In our 2023 Annuity Insights Report, we predicted that as the baby boomers continued to head into retirement, their desire for portfolio protection would drive annuity sales to record highs. This predication has come to pass. We anticipate that this desire for protection will not be a short-term phenomenon because the baby boomers and the silent generation hold almost $100 trillion in wealth, or 64.9% of the total wealth in the country.1 It’s likely to drive the need for protected products such as fixed, indexed, and RILAs for many years to come. Based on this expected trend, it’s not surprising that LIMRA reported 2024 industry sales hit a record $432.4 billion, up 12% over the previous year.2 While fixed annuities did decline 7% from 2023 levels due to lower interest rates in the second half of 2024, indexed and RILA annual sales rose 31% and 37% respectively.3

Is this Level of Growth Sustainable?

In addition to preretirees’ and retirees’ strong desire for protection, there are four key factors that we believe will continue to drive annuity sales higher in 2025:

1. Record stock prices will likely increase the desire for protection – The S&P 500 achieved returns of 20%+ for the second consecutive year – the first time that’s happened since the late 1990’s.4 Investors that entered the year feeling confident about their ability to finance a long retirement likely ended the year feeling even better. For preretirees and retirees focused on protection, not going backwards may be far more important than potentially earning another 10-20% in upside. This could be especially true for investors concerned about a market correction.

2. Additional Fed rate cuts – Just as the correlation between rising interest rates and high fixed interest rates helped propel fixed, indexed, and registered index-linked annuity sales, declining interest rates could eventually have a similar impact and lead to lower sales due to less attractive pricing. The key word here is “eventually.” Insurance companies don’t typically reduce the rates on their products overnight; they typically give 2-3 weeks’ notice. This gives advisors time to talk to their clients about locking in today’s annuity rates prior to the next potential rate cut. Therefore, if we continue to see a series of Fed rate cuts, we could expect to see a series of corresponding sales spikes in these products. Sales should only moderate when investors become indifferent between the old rate and the new rate.

