Deal activity – including IPOs and M&A – has been stuck in a holding pattern. Heading into 2025, we were of the view that a second Trump term could usher in a more pro-business, market-friendly backdrop, unlocking a wave of transactions. Instead, persistent headwinds – from tariff headlines to growth and recession fears – have largely kept dealmakers sidelined.

Importantly though, the dealmaking engine hasn’t stalled but rather shifted gears. And as we approach the back half of the year, green shoots are beginning to emerge. From our seat, a healthy backlog of potential deals remains in the pipeline as deal activity hasn’t been derailed – just delayed. We now expect momentum to build in late Q3, with a more pronounced lift in Q4 and into 2026.

Current State of Play

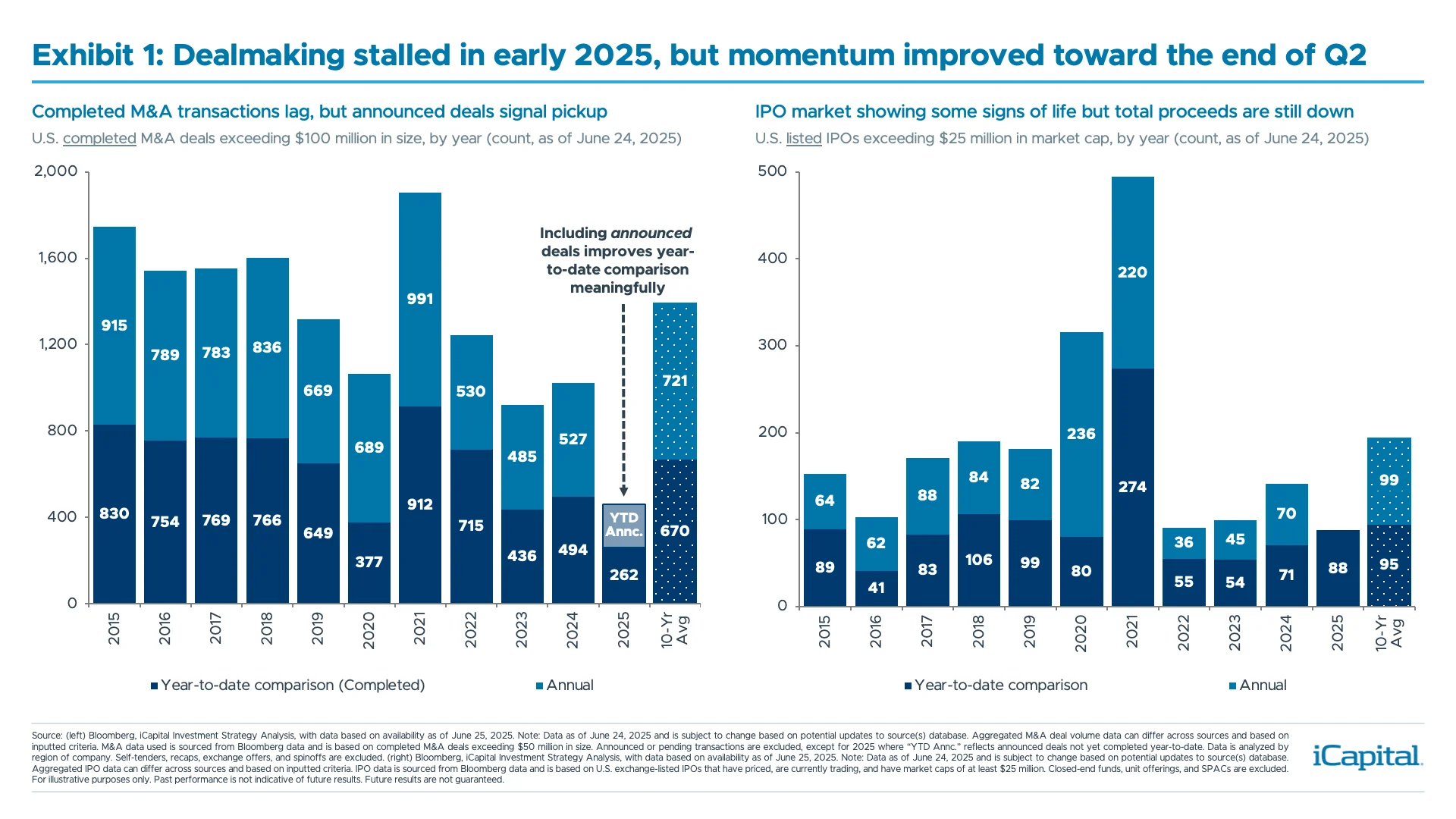

Broadly speaking, deal activity remains soft and below average – but signs of improvement are emerging, particularly around the flow of announced deals in the latter part of Q2. Both M&A and IPO activity were sluggish over the first four months of the year, however, the latter part of May and into June have seen a notable pickup in announced deals, suggesting momentum is starting to build.

On the M&A front, completed U.S. M&A transactions are down -47% year-to-date (through June 24th) versus the same period in 2024 (Exhibit 1).1 Yet, when including announced (and pending) deals, the decline narrows to just -7% – a more constructive signal that activity is picking up.2 Still, both sponsored (private equity-led) and strategic (corporate) deals remain below historical levels.3

Notably, the sharp drop in deal volumes following the early April “Liberation Day” tariffs highlights just how sensitive M&A activity is to policy uncertainty.4 And while there has been modest progress on trade, cross-border M&A remains especially weak – pressured by currency dynamics (weaker U.S. Dollar) and a continued pivot by both executives and sponsors toward domestic opportunities that are limited to broader geopolitical and trade tensions.5

IPOs, meanwhile, are showing signs of life but activity is still subdued. So far in 2025 (through June 24th), 88 companies – including high-profile names like Chime and CoreWeave – have priced on U.S. exchanges, raising roughly $13.5 billion.6 While that’s a +24% increase in deal count compared to the same period in 2024, total proceeds are still down -11%, suggesting smaller deal sizes and a more cautious investor base.7 In fact, activity remains below the 10- and 20-year averages on both a year-to-date and annualized basis.8 So, despite some early traction, the IPO window remains narrow and selective, with most activity concentrated in a handful of high-quality names.

What Will It Take to Turn the Corner?

What Will It Take to Turn the Corner?

We’re watching four key drivers that could unlock a sustained pickup in deal activity:

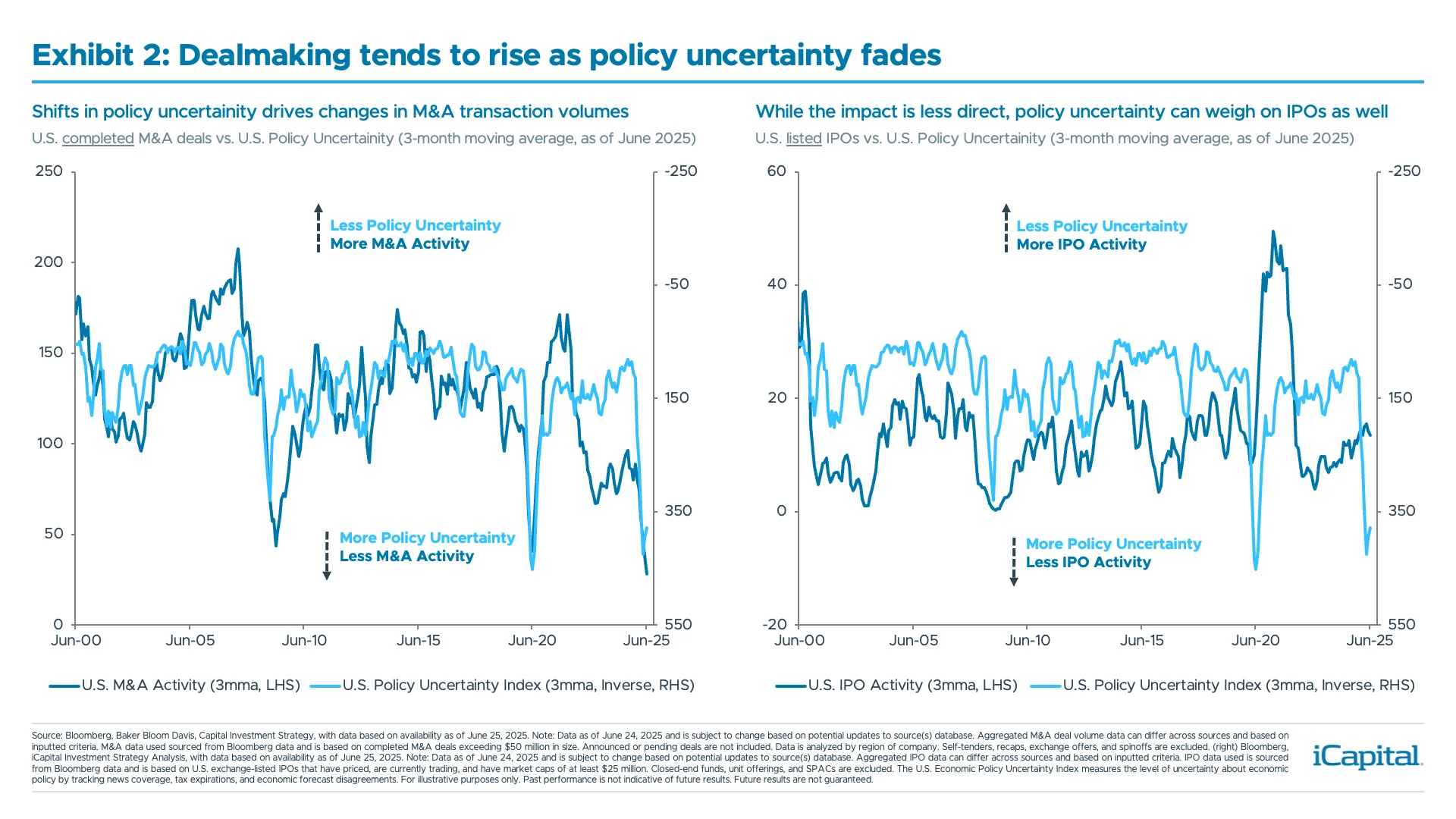

- Reduction in Trade Policy Uncertainty: Trade headlines have been a persistent challenge this year. However, businesses are growing more comfortable operating in what’s now a more “known unknown” environment. With recent progress on trade negotiations and firming expectations around a relatively more stable tariff backdrop, companies are now better positioned to quantify and price-in the impact of tariffs. In particular, it now seems increasingly likely that a 10% effective tariff rate will serve as a floor, providing a clearer baseline for planning – even if some sectors and countries are subject to higher rates.9 The key point here is that businesses can work around and adapt to unfavorable policies, but they can’t underwrite uncertainty. As clarity improves in the months ahead – even if tariff deadlines shift and get pushed out – the drag from trade uncertainty should ease. That, in turn, could give executives and GPs greater confidence to pursue deals, and while the impact on IPOs is less direct, a more stable macro environment generally supports public market activity as well (Exhibit 2). In fact, historically, a 100-point shift in policy uncertainty typically leads to a 10% change in cash M&A spending by S&P 500 companies – highlighting just how powerful clarity can be for dealmaking.10

