Key Takeaways:

- Recent dislocation in private credit and among software borrowers has many advisors and investors asking about the private equity invested in these companies.

- Private credit and private equity should be evaluated differently: credit prioritizes downside protection, while equity accepts risk in pursuit of upside.

- In private credit, rising non-accruals and softer marks point to select stress in select cases, but most markdowns reflect pricing changes not borrower deterioration.

- In private equity, stress can be tolerated as diversified portfolios are structured to absorb underperforming investments.

- Advisors should focus diligence on stressed holdings by asking targeted questions about non-accruals, valuation methodology, portfolio weight, and exit or improvement plans.

Recent dislocation across private credit and software-driven investments has led to a noticeable increase in advisor questions around “problem investments.” In particular, concerns have emerged about whether deals underwritten during the 2020–2022 period—when valuations peaked and capital was abundant—are now beginning to deteriorate.

These concerns are understandable, but the reality is more nuanced. Risks are beginning to surface, but they are concentrated rather than systemic. And outcomes differ meaningfully across private credit and private equity structures because credit is designed to minimize losses, while equity seeks excess returns and accepts greater risk. For advisors, the objective is not to avoid these exposures altogether. Rather, it is to correctly interpret what is happening beneath the surface—distinguishing market-driven valuation pressure from true deterioration—and to focus diligence where it matters most.

Asset managers continue to report stable fundamentals, but signs of stress are emerging in select companies. The key is distinguishing between market-based valuation changes and borrower-specific risk, while also asking practical questions about exposure tied to these high-valuation vintages. Together, these factors provide a practical framework for evaluating how managers identify and manage challenged investments.

Peak valuation deals: Understanding “vintage risk”

History shows that investing at elevated valuations can lead to losses. Between 2020 and 2022, low interest rates and strong demand for growth drove software valuations to record highs—often exceeding 15x revenue. (Exhibit 1). When valuations were inflated, so too were the amounts of debt financing used to support them. Software deals completed at these peak valuations have become vulnerable now that the valuations have compressed.

Many acquisitions from that period are now effectively “underwater” on paper, meaning they would sell for less than their original purchase price. This is known as “vintage risk”: capital invested at elevated valuations, especially in concentrated markets, may produce weaker returns over time.

Two indicators of stress in credit portfolios

These challenges aren’t just theoretical—there are real signs of stress in private credit portfolios, reflected in non-accruals and fair value marks:1

Rising non-accruals: One key measure is non-accrual status, or when a lender stops recognizing the income from missed interest payments. In Q1 2026, approximately 3.2% of private credit portfolios were on non-accrual, up 70 basis points2 in the non-accrual rate in just three months. (Exhibit 2)

While well under the 6.0% reached in 2020, we believe non-accrual status is a useful proxy for potential realized losses and signals that more borrowers are experiencing meaningful stress. Loans made at peak valuations—where valuation compression has been most pronounced—are one driver of the recent uptick.

Loan fair value marks: Another signal is how private credit funds are periodically marking (i.e., valuing) their loans. In our analysis of 6,000 loans, software loans have seen the sharpest markdowns. As of Q1 2026, large private credit funds have marked software loans to 97.4% of cost, down roughly two percentage points from the end of 2025 (Exhibit 3). Non-software loans declined more modestly to 99.1% from 99.8%. Software represents 15% to 20% of direct lending portfolios.3

Importantly, a markdown does not necessarily reflect a deterioration in credit quality or imply that a loss will occur. Changes in market rates or spreads can reduce a loan’s fair value even when the underlying borrower remains financially sound. Most Q1 2026 markdowns reflect pricing adjustments, not fundamental weakness, with pressure more concentrated in areas like software. In short, this is market-driven, not broad-based credit stress.

Assets held by private credit vs private equity: assessing the risks

If some of these companies do falter, who shoulders the risk—lenders or equity investors? In a typical sponsor-based deal, debt sits higher in the capital structure and has priority in repayment, while equity sits at the bottom and absorbs losses first. Senior secured loans, particularly first lien, are designed to protect lenders in downside scenarios.

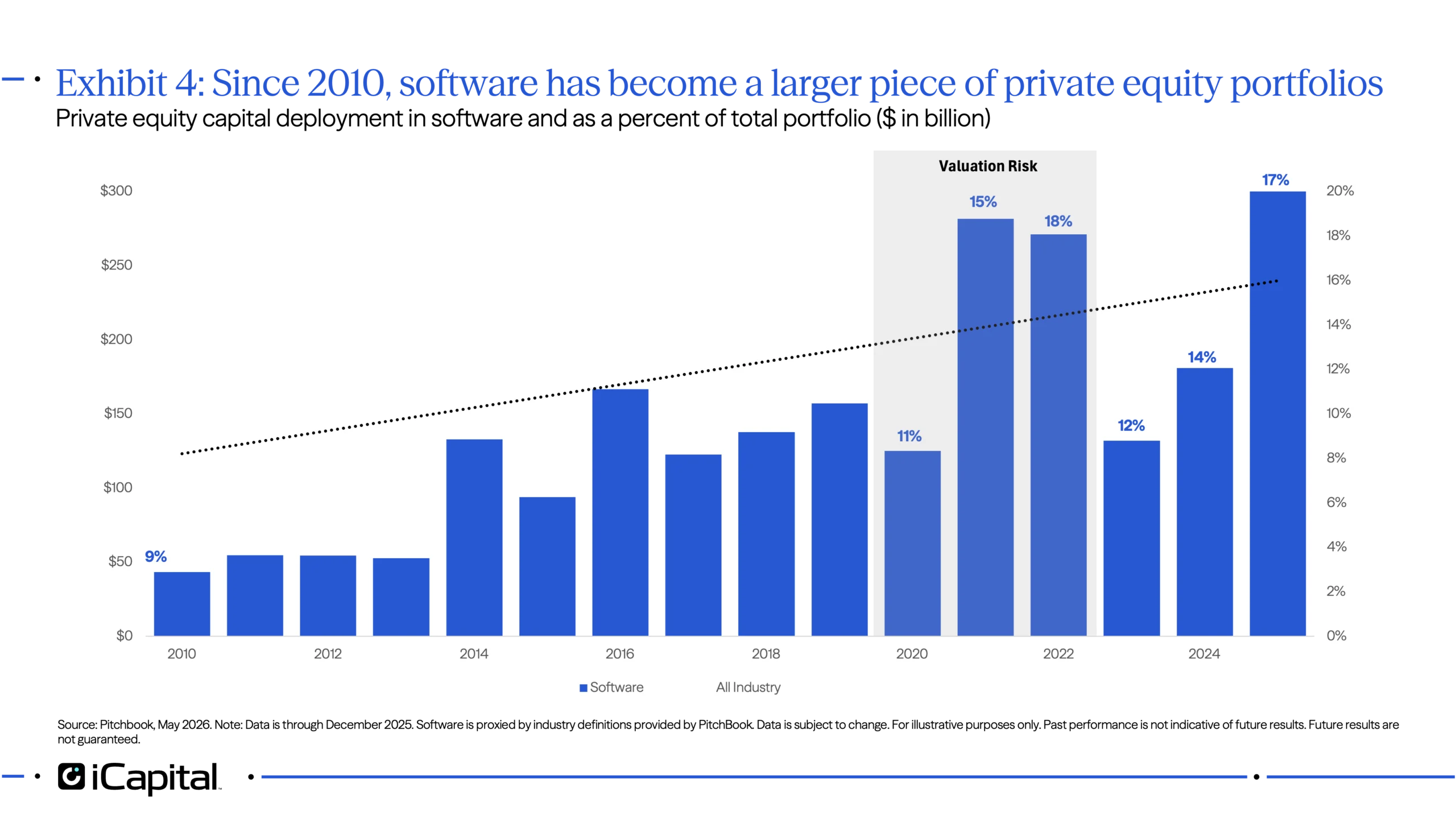

At the same time, software has become a bigger piece of private equity portfolios. In 2021, approximately 15% of private equity capital was deployed into software, up from about 10% over the prior decade. (Exhibit 4). In fact, private equity investment in these companies is roughly double that of private credit.

This is where it’s important to look at investments through the appropriate lens.

Private equity investors accept more risk in pursuit of higher returns. An equity fund can afford a few bad investments as long as they have a diversified portfolio with other winning investments that, in aggregate, deliver outsized returns. This, of course, depends on the fund strategy. For example, a concentrated portfolio with large investments does not have the same latitude to absorb losses. On the other hand, a private credit fund return is capped at interest payments and repayment at par and does not have upside potential to offset losses.

Consequently, a private credit manager’s main goal is to avoid losses because the fund can’t “offset” it with excess returns elsewhere. This fundamental difference drives how each type of strategy approaches investments.

- Private credit managers focus on downside protection—they structure deals conservatively, as senior-secured investments with covenants and low loan-to-value ratios precisely to avoid losses. And, when losses do occur, the debt captures whatever value is left over in the company. If funds avoid defaults and maximizes recovery value, their returns should be steady and reliable.

- Private equity managers, conversely, accept that some investments may not work out. Their goal is to generate enough “alpha,” or outperformance, from successful investments to more than offset losses elsewhere in the portfolio.

Given this context, it’s easier to understand why sentiment in equity and credit markets is different. Equity deals underwritten at an inflated valuation may not have a clear exit path today, but they have a longer timeframe to nurture investments and often have a controlling stake to help with value creation. There will also be many portfolio companies that adapt, seeking to drive value in an AI-native era. In those cases, equity holders capture all the upside as companies succeed and grow into their valuations.

A framework for evaluating problem investments

When evaluating investments on non-accrual or experiencing valuation pressure, advisors can apply a structured approach. This framework, backed by a set of targeted questions, can help advisors and investors with visibility to underlying investments and portfolio health.

Final takeaway

For advisors, the cross-asset view is clear: Risks tied to inflated valuations are real—but not uniform. We believe private credit portfolios remain broadly stable, while private equity portfolios retain upside potential from true credit deterioration and evaluating credit and equity through their respective risk framework. Today’s environment requires sharper questions—not broader assumptions.

1. Fair value is generally defined as the price that would be received to sell an asset in an orderly, arm’s length transaction.

2. Note: a basis point is a hundredth of 1%.

3. iCapital analysis of SEC filings of private credit funds.

INDEX DEFINITIONS

IGV iShares Expanded Tech-Software Sector ETF: The iShares Expanded Tech-Software Sector ETF seeks to track the investment results of an index composed of North American equities in the software industry and select North American equities from interactive home entertainment and interactive media and services industries.

S&P BDC Index: The S&P BDC Index is designed to track leading business development companies that trade on major U.S. exchanges.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax, and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit from an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection, or forecast on the economy, stock market, bond market, or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third-party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2026 Institutional Capital Network, Inc. All Rights Reserved.