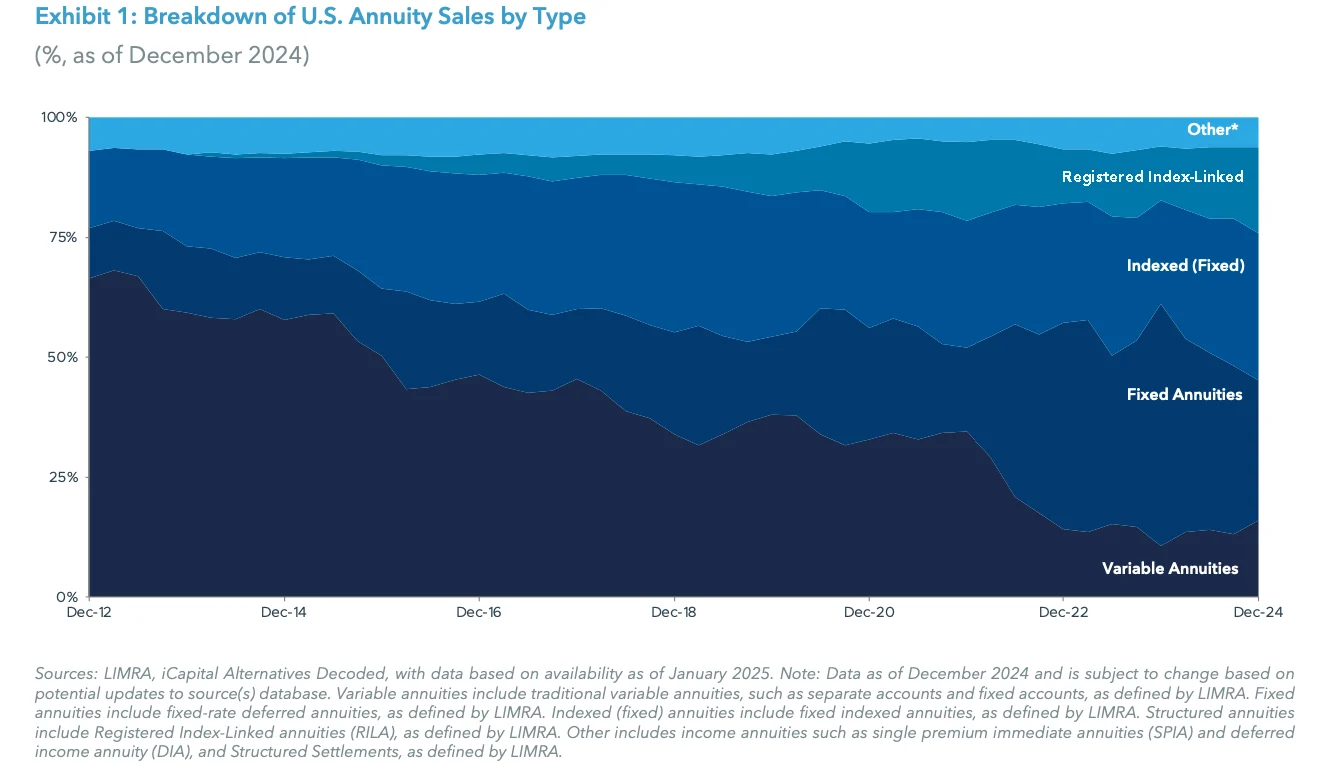

3. More companies and more products – The last time ten-year treasuries peaked at levels we recently witnessed was the summer of 2007. The annuity industry looked very different back then. Of the $256.8 billion in total annuity sales, $184 billion (71.6%) went into variable annuities – a product that has a low correlation to interest rates.5 Fixed indexed annuities were still in their infancy. According to LIMRA, total sales of that product were only $25 billion.6 Registered indexed- linked annuities (RILAs) weren’t even on the drawing board in 2007. Fast forward to today and the mix of annuity sales is very different. LIMRA reported that, for 2024, fixed, indexed, and RILAs were 80% of total annuity sales, while traditional variable annuities were only 14%. This shift in product mix combined with significant sales growth over the last several years has increased product supply and the overall number of annuity contracts available in the market. While annuity sales were concentrated amongst 10-15 carriers in 2007, today LIMRA tracks the annuity assets of 44 different companies. This increase means that if carriers cut rates because of interest declines, there are currently more companies that would perform rate cuts compared to 2007, which could mean a significant difference in how it impacts sales.

4. Money in motion – According to LIMRA, fixed annuity sales were $113 billion in 2022. A good portion of this would be in a rate duration and surrender charge of three years. For illustrative purposes, assuming 50% of the 2022 sales were in three-year products earning a 4% average interest rate, in 2025 alone, as these three-year durations end, approximately $65 billion in annuity assets could become eligible for reallocation. Some of this money could remain in the existing contract – either because the insurance company will elect to offer a competitive renewal rate to retain the money or because renewal options won’t be addressed by clients. Some of these contracts could also get reinvested in other investment solutions, however, it’s possible that more than half of this money will be moved to another annuity with another carrier to capture higher rates. This could create a steady supply of new sales in 2025 and beyond.

Registered Index-Linked Annuities – A Relevant Product for a Large Investor Pool

LIMRA calculated RILA sales to be $65.2 billion in 20247 – surpassing last year’s record-breaking total. In fact, RILA sales have achieved record levels each year since their introduction in 2014. Given the product’s unique ability to mix and match various levels of protection and upside potential over different periods of time, we expect this annuity category to continue to gain acceptance for many years to come.

The general level of interest rates does play a key role in determining RILA rates, even though its crediting rates are not as interest rate dependent as both fixed and indexed annuities. Therefore, we do not expect rates on this product to decline substantially in correlation with interest rate declines.

