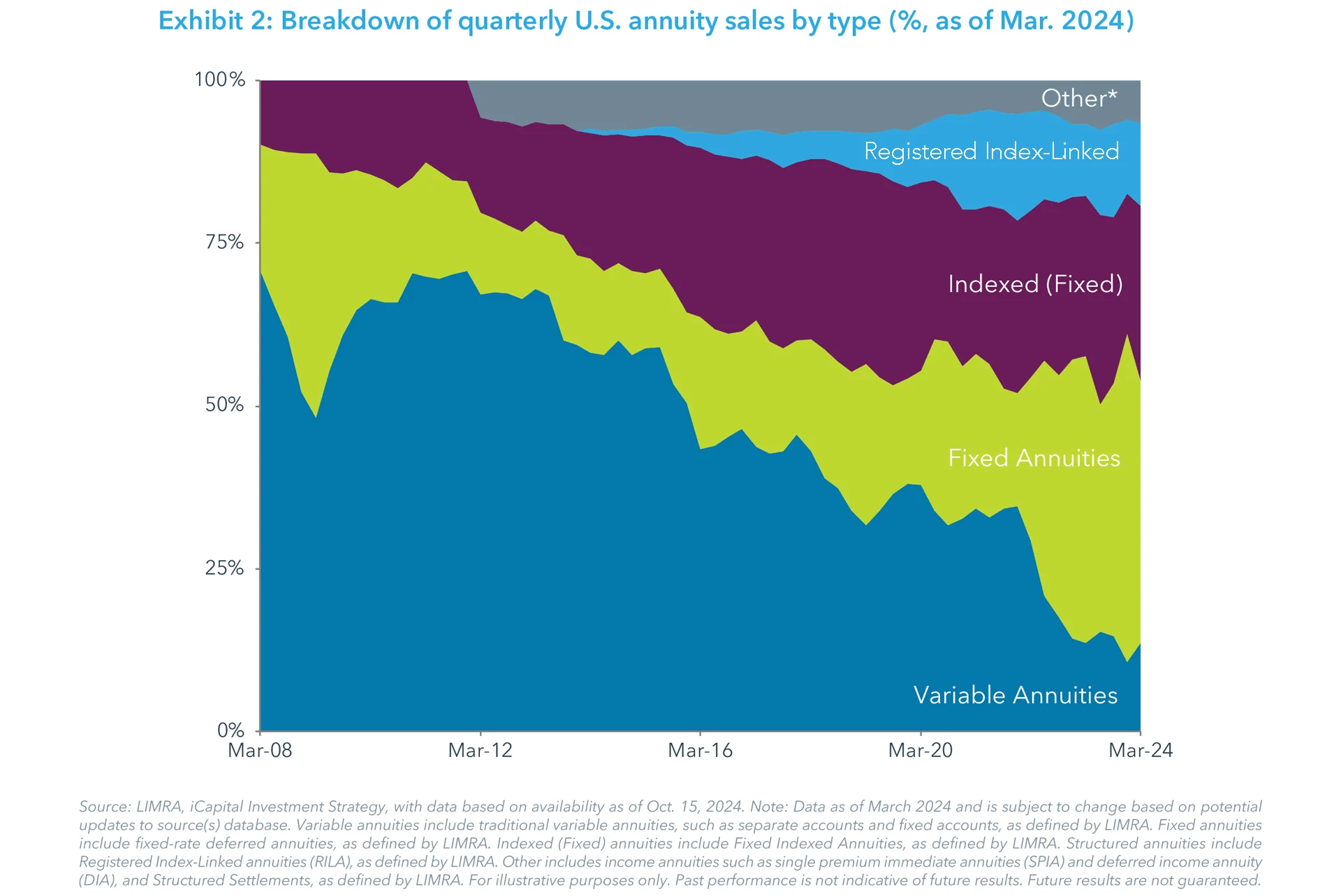

The annuity industry, however, is very different today than it was in 2007. Back then, of the $256.8 billion in total annuity sales, $184 billion (71.6%) went into variable annuities – a product that has a low correlation to interest rates. Fixed indexed annuities were still in their infancy. According to LIMRA, total sales of that product were only $25 billion.2 Registered indexed-linked annuities (RILAs) weren’t even on the drawing board. Fast forward to today, and the mix of annuity sales is very different. LIMRA reported that, in the 2nd quarter of 2024, fixed, indexed, and registered index-linked annuities represented 80% of total annuity sales, while traditional variable annuities made up only 14%.

The change in the annuity sales mix could have an interesting effect on a potential influx in to annuity contracts thanks to four key differences. First, back in 2007, annuity sales would have been mostly limited to fixed annuities. This time around, it could impact fixed, indexed, and registered index-linked annuities. Second, dozens of carriers might cut rates in the coming months compared to 15 or 20 carriers back in 2007. Third, there are significantly more pre-retirees and retirees today than ever before – many of whom have investment objectives that are more focused on the protection these three annuity types provide. And finally, the sales base on these three annuity types is significantly higher today, $340 billion compared to an $80 billion sales base in 2007. If carriers announce a series of rate cuts, they could create one wave after another of inflows into annuity contracts. The only question is will it be a three-foot wave or a tsunami? Given the unprecedented demand for protection, I’m expecting the tsunami. I just hope the industry has enough sandbags to survive it.

1. LIMRA: U.S. Annuity Sales Jump 26% in Second Quarter 2024, Fueled by Record FIA and RILA Sales.

2. US Individual Annuity Yearbook 2023 (limra.com).

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ANNUITIES ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. The information is not intended as investment advice and is not a recommendation about managing or investing retirement savings. Actual annuity contracts may differ materially from the general overview provided. Prior to making any decision with respect to an annuity contract, purchasers must review, as applicable, the offering document, the disclosure document, and the buyer’s guide which contain detailed and additional information about the annuity. Any annuity contract is subject in its entirety is to the terms and conditions imposed by the carrier under the contract. Withdrawals or surrenders may be subject to surrender charges, and/or market value adjustments, which can reduce the owner’s contract value or the actual withdrawal amount received. Withdrawals and distributions of taxable amounts are subject to ordinary income tax and, if made prior to age 591⁄2, may be subject to an additional 10% federal income tax penalty. Annuities are not FDIC-insured. All references to guarantees arising under an annuity contract are subject to the financial strength and claims-paying ability of the carrier.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2024 Institutional Capital Network, Inc. All Rights Reserved. | 2024.06