Key Takeaways

- AI disruption is broadening, moving beyond software into financial services, trucking & logistics, and life science tools, driving notable single‑stock dispersion.

- Certain business models remain more exposed, particularly low‑capex, data‑light, product‑centric, or weak‑relationship models, while firms with proprietary data or strong enterprise ties maintain wider moats.

- Sentiment remains resilient despite rising volatility; the M&A pipeline impact is still contained, and business confidence remains above long‑term averages.

- Dispersion continues to favor hedge funds – particularly multi strategy platforms – that can capitalize on sharp moves within the S&P 500, while the index hovers near all‑time highs. Structured investments may also help provide downside protection if volatility remains elevated in the near term.

AI continues to move in what feels like a “seek‑and‑destroy” mode, with concerns around disruption now spreading beyond software (discussed here) and into industries such as financial services, trucking and logistics, and life science tools. After the large drawdowns across these groups, investors are increasingly asking who might be next.

While AI will inevitably reshape parts of the market, we think it is just as important to focus on companies that are more capital intensive, have access to proprietary data, focus on providing services and have strong enterprise relationships.

At the same time, questions have emerged around whether this disruption could begin to weigh on capital‑markets activity and business sentiment. While still early, it appears that the groups being impacted by disruption only account for a relatively modest portion of the global M&A pipeline. Nvidia’s earnings on Wednesday could also serve as an important catalyst, potentially helping to stabilize sentiment and put a floor under parts of the AI trade.

With dispersion rising within equity markets, this backdrop should be supportive for hedge funds, which are well positioned to capture opportunities on both the long and short side. And in public markets, we would be favoring structured investments which should provide downside protection, or given the reset in volatility, better terms on income notes.

Inside the AI Trade: Will Nvidia Save The Day?

As the AI trade continues to come under pressure, Nvidia’s earnings on Wednesday (2/25) could be an important catalyst going forward. With AI disruption top of mind for markets – particularly as it relates to software – we think there will be a heightened focus on the CUDA software and Nvidia’s ability to reinforce the scale and durability of its AI ecosystem. We expect Nvidia to reiterate that its CUDA moat remains deep, which should help offset any near‑term concerns around rising competition. Investors will also be watching gross margins closely, which we believe Nvidia should be able to maintain given its pricing power, product mix, and continued demand for high‑end compute.

Another reason why Nvidia may follow its historical pattern of a beat‑and‑raise is the strength in hyperscalers’ CapEx forecasts. This quarter, forecasts have been raised by roughly $140 billion, with CapEx expected to grow 60% and 10% year‑over‑year in 2026 and 2027, respectively – providing continued support for Nvidia’s data‑center revenue outlook.1

In addition to Nvidia, Salesforce will also report earnings on Wednesday. We expect the market to focus on the subscription revenue guide, particularly amid rising concerns about internally developed AI‑driven software. We believe an inline outlook could help put a floor under the AI trade – and potentially stabilize software more broadly – especially after last quarter’s results hinted at early signs of an inflection in the business.

Disruption Broadens Out:

But, will this be enough to stop the AI disruption trade? What started as a software story has now broadened out, with AI disruption impacting areas such as trucking & logistics, financial services and life science companies.

While the disruption narrative really began with Anthropic’s recent plugin announcements, mentions of AI disruption on company earnings calls have spiked this reporting season. In fact, there have been 120 mentions of AI disruption on earnings calls this quarter – more than double the previous quarter and roughly 100 mentions above the five‑year average (see Exhibit 1).2

Given the large drawdowns we have seen in these groups and heightened mentions of disruption risk, investors remained focused on which areas may be next. We think companies and groups that are more susceptible to disruption risk have four qualities.

Given the large drawdowns we have seen in these groups and heightened mentions of disruption risk, investors remained focused on which areas may be next. We think companies and groups that are more susceptible to disruption risk have four qualities.

- Low Capital Intensity: Sectors that require significant physical infrastructure (e.g., manufacturing, industrials, utilities) are inherently harder to disrupt. In contrast, low‑capital intensive sectors – media, marketing, IT tools and software – are more exposed because AI can create substitutes and can be deployed nearly instantly with minimal incremental cost.

- Lack of Proprietary Data: Businesses whose value proposition rests on widely available, undifferentiated information are more easily displaced by AI systems trained on massive public datasets. Firms with unique, hard‑to‑replicate data ecosystems enjoy a structural moat that reduces disruption risk.

