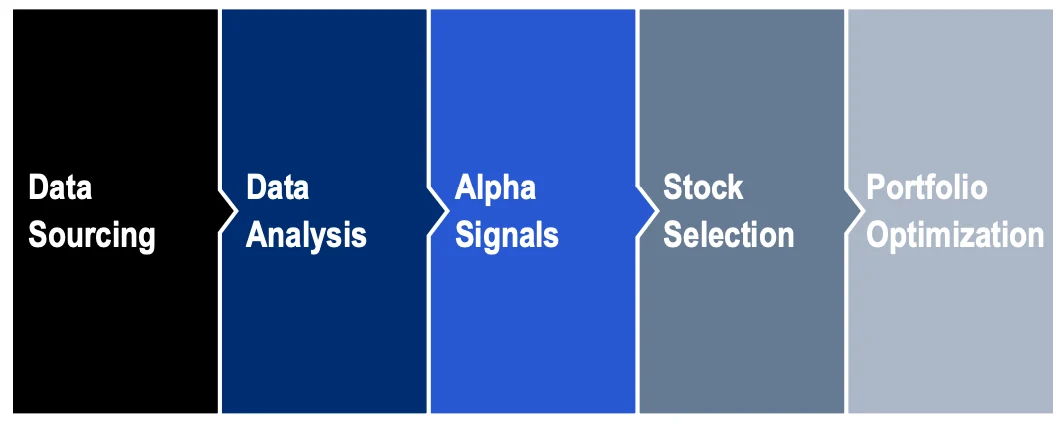

What is Quantitative Investing?

Quantitative equity hedge funds use statistical analysis and computer algorithms to identify and exploit market opportunities. These strategies analyze large, complex datasets to develop ‘alpha signals’ or ‘models’ which the fund manager employs to systematically capture pricing inefficiencies and market anomalies. These funds then use automated trading systems to execute long and short positions, and optimization techniques to construct diversified portfolios.

In this way, a fund manager can apply an objective, rules-based approach for strategy implementation, removing any emotional bias from the process. These strategies can analyze a broader range of stocks than a traditional, fundamental approach and at greater speed. By exploiting technology and statistical algorithms to process a multitude of inputs across a diverse range of stocks, sectors and geographies, these funds typically hold hundreds or even thousands of positions. Outperformance is a function of many small, profitable trades, each of which meet defined criteria, which ideally add to the consistency and predictability of the strategy.

Source: iCapital; for illustrative purposes only

Market Backdrop and Recent Outperformance

The market backdrop from 2023 to 2025 was conducive to a range of hedge fund strategies. Perhaps unsurprisingly, as the era of easy money came to an end, uneven global growth and a volatile geopolitical environment created trading opportunities across numerous asset classes and geographies. This was particularly true in global equity markets. Dispersion, a measure of the spread of performance among stocks, continued to trend higher, while at the same time correlations between stocks sharply declined. These moves reflected investors’ decision to further distinguish between stronger and weaker companies, broadening the opportunity set and improving the odds of success for long/short equity managers.

Quantitative equity hedge funds were among the leading beneficiaries during this period. Through their broadly diversified portfolios, these funds have taken advantage of this backdrop to generate attractive absolute and risk-adjusted performance utilizing a long/short portfolio construction process. This has contributed to a period of increasing outperformance by quantitative equity hedge funds relative to a traditional global balanced portfolio.

Outlook

While the recent market backdrop has been supportive of quantitative equity hedge funds, the outlook for these strategies is equally compelling. As noted earlier, data provides the ‘raw material’ for quantitative strategies, and the amount of data available for collection and analysis continues to grow exponentially. Typically, quantitative managers broadly classify their data sources as being fundamental, technical or ‘alternative’. The alternative category is where most newer data sets are being discovered — examples include social media activity, satellite imagery, webpage scraping, weather patterns, smartphone app data and others.

Given this volume of data and the speed at which it is being created, the most successful quantitative equity hedge funds devote substantial resources to data management. These firms often employ hundreds of professionals — many with PhDs in mathematics, engineering, and computer science — who are responsible for identifying, collecting and cleaning data. Additionally, the leading managers are increasingly using artificial intelligence (‘AI’) and other machine learning techniques to gather and organize ‘unstructured’ data. Relative to humans, AI programs are better equipped to quickly and efficiently identify relationships between seemingly disparate sources. This enables managers to tap into an even broader range of data inputs as they look to extract differentiated alpha signals and drive outperformance. That said, while AI is likely to play an ever-growing role in implementing quantitative strategies, human input is still needed to develop the high-quality hypotheses and models which guide the AI programs.

Of course, no strategy is foolproof and even the most sophisticated AI-driven strategies can fail to live up to expectations. For example, machine learning models can be extremely powerful in their use of historical data but may still be unable to adapt to real world conditions because of ‘overfitting’, which results in a model being overly optimized for historical data. In other words, a model can identify alpha signals that are specific to historical data, rather than capture signals that are more appropriate to current market conditions. Quantitative strategies can also be prone to underperformance during severe market dislocations, when market correlations often surge and historical alpha signals are less likely to be relevant.

Conclusion

Market conditions ebb-and-flow over time, and various hedge fund strategies perform differently during changing market environments. Given the prevailing market backdrop, quantitative equity hedge funds can provide differentiated and complimentary sources of return to an investor’s overall equity allocation. In a volatile market, these funds offer broad diversification, enabling them to take advantage of increased dispersion and lower correlation among individual stocks. An added advantage is that these funds also tend to be relatively liquid with investor friendly liquidity terms – many on a monthly basis. And with decades of experience and extensive resources, the leading quantitative firms are increasingly harnessing the power of AI as a core component of their investment process.

These technological advancements, combined with the explosion of data globally, create both a growing opportunity set and a competitive advantage for established players looking to deliver superior absolute and risk-adjusted returns for investors.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2026 Institutional Capital Network, Inc. All Rights Reserved.