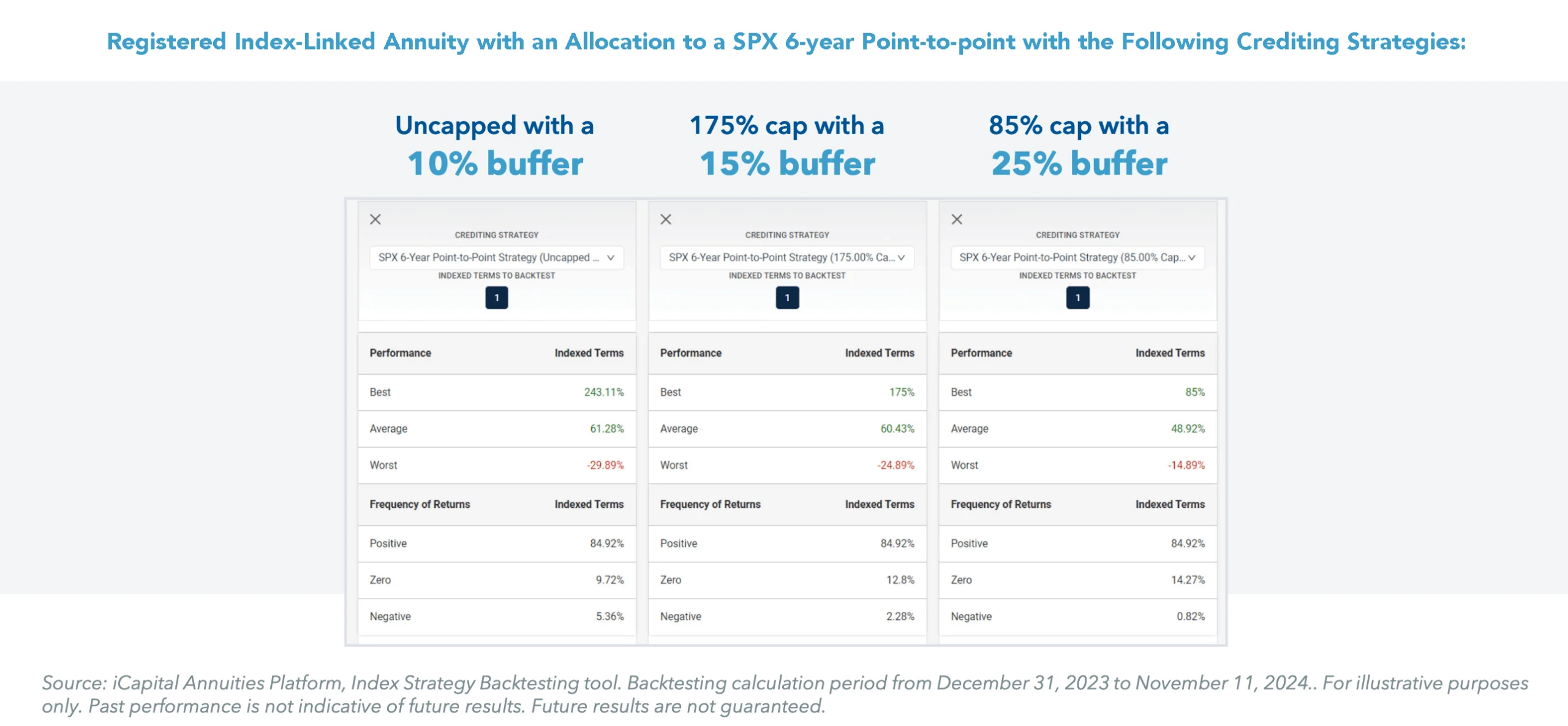

Additionally, many RILAs offer a wide range of available strategies. The example below illustrates how a RILA could be uniquely qualified to offer a solution for clients with varying needs for protection.

The charts above summarize every six-year period of the S&P 500 beginning 12/31/23 through 11/11/24 to reveal the following:

- Over the last 60 years, the uncapped strategy with the 10% buffer yielded the highest possible return but also the worst possible return during a six-year period over the available time frame.

- Due to the lower cap, the strategy with a 175% cap and a 15% buffer delivered a lower best return than the uncapped strategy but only a slightly less average return. This is because the higher buffer not only reduces the worst return number, but moves some of the negative return results to a zero return.

- The strategy with the 85% cap and a 25% buffer of course had the lowest best as well as the lowest percentage of negative results. However, because of the significantly lower cap, this strategy also delivered meaningful lower average returns.

These numbers demonstrate how RILAs, with flexible crediting strategy options, could allow for better alignment with client goals than traditional 60/40 portfolios. Despite the above calculations’ assumption that the listed crediting rates are in effect for the entire 60-year look back period — and though past performance is certainly no indication of future performance — this example showcases how the need for downside protection from preretirees and retires could make a strong case for portfolio inclusion and lead to increased RILA sales.

A 2024 AARP report shows that the top concern for retirees is the fear of running out of money,8 which indicates that retirees want to feel secure about their finances. This understandable fear may make many retirees cautious about taking risks. Annuities can address this fear in two distinct ways. For those who want to protect their retirement savings, the options of fixed, indexed, and RILAs can all play a significant role. For those who want the peace of mind of getting a protected income for life, annuities may increasingly become a selected solution. The direction of the stock market will not change the trend for these needs. Therefore, we expect 2025 to be yet another record year for annuities.

Endnotes

1. The Federal Reserve, Distribution of Household Wealth in the U.S. since 1989, December, 2024.

2. LIMRA, LIMRA: 2024 Retail Annuity Sales Power to a Record $432.4 Billion, January 2025.

3. LIMRA, LIMRA: 2024 Retail Annuity Sales Power to a Record $432.4 Billion, January 2025.

4. LIMRA, iCapital Alternatives Decoded, January 2025.

5. U.S. Global Investors, AI Frenzy Drove the S&P 500’s Best Two-Year Gains Since the Dot-Com Era, January, 2025.

6. LIMRA, U.S. Individual Annuity Yearbook, December, 2023.

7. LIMRA, LIMRA: 2024 Retail Annuity Sales Power to a Record $432.4 Billion, January 2025.

8. AARP, 5 Retirement Fears and How to Conquer Them, October, 2024.

Important Information

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax, and legal advisors to understand the implications of any investment specific to your personal financial situation.

ANNUITIES ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. The information is not intended as investment advice and is not a recommendation about managing or investing retirement savings. Actual annuity contracts may differ materially from the general overview provided. Prior to making any decision with respect to an annuity contract, purchasers must review, as applicable, the offering document, the disclosure document, and the buyer’s guide which contain detailed and additional information about the annuity. Any annuity contract is subject in its entirety to the terms and conditions imposed by the carrier under the contract. Withdrawals or surrenders may be subject to surrender charges, and/or market value adjustments, which can reduce the owner’s contract value or the actual withdrawal amount received. Withdrawals and distributions of taxable amounts are subject to ordinary income tax and, if made prior to age 591⁄2, may be subject to an additional 10% federal income tax penalty. Annuities are not FDIC-insured. All references to guarantees arising under an annuity contract are subject to the financial strength and claims-paying ability of the carrier.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2025 Institutional Capital Network, Inc. All Rights Reserved.