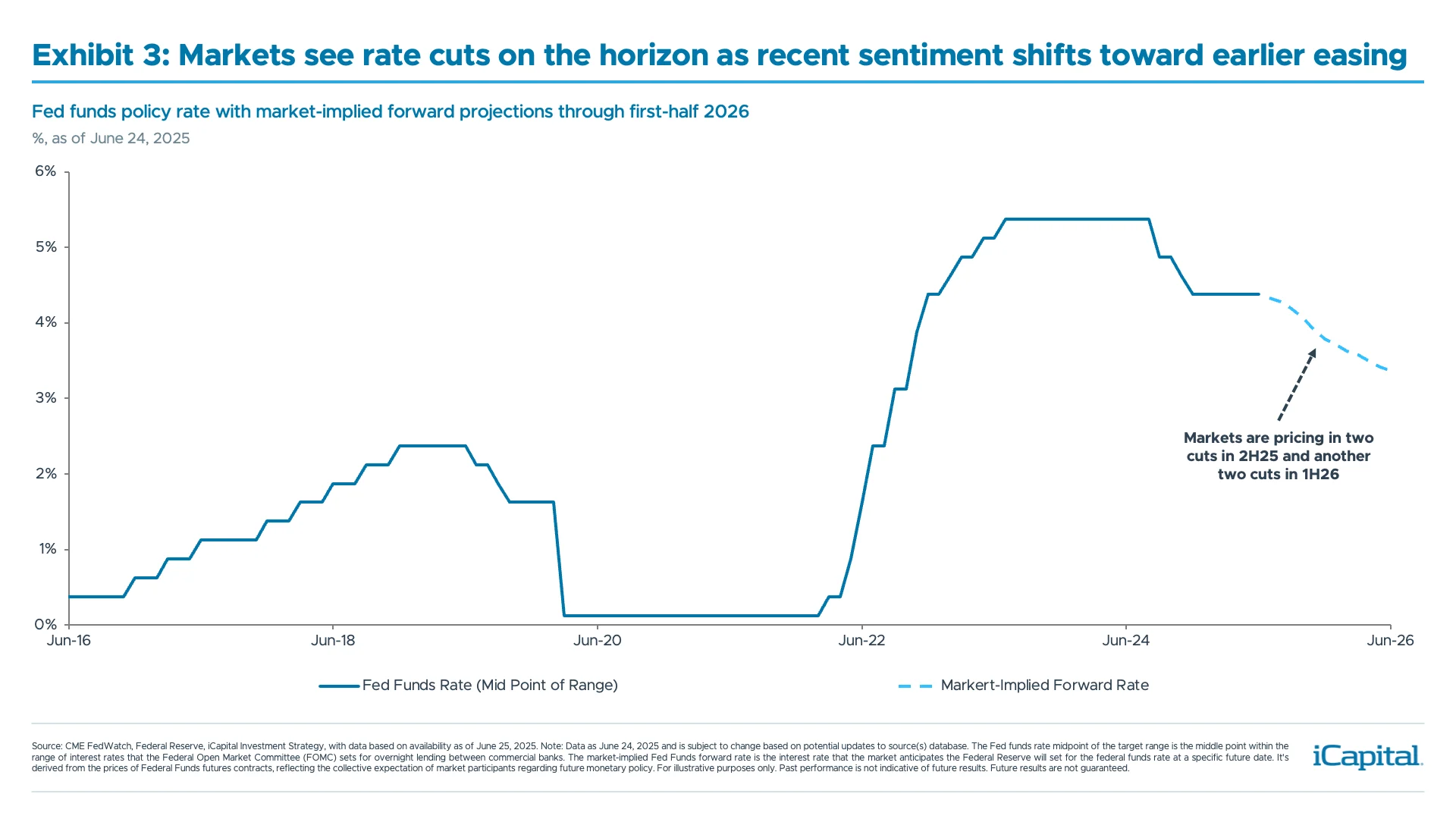

- Clarity on Fed Policy Path: Rate cuts – on the back of a soft-landing environment – would be a green light for deal activity, easing financing costs and encouraging capital deployment from both GPs and corporates. While immediate cuts aren’t essential, a clear, well-telegraphed signal from the Fed on when they plan to restart their easing cycle would provide confidence to underwrite deals. While Powell has emphasized patience, noting the Fed is “well positioned to wait,” more dovish voices like Governor Waller and Bowman have hinted at wanting to cut sooner.11 As it stands, markets are pricing in roughly two cuts in 2025, starting around the September or October FOMC meeting, with another two expected in the first half of 2026 bringing the Fed Funds rate down 100 basis points, to a 3.25-3.50% target range (Exhibit 3).12 However, the exact timing keeps shifting, and until there’s a clearer and more concrete timeline, deal momentum may remain relatively soft.

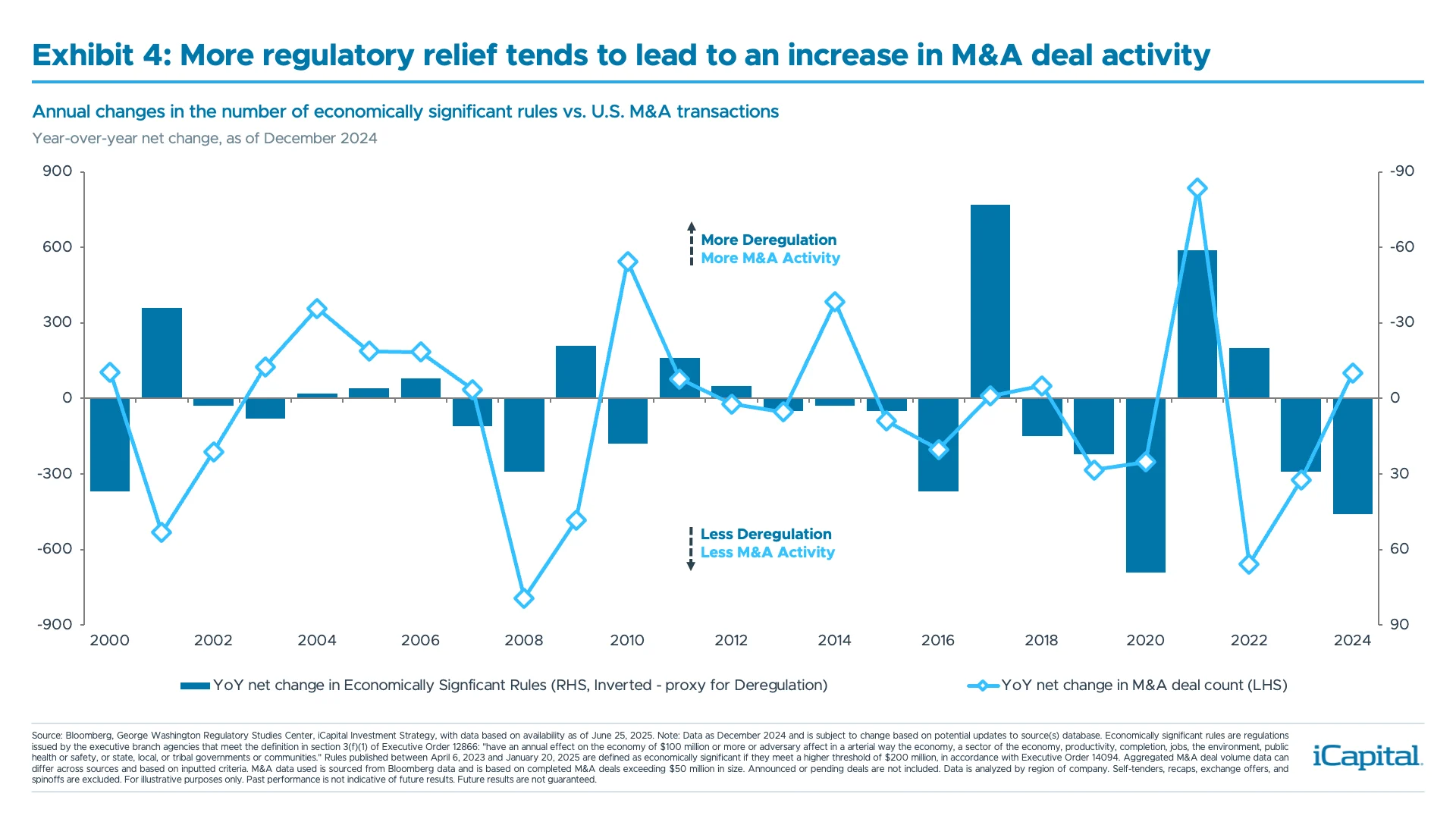

- Regulatory Relief: While Trump’s second term has so far largely focused on trade and tax policy, pro-growth deregulation and regulatory streamlining will likely become a focal point in the months ahead. A return to a lighter-touch regulatory regime – similar to Trump’s first term, which saw the fewest economically significant rules enacted since Reagan – could provide a meaningful tailwind to dealmaking (Exhibit 4).13 Notably, back in January, Trump signed an executive order requiring agencies to repeal ten existing regulations for every new one introduced – signaling a broader deregulatory agenda.14 And more recently, financial sector deregulation is becoming noteworthy, especially in light of reports that regulators may plan to reduce the enhanced supplementary leverage ratio (eSLR) by up to 1.5 percentage points.15 This could free up bank balance sheets, enabling increased lending and supporting deal activity. And combining that with the potential for faster, more transparent antitrust approvals, these changes could significantly boost both M&A and IPO activity.