- Application/product focus: Areas that are heavily application- or product‑based appear more vulnerable than service‑based businesses. Products and tools can often be replaced quickly, whereas service providers with embedded workflows, ongoing support, and large enterprise integrations benefit from stronger network effects and higher switching costs

- Strength of relationships: Companies with weaker or predominantly consumer-facing relationships – where loyalty is minimal and product substitution is easy – face greater disruption risk. Conversely, firms with strong enterprise relationships, deep integration, and recurring workflows tend to be more insulated.

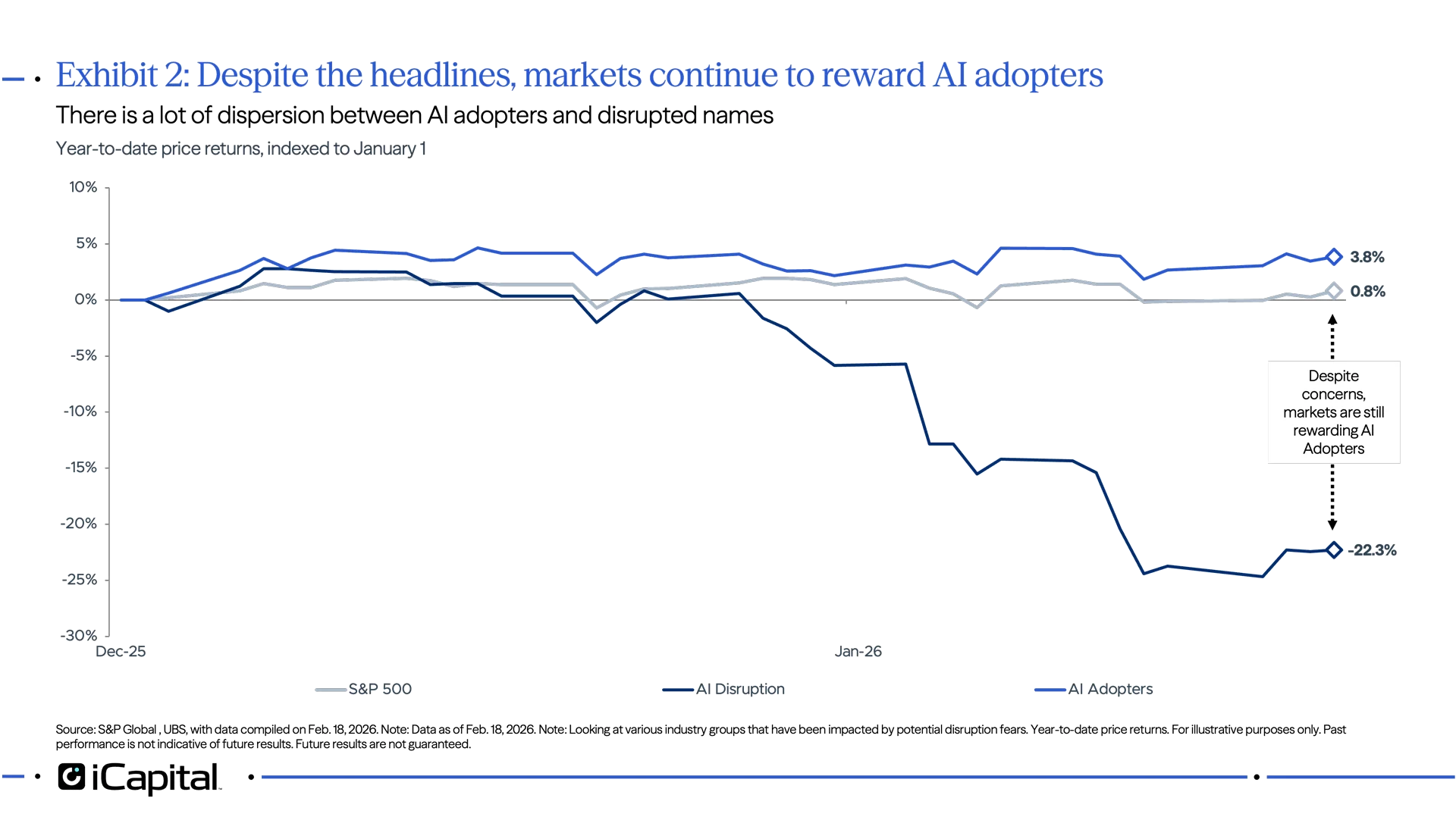

But, it is also important to think about how AI can be additive to firms. AI adoption has been increasing, even if slower than initial estimates. Currently, 18.9% of U.S. established businesses have adopted AI, with adoption expected to rise to 22.1% in the coming months.3 The firms leading in adoption include information services, professional services, education services and finance/insurance firms.4 We are seeing this in market performance, where AI adopters have been outperforming the disruption names by roughly 26% since the start of the year (see Exhibit 2).5

