The last day of January was everything the rest of the month wasn’t – stocks were up, the Nasdaq led the gains, and Cathie Wood’s ARK Innovation ETF (ARKK—the poster child for high-multiple, high-promise, as-yet-unprofitable tech, i.e. speculative or “spec” tech) was up 9.5%.1 After a major reset, could this bounce be a sign of things to come in February? Could the Nasdaq bounce and could “spec tech” outperform?

Broadly, January’s sell-off cleared a lot of pandemic-era froth – in valuations and positioning. For example, the Nasdaq forward price-to-earnings multiple reset to 26.5x from a peak of 34x on January 26, 2021.2 Tech became an underweighted sector. The Federal Reserve’s more hawkish tone caused a repricing higher in yields. Now with this needed reset behind us, we are starting with a much cleaner slate and can focus on the positives.

One such positive is the return in February of the largest buyer in the markets—corporates making discretionary share buybacks. Most of the S&P 500 was in a blackout period until January 24 due to earnings reporting requirements, but by the end of this week 70% of S&P 500 market cap is projected to be out of blackout.3 This number will rise further in the coming weeks. Given the degree of corrections in many stocks, many companies may accelerate buyback plans. Corporate buybacks are expected to reach $872 billion in 2022, outpacing last year’s $808 billion.4 This could be a significant source of support for the markets, starting this month.

Can “spec tech” also bounce back? In the short term (the next few weeks or months), it is overdue for a tactical bounce and potentially a short squeeze; in the medium term (the duration of the Fed tightening cycle) we do not expect the space to be a big outperformer; in the long term (three years-plus), we believe these companies could become profitable, grow into their valuations, and outperform as a result. Here are some reasons why.

Short term: “Spec tech” is due for a tactical bounce

Short term: “Spec tech” is due for a tactical bounce

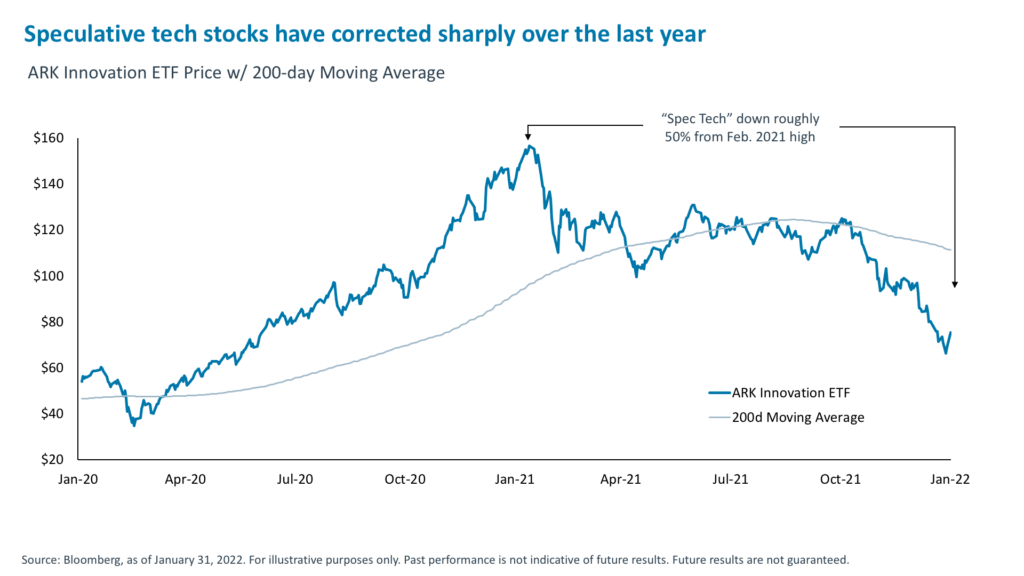

Despite the S&P 500 barely correcting 10%, ARKK—taken as a proxy for “spec tech”—is roughly 50% lower than its 52-week high in mid-February 2021.5 Last week, technical indicators on the ARKK fund screened as oversold, as they last did in March 2020. The fund’s options skew—a measure of fear in the market—was in the 92nd percentile over the last five years.6 Its median stock multiple, as measured by price-to-sales, fell from 14.3x on November 9, 2021, to 8.2x as of January 31, only slightly higher than the 6.5x recorded back on April 9, 2020.7

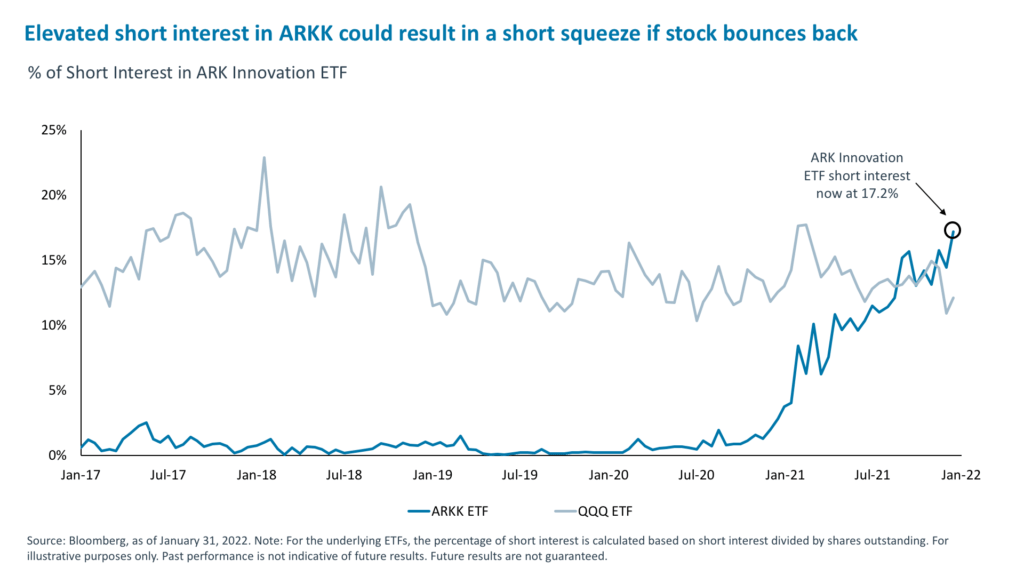

As a result, the median stock in the fund is now forecast to have 86% upside to the consensus analyst price target.8 Sure, another bout of Fed-induced uncertainty could pressure valuations further but without a Fed meeting until March, and given the reset in prices and outflows from growth stocks in January, a tactical bounce is likely. Finally, short interest in ARKK is at a record 17%, against 12% for the Nasdaq 100. In the event of a tactical bounce, it could force those with short positions to close them out, causing a short squeeze and pushing the price up further.9

Medium term: Tightening cycle caps outperformance potential

Medium term: Tightening cycle caps outperformance potential

The big driver of outperformance of “spec tech” has been the rise in valuations, which more than doubled from April 2020 to November 2021.10 A valuation re-rating should not be expected amid a Fed tightening cycle. History suggests that multiples typically stay either range-bound or compress somewhat (we wrote about this in our 2022 Outlook).11

This implies that earnings will have to rise to spur a resurgence. However, many high-promise innovation-based stocks remain unprofitable. For example, the median stock in the ARKK ETF had adjusted earnings per share (EPS) of negative $0.34, and if you exclude Tesla, Zoom, Coinbase, and Shopify, it falls to negative $0.41.12

The burden therefore falls on revenue growth to drive performance. However, revenue growth could slow for many “spec tech” stocks over the next couple of years because the pull forward in demand spurred by the pandemic is likely not repeatable. Coupled with uncertainties around multiples, we would not expect a repeat of their 2020 outperformance. Finally, equity returns for factors such as growth, momentum, risk, and small-cap—which are applicable to many “spec tech” stocks—tend to be muted during the tightening phase of the cycle, with little differentiation between these factors.13

Longer term: Bullish on expectation that companies grow into their valuations

Despite the recent underperformance, it should be noted that themes like gene therapy, automation and robotics, artificial intelligence, Web 3.0, and fintech innovation, among others, are not fads but long-term secular themes that are already changing and shaping our future. Companies that are building this future and are little known today could eventually become household names. However, for them to outperform they either need a tangible catalyst (like the pandemic was for many digital stocks) or time to grow into their valuations and turn from “spec tech” to “profitable tech”. Indeed, the ARK Innovation ETF’s median adjusted EPS is projected to improve from negative $0.34 to $0.00 by 2024.14

For investors focused on the longer term, we recommend buying into innovation stocks when their price drops and more broadly staying the course, but being prepared for periodic pullbacks after period of outperformance. Of course, stock and/or fund selection is still key to long-term success. We also recommend looking to private markets. Venture capital-backed companies are accessing the same innovation megatrends but even earlier in the companies’ lifecycle, thereby capturing more of their hypergrowth phase. This is why venture capital is one of our top investment ideas for hypergrowth in 2022. For a more detailed analysis, please see our 2022 Outlook.

1. Bloomberg, as of January 31, 2022.

2. Bloomberg, as of January 31, 2022.

3. Goldman Markets Division, January 31, 2022.

4. Compustat, Goldman Sachs Investment Research, as of December 2, 2021.

5. Bloomberg, as of January 31, 2022.

6. Bloomberg, as of January 26, 2022.

7. iCapital Investment Strategy, Bloomberg, as of January 31, 2022

8. iCapital Investment Strategy, Bloomberg, as of January 31, 2022

9. Bloomberg, as of January 31, 2022.

10. Bloomberg, as of January 31, 2022.

11. iCapital Investment Strategy, Bloomberg, as of December 31, 2021

12. iCapital Investment Strategy, Bloomberg, as of January 31, 2022

13. Bank of America Quantitative Research, as of January 28, 2022

14. iCapital Investment Strategy, Bloomberg, as of January 31, 2022

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by iCapital, Inc. (“iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer to sell, a solicitation of an offer to purchase or a recommendation of any interest in any fund or security. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation. This material does not intend to address the financial objectives, situation or specific needs of any individual investor. Alternative investments are complex, speculative investment vehicles and are not suitable for all investors.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2023 Institutional Capital Network, Inc. All Rights Reserved.