- Valuation Stabilization: Despite April’s brief volatility spike, valuations in both public and private markets have largely rebounded from their 2022–23 lows and are stabilizing near pre-pandemic (2017-19) norms, signaling that the valuation reset from higher rates and inflation is largely complete.16 This normalization is providing more realistic and sustainable pricing. For dealmaking, stable valuations are critical for narrowing the gap between buyers and sellers in M&A transactions and for determining the attractiveness of IPOs. Firming valuations not only support pricing but also restore confidence in growth projections and exit strategies.

If these factors align, we’d expect a pickup in deal activity, especially as CEO and business confidence rebounds – a key missing ingredient. Indeed, our iCapital Business Optimism Barometer remains below average but is showing early signs of improvement and may be poised to improve further in the coming months (Exhibit 5).17 And from where we sit, there are reasons for optimism: M&A conversations and announcements are picking up, IPO pipelines are building, and financing is becoming more accessible. A shift in sentiment would likely precede a meaningful uptick in deal flow.

What Sectors Could Lead?

As conditions improve, we expect the initial pickup in activity to be concentrated in sectors with strong secular growth narratives, before broadening out more meaningfully.

Tech, AI, and AI adjacent verticals including digital infrastructure, automation, and AI Power remain the clearest leaders in our view. Investor interest and deal momentum continue to build in these areas thanks to long-term innovation tailwinds and strong fundamentals. Indeed, Tech M&A reached a near three-year high in Q1 202518, and with mega-cap tech firms sitting on north of $250 billion in net cash19, there’s ample firepower to pursue strategic acquisitions in the months and quarters ahead. On the IPO front, AI-linked names have been among the most active and best-performing listings this year – a clear signal that capital markets are open for the right stories.

Beyond tech, rising conviction in healthcare and life sciences innovation as well as continued momentum in the energy transition vertical could also drive a pick-up in activity. In healthcare specifically, with valuations reset and the FDA approval backlog beginning to clear, both IPOs and M&A deal flow could see renewed strength.

Positioning for What’s Ahead

For investors looking to capitalize on a pick-up in deal activity, we see compelling opportunities across both public and private markets. In public markets, large-cap banks, specifically those with significant exposure to capital markets and M&A advisory, stand to benefit directly from an uptick in transaction volumes. We also see opportunities within public alternative asset managers, which are well-positioned to capture upside from a broader pickup in fundraising, deployments, and exits.

In private markets, we’d favor GPs deploying capital into high-growth and secular themes like AI, automation, and digital infrastructure – areas where we expect deal activity to accelerate most notably. And in private markets the setup is particularly compelling given structural tailwinds. GPs currently own roughly 12,000 companies and face mounting pressure to exit portfolio companies and return capital to investors.20 And with a near record of $3.9 trillion of dry powder across private capital that should provide support for deal activity once conditions improve.21

We also would reiterate our view from earlier in the year on Event-Driven Hedge Funds, which historically see strong returns during periods of rising M&A activity.

Bottom Line: A Shift Is Coming

We’re not calling for a 2021-style deal frenzy, but we do believe a meaningful and sustained lift in transaction volumes is on the horizon. Pent-up demand from the past 4–6 quarters, initially expected to materialize in early 2025, has been pushed out/back by recent market turbulence – but importantly, not canceled/erased.

The exact timing hinges on a multitude of factors, but the conditions for a broad pickup are steadily aligning. We see momentum building in the latter part of Q3, as we move past the typical summer lull, with a more pronounced inflection higher likely in Q4 and into 2026.

The point is – the appetite is there. It’s just waiting for the right moment to be released.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025. Note: Aggregated M&A deal volume data can differ across sources and based on inputted criteria. M&A data used in this commentary is sourced from Bloomberg data and is based on completed M&A deals exceeding $50 million in size. Announced or pending deals are not included unless otherwise noted. Data is analyzed by region of company. Self-tenders, recaps, exchange offers, and spinoffs are excluded.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025. Note: Aggregated M&A deal volume data can differ across sources and based on inputted criteria. M&A data used in this commentary is sourced from Bloomberg data and is based on completed M&A deals exceeding $50 million in size. Announced or pending deals are not included unless otherwise noted. Data is analyzed by region of company. Self-tenders, recaps, exchange offers, and spinoffs are excluded.

- PitchBook | LCD, Morgan Stanley, as of June 25, 2025.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025. Note: Aggregated IPO data can differ across sources and based on inputted criteria. IPO data used in this commentary is sourced from Bloomberg data and is based on U.S. exchange-listed IPOs that have priced, are currently trading, and have market caps of at least $25 million. Closed-end funds, unit offerings, and SPACs are excluded.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025.

- CNBC, “Lutnick says 10% baseline tariff will stick around for “foreseeable future”, as of May 11, 2025.

- Goldman Sachs, as of April 23, 2025.

- Bloomberg News, Wall Street Journal, Reuters, as of June 25, 2025.

- CME FedWatch, as of June 25, 2025.

- The George Washington University Regulatory Studies Center, Office of the Federal Register, Office of Information and Regulatory Affairs, as of Mar. 1, 2024.

- The White House, “Unleashing Prosperity Through Deregulation”, January 31, 2025.

- Bloomberg News, as of June 17, 2025. Note: The proposal would lower a bank holding company’s capital requirement under the enhanced supplementary leverage ratio by up to 1.5 percentage points to a range of 3.5% to 4.5%, down from the current 5%.

- Bloomberg, iCapital Investment Strategy Analysis, as of June 25, 2025.

- Business Roundtable, Chief Executive Magazine, Duke University’s Fuqua School of Business, Federal Reserve Bank of Dallas, Federal Reserve Bank of Kansas City, Federal Reserve Bank of New York, Federal Reserve Bank of Richmond, Federal Reserve Bank of Philadelphia, Federal Reserve Bank of Chicago, National Federation of Independent Business, iCapital Investment Strategy, with data based on availability as of June 24, 2025. Note: Data as of May 2025 and is subject to change based on potential updates to source(s) database. The iCapital Business Optimism Barometer is a composite leading measure designed to offer forward-looking insights into underlying trends in U.S. business confidence. It draws on 14 key indicators including Dallas Fed Texas Service Sector Outlook Survey - General Business Conditions 6mo Ahead, Dallas Fed Texas Manufacturing Outlook Survey - General Business Conditions 6mo Ahead, Kansas City Fed Manufacturing Survey - Composite Index Expected in Six Months, Kansas City Fed Service Sector Survey - Composite Index Expected in Six Months, FRBNY U.S. Empire State Manufacturing Survey - General Business Conditions 6mo Ahead, FRBNY Business Leaders Survey - Business Climate Expected in Six Months, Richmond Fed Services Sector Activity Survey - Expected Local Business Condition, Philadelphia Fed Business Outlook Survey - General Business Conditions 6mo Ahead, Chicago Fed Survey of Economic Conditions - 6-12 Mo Outlook for U.S. Economy, U.S. Duke CFO Survey - Optimism about the U.S. Economy, U.S. Duke CFO Survey - Optimism About Own Company, Chief Executive Magazine CEO Confidence Index - Confidence in the Economy 1 Year from Now, U.S. Business Roundtable CEO Survey Economic Outlook Index, NFIB Small Business Optimism Index - Outlook for General Business Conditions. Given the indicator’s structure, the focus should be on overall trends rather than short-term fluctuations or specific levels at any given time.

- PitchBook | LCD, “Q1 2025 Global M&A Report”, as of April 29, 2025.

- Morgan Stanley, as of June 6, 2025. Note: Mega-cap tech firms include those with market caps greater than $200 billion.

- PitchBook | LCD, iCapital Alternatives Decoded, as of April 30, 2025.

- Preqin, iCapital Alternatives Decoded, as of April 30, 2025.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2025 Institutional Capital Network, Inc. All Rights Reserved.