But, will sentiment weigh on capital market activity?

But, will sentiment weigh on capital market activity?

As witnessed in 2025, sentiment can shift quickly and weigh on capital market activity. Currently, with the VIX index above 20, we have already seen some deals get postponed such as Clear Street and Liftoff Mobile, which could be an indication that the latest bout of volatility related to disruption is starting to weigh on sentiment, or at least weigh on valuations for subset of offerings.6 While this remains a risk and something we are monitoring closely, our iCapital Business Sentiment Barometer continues to recover from its post–Liberation Day trough and remains above its long‑term historical average (see Exhibit 3), suggesting that, for now, disruption‑related volatility has not fully translated into a deterioration in corporate confidence.

Also looking at sectors and groups that have been impacted by AI disruption, its exposure to the proposed M&A pipeline appears to be relatively manageable. Currently, software only makes up 11%, while the other impacted groups represent an additional 12.5% (see Exhibit 4).7

So, while sentiment can change quickly, we still think “disrupted” areas represent only a portion of the current M&A pipeline. And while we have seen volatility tick up since the beginning of 2026, markets still remain near all-time highs and business sentiment still seems supportive, which should continue to keep the capital market window open.

So, while sentiment can change quickly, we still think “disrupted” areas represent only a portion of the current M&A pipeline. And while we have seen volatility tick up since the beginning of 2026, markets still remain near all-time highs and business sentiment still seems supportive, which should continue to keep the capital market window open.

Investment Implications : Dispersion is rising, but limited impact on the index

Despite the sharp selloffs in the industry groups being impacted by AI disruption, it has yet to bleed into the broader market, with the S&P 500 still near its all‑time high. Given the significant moves we’ve seen at a company level, we think this backdrop should continue to favor hedge funds – particularly multi-strategy – which are well positioned to take advantage of these dislocations and the pick‑up in capital‑markets activity that is still expected in 2026.

In addition, with volatility likely to remain elevated this year and U.S. equities expected to deliver mid‑ to high‑single‑digit returns, the low correlation and lower‑volatility profile of hedge‑fund strategies should offer attractive diversification benefits in portfolios.

In public markets, we think the current environment presents a compelling opportunity for structured investments. While we expect the market to continue distinguishing between AI beneficiaries and at‑risk names, we believe we are closer to the end of the disruption phase – particularly in software – than the beginning. That said, if disruption mentions keep rising on earnings calls, volatility is likely to remain elevated. Against this backdrop, structured investments can help provide downside protection or enhance income within the portfolio.

ENDNOTES

- Meta, Microsoft, Amazon, Alphabet and Oracle company data, as of Feb. 19, 2026.

- Bloomberg, as of Feb. 17, 2026.

- Goldmans Sachs, as of Feb. 18, 2026.

- Goldmans Sachs, as of Feb. 18, 2026.

- S&P Global, UBS, Goldman Sachs, as of Feb. 18, 2026.

- Bloomberg News, as of Feb 12, 2026.

- Morgan Stanley, as of Feb. 11, 2026.

INDEX DEFINITIONS

AI Adopters Basket: is a basket of stocks that are actively adopting AI, where AI plays a significant or core role in the investments and where the company has the scale (data, capital, reach) to expand market share via AI.

AI Disruption Basket: Is a basket of stocks where AI could automate existing workflows or where software can be rebuilt internally using AI tools.

S&P 500 Index: The S&P 500 is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 of the top companies in leading industries of the U.S. economy and covers approximately 80% of available market capitalization.

VIX Index: The Cboe Volatility Index (VIX) is a real‑time benchmark designed to measure the market’s 30‑day expected volatility derived from S&P 500® index (SPX) options.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit from an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.