Kevin Warsh and the AI Economy

Kevin Warsh’s first FOMC press conference focused less on a single rate decision and more on a broader question: is the Fed’s toolkit still fit for an economy being rewired by artificial intelligence?

The Fed’s new agenda is an AI agenda

His answer lies in the task forces he unveiled. Three of the five are AI-focused: productivity & jobs, inflation frameworks, and data. The overlap is no accident. AI is already reshaping capital spending, power demand, semiconductor prices, software costs and business formation. The harder question is whether official data can distinguish a true productivity boom from a temporary investment surge alongside a shrinking labor force.

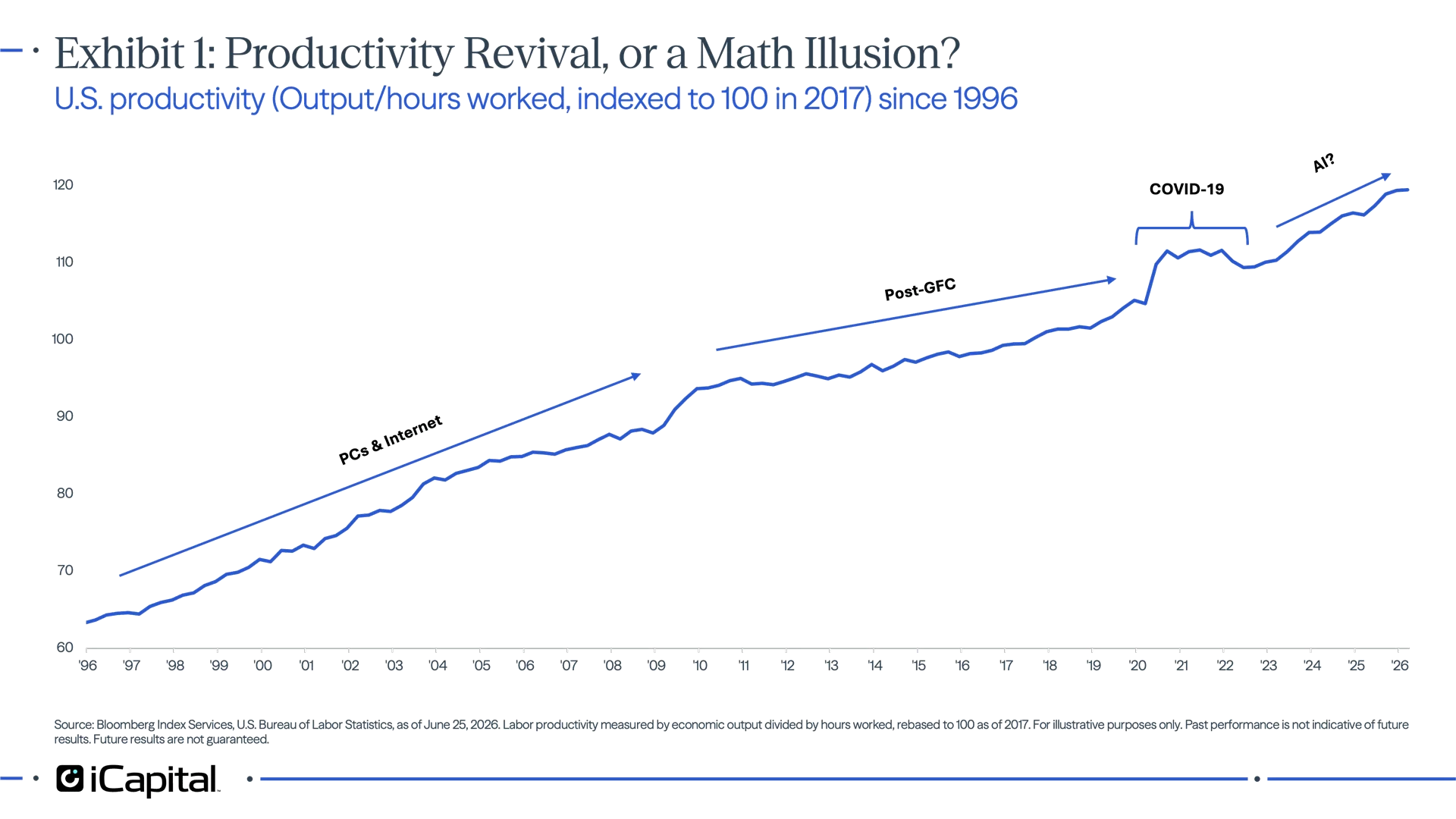

Productivity is simple in theory, slippery in practice

Productivity is the most elusive of the three. In theory, it measures how much more output a worker can produce in the same hour, the payoff from education, training and technology. In practice, it is just the plug connecting GDP—or output —to total hours worked, which makes real gains hard to separate from quirks in the data. The pandemic is the cleanest example: productivity surged not because anyone became more efficient, but because GDP didn’t fall by as much as hours worked.

Too early to measure AI productivity

A similar dynamic is at work today. Since 2022, productivity has improved faster than during the 2010-2018 post-Global Financial Crisis period (Exhibit 1). While it’s tempting to attribute this to AI, a more likely driver is heavy upfront infrastructure spending boosting growth, just as demographics and tighter immigration slow job creation. Strong output divided by slow hours flatters the math, whether or not anyone is working smarter. Fewer jobs lost, more inflation gained

Fewer jobs lost, more inflation gained

Until AI’s benefits broaden, productivity measures anchored in GDP and hours will continue to miss part of the story. That gap is colliding with real anxieties about job displacement, despite little evidence it is happening yet. Two surprises cut against the consensus, both central to the Fed’s outlook. AI appears to be displacing fewer jobs than feared, and stoking more near-term inflation than expected. We take each in turn.

Watching for Jobs

Consensus is AI will gut jobs, but there are near-term offsets

AI-driven productivity is a necessity, not a risk

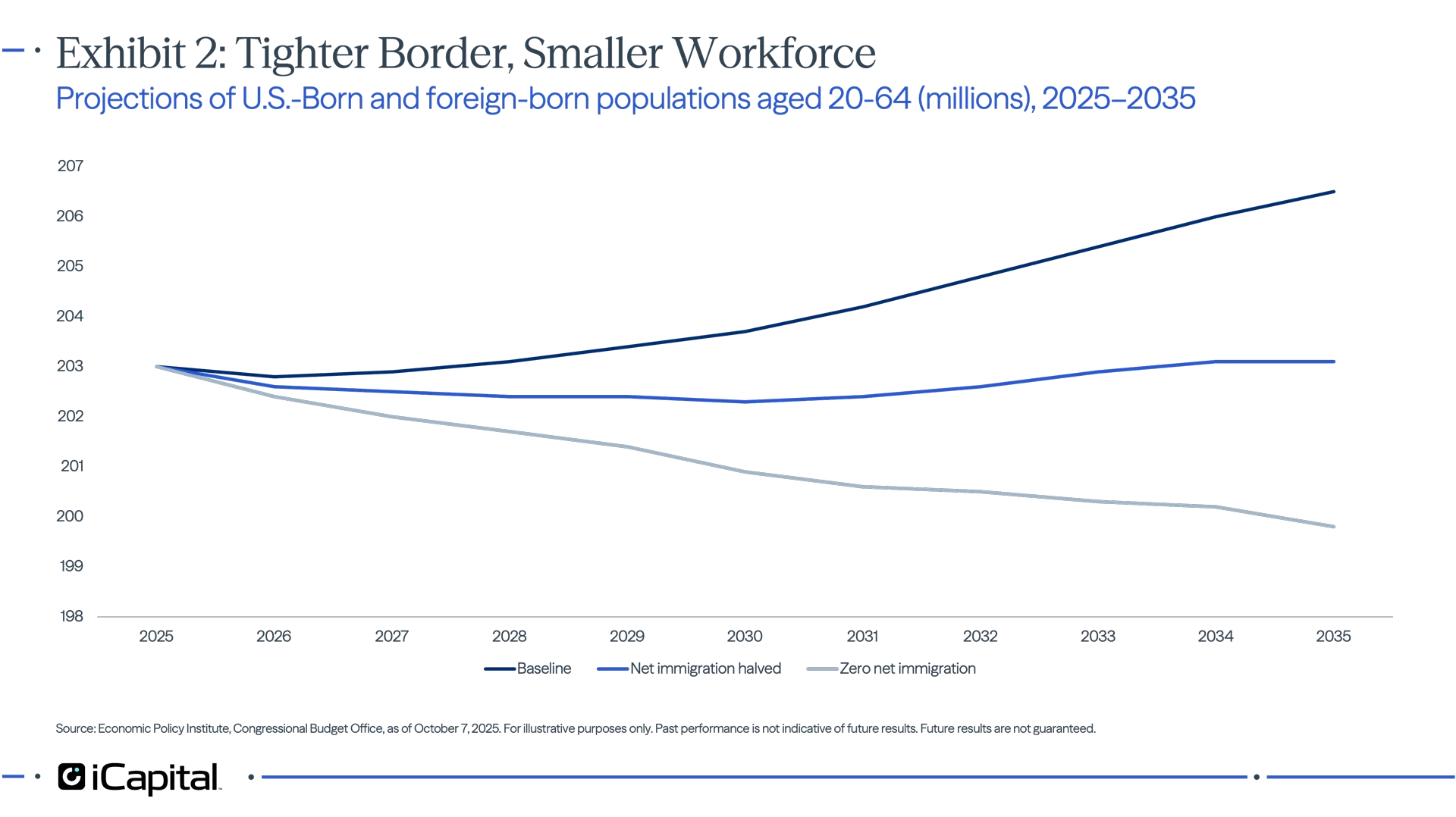

Before asking whether AI will destroy jobs, ask whether developed economies can afford not to lift productivity. Two-thirds of the world now lives in countries with fertility below replacement, and the US-born labor force is projected to shrink over the next decade as the baby boomer generation continues to retire in large numbers, accelerating the exit of experienced workers.1 2 Manufacturing alone faces 1.9 million unfilled jobs by 2033.3

At the same time, immigration policy has become more restrictive. In the US, net migration is projected to fall to 321,000 this year, down 90% from 3.3 million in 2023.4 Rather than replacing workers, AI is often filling roles that can’t be filled elsewhere.

Historically, a growing labor force was the primary driver of output growth. With the labor force potentially shrinking, productivity has to carry the load once borne by workers, and AI is the most plausible candidate to deliver it.

Historically, a growing labor force was the primary driver of output growth. With the labor force potentially shrinking, productivity has to carry the load once borne by workers, and AI is the most plausible candidate to deliver it.

Jobs and robot adoption can go hand in hand

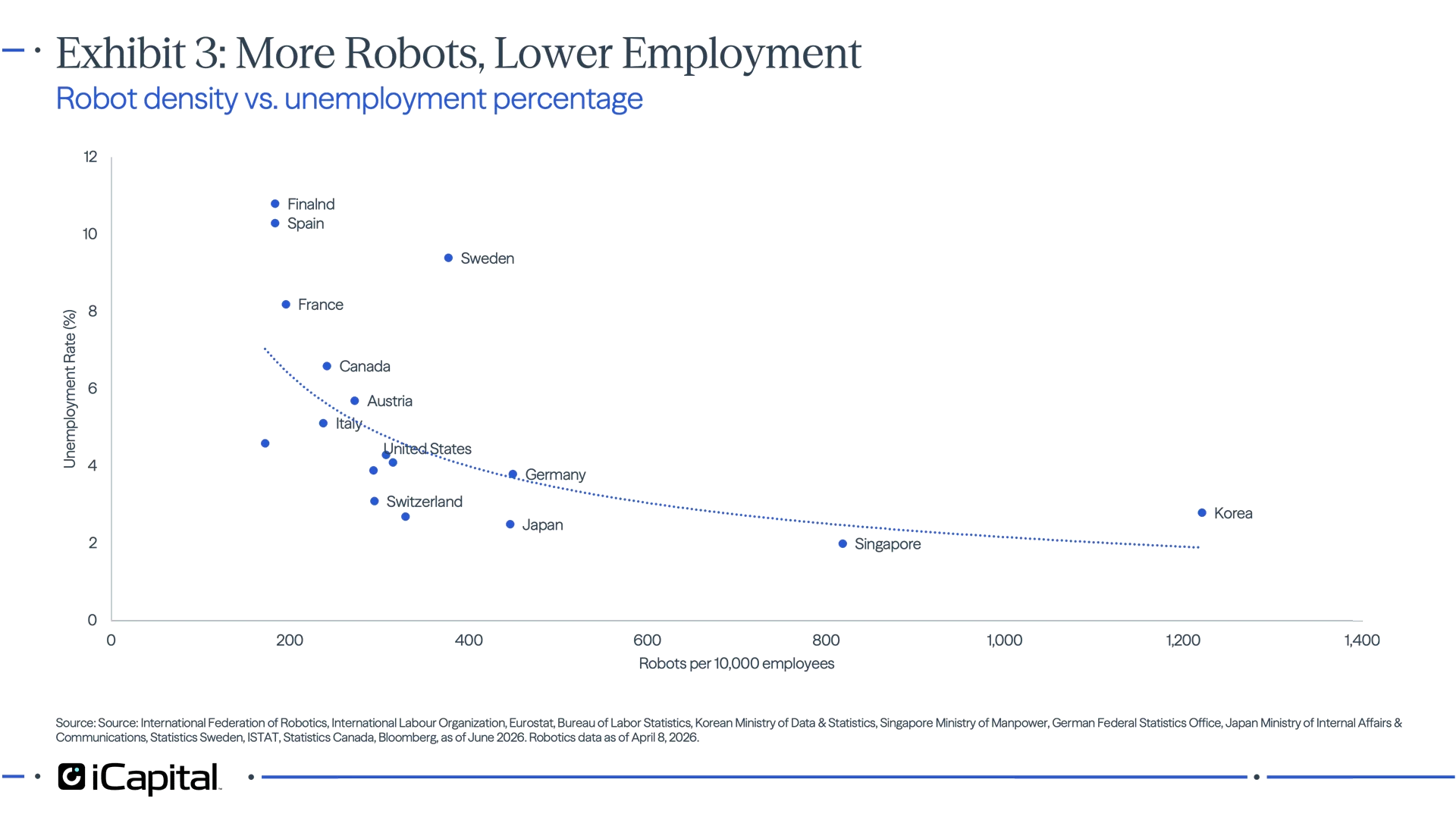

Blue-collar displacement is unfolding slowly. Robot density has roughly doubled over eight years but remains concentrated in automotive and electronics, which account for about 70% of all deployments.5 Physical AI, meaning robots that can operate in unstructured environments, remain in prototype. Until production scales and costs fall, physical automation will continue along the incremental path it has followed for decades.

Automation and employment often rise together. Amazon, the world’s second-largest private employer, operates more than 1 million robots alongside over 1.5 million workers.6 The countries with the highest robot density also have some of the tightest labor markets: South Korea (1,220 robots per 10,000 workers, 2.7% unemployment), Japan (446, 2.5%) and Germany (449, 3.7%) (Exhibit 3).

White-collar risk is real but overstated

White-collar risk is real but overstated

White-collar work faces the more immediate risk, though even that looks overstated. Yale’s Budget Lab found “no discernible disruption” in the labor market 33 months after ChatGPT’s launch, a finding that was supported by Anthropic’s research.7 A hard physical constraint reinforces that point. Wells Fargo estimates that replacing just 1% of workers would absorb roughly all the global compute capacity expected by the end of 2026.8

Call centers and entry-level knowledge work are the clearest near-term casualties, but across the economy the evidence points to augmentation rather than extinction. Where displacement does occur, white-collar workers adapt faster than blue-collar workers. Digital reskilling can take weeks to months, especially for younger workers, while becoming a licensed electrician or welder takes three to five years of hands-on apprenticeship.

AI is creating new work, not just replacing it

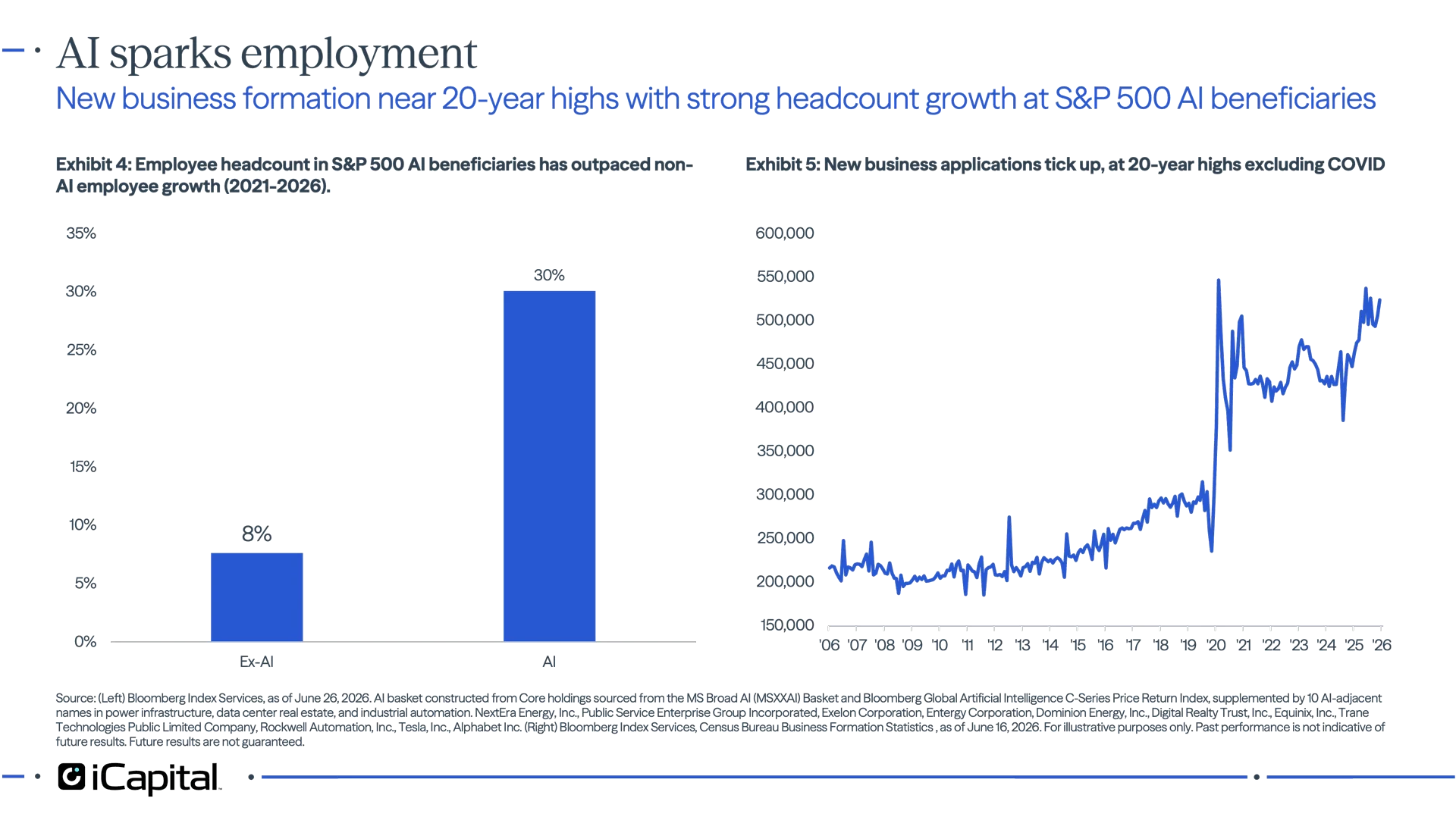

AI is creating employment through two channels: more hiring at the companies adopting it, and more new businesses able to form in the first place. On the first, AI-related S&P 500 companies have grown their workforce by 30% since 2021, versus 8% for the rest of the index (Exhibit 4). On the second, AI is compressing the fixed costs that once gated entrepreneurship—the legal, accounting, web, and administrative work that previously required hiring or expensive outside help—letting far more people cross from employee to founder. US business applications have roughly doubled, from about 3.5 million annually pre-COVID to more than 5.5 million, hitting non-pandemic highs in late 2025, with a growing share opportunity-driven rather than necessity-driven.9 Every one of those firms is a potential future employer.

History favors the optimists. MIT’s David Autor estimates that 60% of today’s jobs did not exist in 1940.10 Every prior automation wave, from ATMs to spreadsheets to medical imaging, has triggered a version of the Jevons Paradox: making work cheaper expands demand enough to offset the labor it saves.

History favors the optimists. MIT’s David Autor estimates that 60% of today’s jobs did not exist in 1940.10 Every prior automation wave, from ATMs to spreadsheets to medical imaging, has triggered a version of the Jevons Paradox: making work cheaper expands demand enough to offset the labor it saves.

The strongest bear case is that AI’s cognitive breadth is unprecedented, and that is fair. But compute constraints, gradual adoption, and demographic tailwinds all point to a transition measured in years and decades, leaving labor markets time to adapt, as they have before.

Watching for Inflation

Consensus is AI is deflationary, but it’s likely more inflationary in the near term

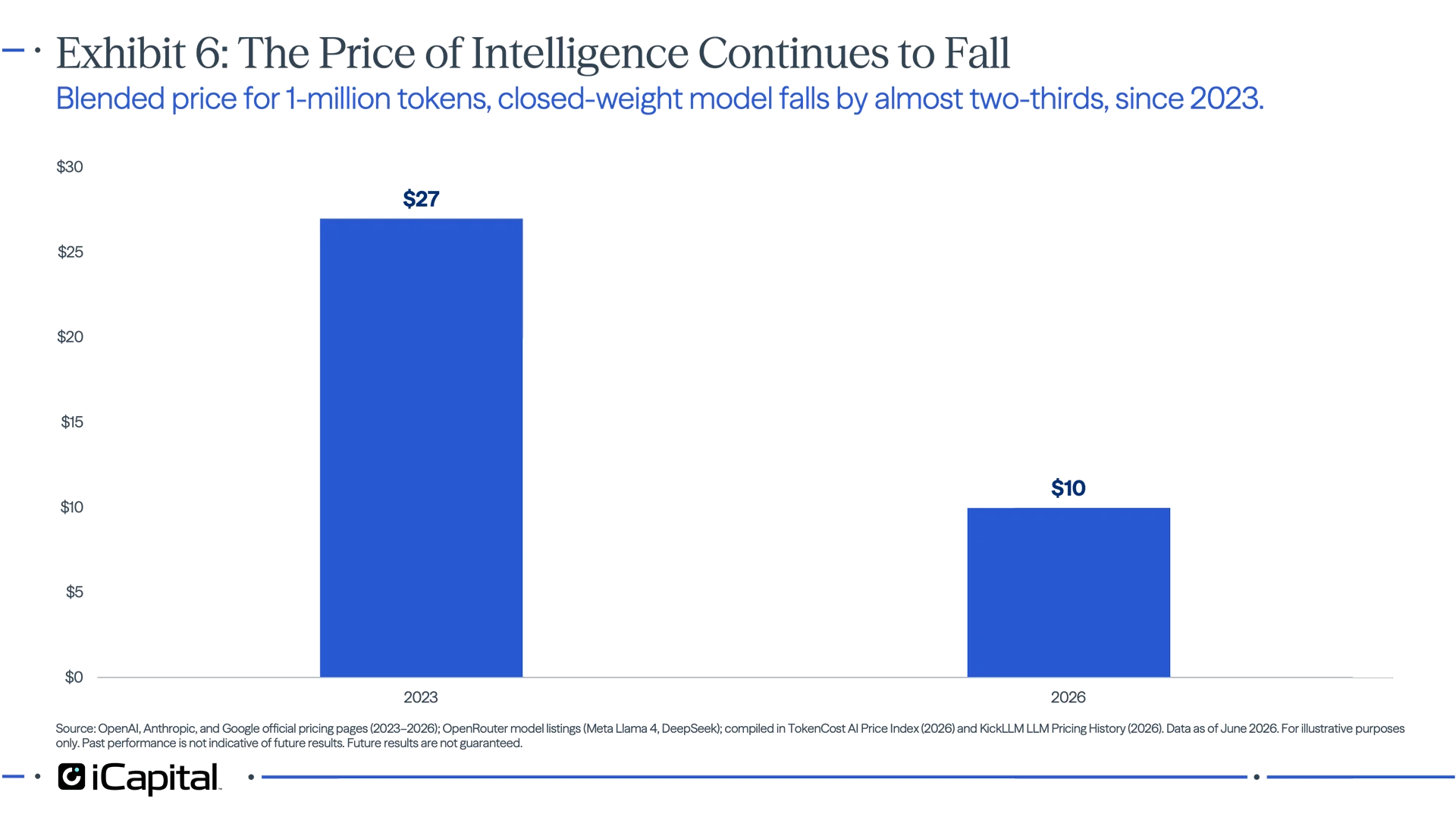

Corporate AI spending illustrates the Jevons Paradox. Even as per-token costs have fallen, enterprise AI spending has continued to surge, driven by wider adoption, newer models, and more complex use cases. While US frontier models cost roughly a third of their 2023 levels, token usage has scaled exponentially, with consumption measured in quadrillions (one thousand trillion).11 With adoption accelerating, hyperscalers are making record capex investments to meet AI and compute demand.

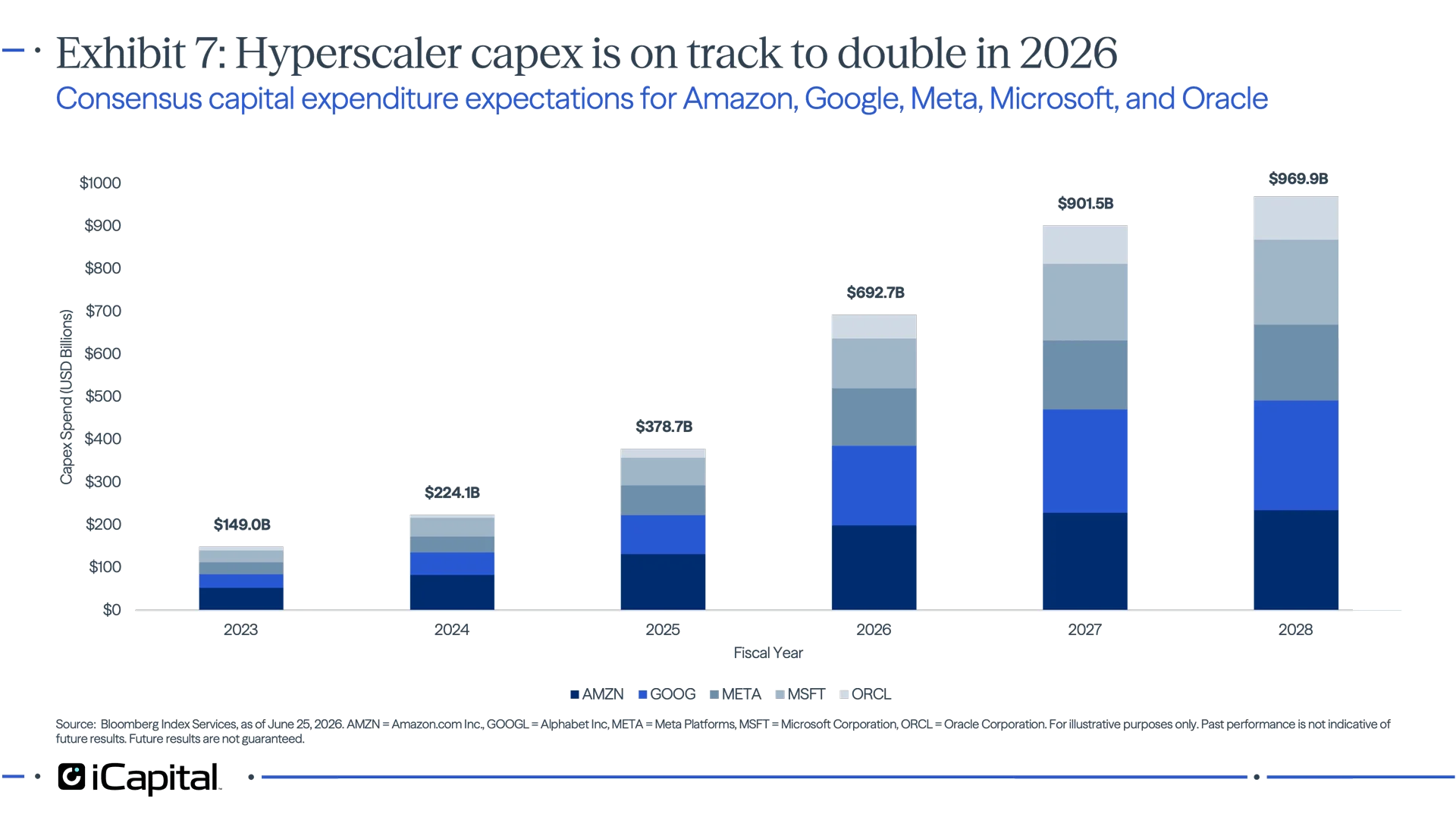

The demand shock

The demand shock

Hyperscaler capex could approach $800 billion in 2026, roughly double 2025 levels (Exhibit 7). Broader spending across computers and peripherals, data centers, software and R&D topped $2 trillion, or 6.5% of GDP, in 2025.12 Gartner expects global data center electricity consumption to rise more than 50% between 2025 and 2027.13

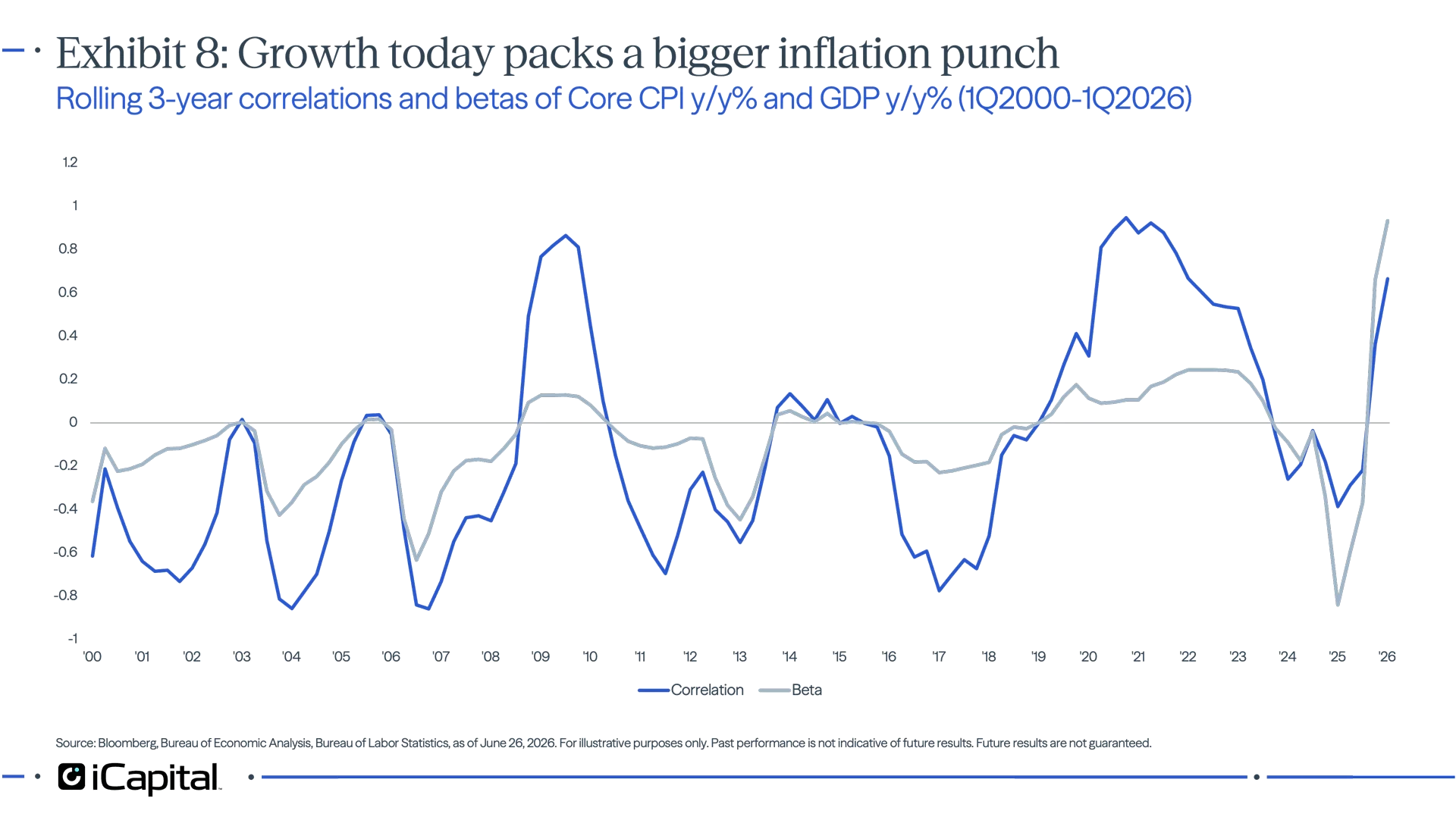

That surge is landing just as inflation has become unusually sensitive to growth. The rolling three-year sensitivity (beta) of inflation (Core CPI y/y%) to GDP growth y/y% sits at a multi-decade high, meaning each additional unit of growth now feeds through to more inflation than at almost any point in the past 20 years (Exhibit 8). Broad supply bottlenecks are the likely driver of this elevated correlation.

That surge is landing just as inflation has become unusually sensitive to growth. The rolling three-year sensitivity (beta) of inflation (Core CPI y/y%) to GDP growth y/y% sits at a multi-decade high, meaning each additional unit of growth now feeds through to more inflation than at almost any point in the past 20 years (Exhibit 8). Broad supply bottlenecks are the likely driver of this elevated correlation.

Supply shortages are amplifying prices

Supply shortages are amplifying prices

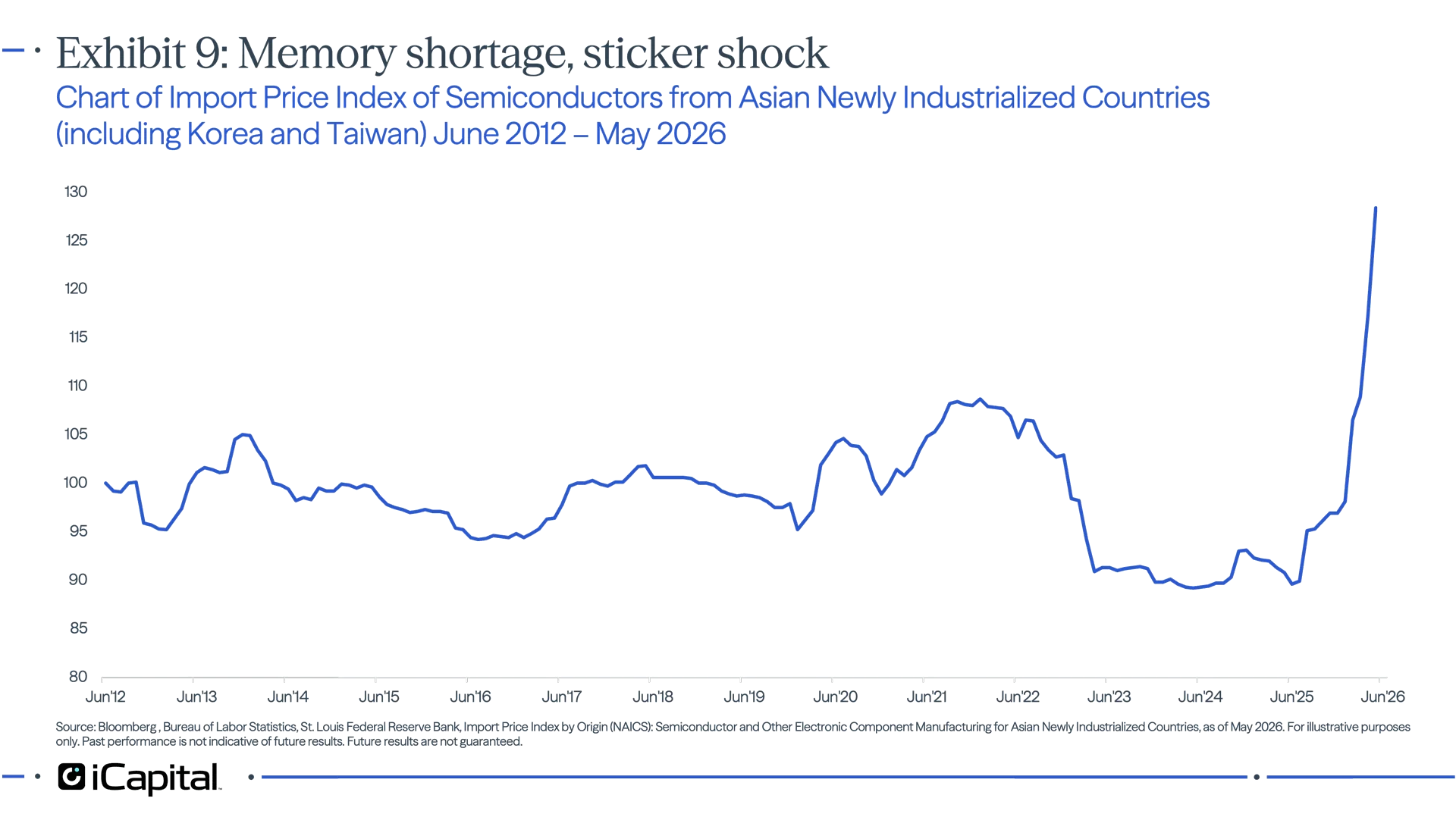

The US Producer Price Index (PPI) rose 6.5% YoY in May 2026, the fastest pace since November 2022, with AI-related input costs contributing.14 AI training’s appetite for memory and storage has pushed up semiconductor prices in Asian newly industrialized countries—home to Taiwan Semiconductor, Samsung and SK Hynix—up more than 40% in less than a year.15 The pass-through is broadening to the consumer. Dell has announced 10–30% price increases on commercial lines.16 Microsoft raised Surface prices by roughly 25%.17 Lenovo has expired existing PC quotes, and even Apple—often viewed as insulated from component cost swings—has raised prices, citing the memory shortage.

Data center electricity consumption raises retail electricity bills

Data center electricity consumption raises retail electricity bills

This AI driven inflation dynamic is also visible in electricity markets, particularly in wholesale capacity markets where grid operators contract years in advance to secure supply. PJM Interconnection, serving data-center-heavy states across the Mid-Atlantic and Midwest and powering roughly 67 million Americans, has reported future capacity auctions hitting price ceilings amid strong demand.18 The grid’s Independent Market Monitor estimates that data center load growth alone is responsible for $23.1 billion in new wholesale capacity costs over the next three delivery years — which PJM expects to translate into retail electricity bill increases of roughly 1.5–5% across its 13-state footprint.19 New demand, overwhelmingly from data centers, is being added far faster than new power plants can be built, leaving PJM with reserve margins at historic lows and little buffer for additional load. 20 21

The strain is extending upstream: Siemens Energy’s CEO recently noted that customers are paying reservation fees just to secure gas turbine production slots.22 While geopolitical risks have been the primary driver of recent energy prices, AI-driven electricity demand is likely creating a persistent floor under power costs.

Policymakers’ dilemma

For policymakers, the challenge is not obvious at first glance: inflation and growth are becoming harder to read. AI is already distorting the data the Fed relies on, pushing inflation higher before productivity gains are fully visible, and masking labor scarcity that is structural, not cyclical. That leaves the margin for error uncomfortably thin. