Private credit has enjoyed a decade of explosive growth but is now facing questions about its future. Some investors have a lack of clarity around the proliferation of new private credit vehicles, primarily their liquidity mechanics, while legitimate concerns are brewing around portfolio credit quality. But one thing is certain: financial advisors are revisiting their private credit allocations with an eye to downside protection.

Nearly every asset manager, particularly in the current climate, describes themselves as “highly conservative”. Given credit is about avoiding losses, it’s not surprising that managers speak routinely about their downside case forecasting and the contractual protection that their loans can provide.

But how do we evaluate conservatism? There are a handful of statistics that help quantify how lenders manage risk. With the appropriate context (i.e. relative rather than absolute values), these factors can provide a solid framework.

Loan Yields

Lenders that offer new origination yields at or near market rates is a general indicator they are staying within their underwriting standards. The risk lies with lenders that are trying to achieve higher returns by compromising credit quality or chasing higher yields by making loans to risky borrowers. A first lien loan that pays a 12% coupon is almost always riskier than a loan priced at Secured Overnight Financing Rate (SOFR) + 400-500 basis points (bps), about the levels for new middle market originations.1

There may be instances where a proprietary origination relationship results in above market returns. But with the proliferation of private credit competition, these outliers are less common. Further, the diversity within business development company (BDC) portfolios reduces the impact of a truly outsized risk—the 10 largest non-traded BDCs average 363 positions (Exhibit 2).

Portfolio by Security Type

The commonality in security type across direct lending loan portfolios isn’t a differentiating factor for downside protection. Senior secured lending results in high recovery rates but the loans can still face principal loss in the event of default. Loans in BDC portfolios are mostly senior secured first lien, which is the highest in the repayment hierarchy. For example, loan portfolios for the top ten BDCs have over 90% of their loan portfolios comprised of first-lien loans. These funds also have an issuer loan-to-value (LTV) in the 40% range, meaning there is about 60% equity loss before the credit is touched.2 Outliers to these statistics may be pursuing a strategy that belongs in a different category (i.e., distressed).

To supplement the similarities in security types in portfolios, advisors can look at the average issuer LTV and the history of default for the fund manager. LTV ratios do not increase risk linearly, meaning a portfolio moving from 65% to 75% LTV is a materially riskier move than a shift from 40% to 50% LTV.

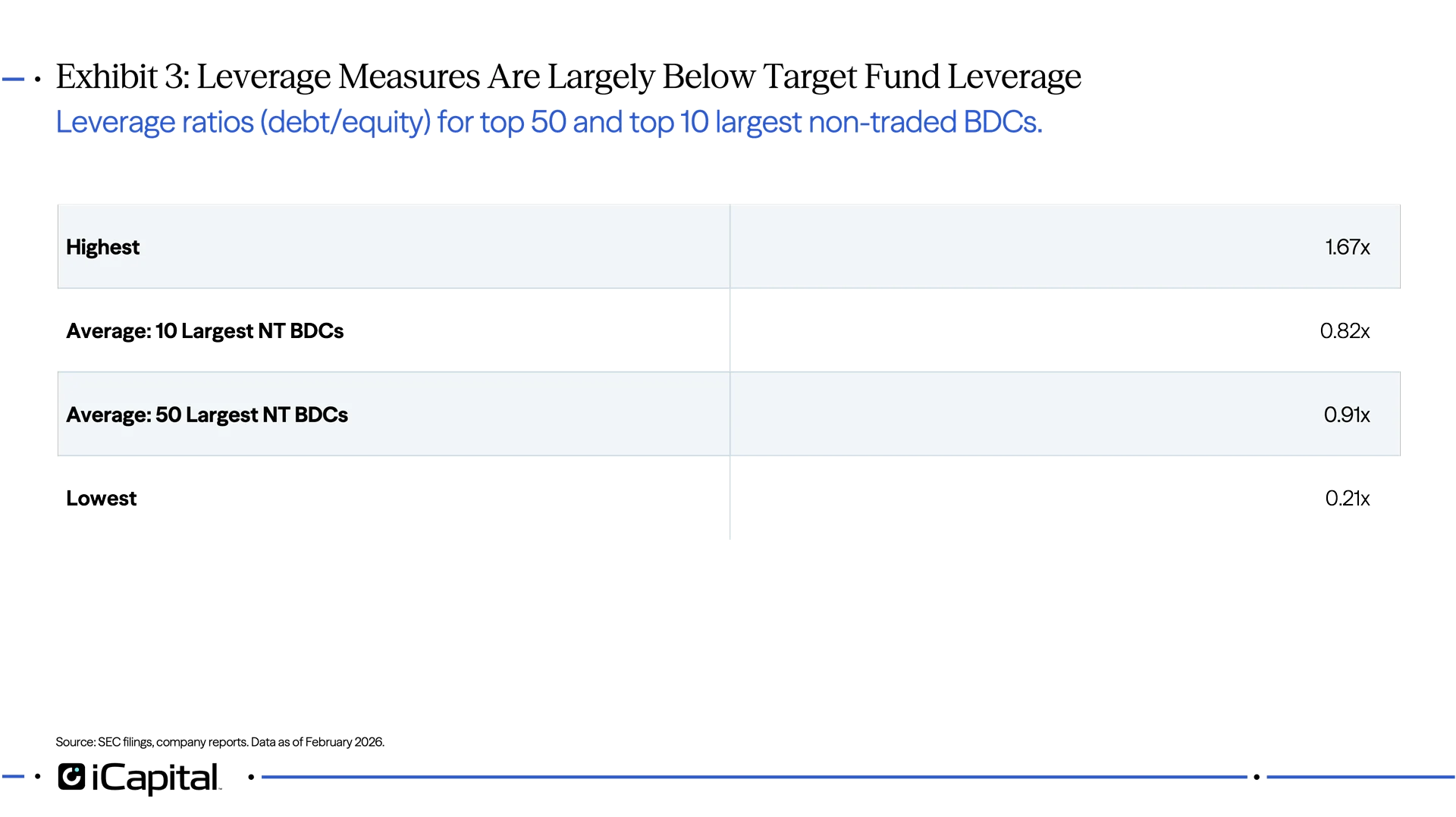

Leverage

Most non-traded BDCs currently maintain leverage below their respective target amount. From a leverage standpoint, risk can generally materialize in three ways: 1) a fund increases its leverage quickly and towards 2.0x (debt/equity), which could indicate a manager is chasing returns, 2) if a fund is overly levered and is struggling to raise new capital, and 3) stress on liquidity because as leverage increases, liquidity and financial flexibility decline.

Advisors should recognize that most BDC carries leverage with the median leverage of the top 50 largest BDCs at 0.89x, well below the regulatory limit of 2.0x.

Payment-in-Kind (PIK)

Payment-in-Kind (PIK)

PIK usage is often talked about as a problem for direct lenders, because it’s viewed as a sign of portfolio stress. In general terms, PIK enables borrowers to use forms other than cash, such as additional debt or equity, to make loan interest payments. Given that PIK income is a natural part of the direct lending business model, it’s fair to question where it starts to become a burden.

There is a natural limiting pressure to manage PIK—if PIK income exceeds 10% of total income, the portfolio could face liquidity stress. This is because BDCs are required to distribute 90% of income, regardless of whether that income is earned in cash or PIK. In other words, when PIK income exceeds 10% of total income, there will be a mismatch in cash interest received and the income paid out.

Further, it’s important to distinguish between “good” and “bad” PIK. Good PIK are features that lenders offer at the time of loan origination. The lender may want to help portfolio companies reinvest in market opportunities or provide additional flexibility for when a business need arises. Bad PIK is when PIK is offered as a retroactive amendment, often in instances of borrower stress.

According to Lincoln International, 11% of private loans paid PIK income in the fourth quarter of 2025 (note: this measure is a percentage of loans, not a percentage of income).3 This measure was relatively flat in 2025 but 58% of those loans included Bad PIK features, up from about 40% at the end of 2022.4 Rising Bad PIK features can be a leading indicator of strain entering the credit portfolio.

Read more on mechanics of PIK here: Painting a PIKture: The Benefits and Risks of PIK in Private Credit – iCapital

Sector Exposure

Advisors can also evaluate sector-level PIK income and LTV trends as leading indicators of portfolio risk. Industry exposure to private credit portfolios is generally well managed but there are indicators that can signal stress within a given sector. For example, the largest BDCs have about 17% portfolio exposure to software (more details on software are here: iCapital Market Pulse: Surveying the Software Space – iCapital).5 Yet, technology companies are growing more reliant on PIK interest (Exhibit 5).

Other Questions for Fund Managers

The ongoing monitoring of investor concentration and behavior is a healthy stress test for advisors, especially as BDCs offer limited redemptions. Investor concentration is not easy to track, but a good topic to ask managers when conducting diligence. Advisors can also consider the investor geographic base of U.S. domestic investors versus non-U.S.

In addition, too much interconnectivity with a particular private equity sponsor can pose a risk. The quality of the private equity owner alongside who a Fund is investing is an important factor in mitigating risk. Concentration with a sponsor that is experiencing broad portfolio distress reduces the leveragability of the underlying portfolio companies.

Many 2021-22 vintage deals are now reaching typical refinancing windows. During this market peak period, many managers deployed capital aggressively when base rates were near zero. This environment favored deal-making at highly levered levels while disciplined underwriting may have been less of a focal point. These same 2021-22 deals are now at the time where they typically face refinancing (the average direct loan length since 2020 is 3.8 years).6 As such, the loans from that period that remain outstanding may be underperforming and operating under the stress of their capital structures.

Parting Thoughts

Amid the market turbulence in private credit, fundamentals are a true measuring stick. Metrics such as defaults make the headlines, but defaults are a lagging indicator. Measures such as relative new origination yields, the trendline in PIK income, LTV trends, and how leverage is used is a baseline to help advisors level-set portfolio health on a relative basis.

ENDNOTES

- Source: Cliffwater LLC, February 2026. Note, Other includes original issue discount and credit spread adjustment. For illustrative purposes only. Past performance is not indicative of future results. Future results are not guaranteed.

- Exhibit 1 and SEC filings.

- Lincoln International, February 2026.

- Lincoln International, February 2026.

- SEC filings.

- Cliffwater Direct Lending Index, February 2026.

INDEX DEFINITIONS

Cliffwater Direct Lending Index (CDLI): An asset-weighted index of over 11,000 directly originated middle market loans totaling $264B. It seeks to measure the unlevered, gross of fee performance of U.S. middle market corporate loans, as represented by the asset-weighted performance of the underlying assets of Business Development Companies (BDCs), including both exchange-traded and unlisted BDCs, subject to certain eligibility requirements.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax, and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit from an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection, or forecast on the economy, stock market, bond market, or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third-party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2026 Institutional Capital Network, Inc. All Rights Reserved.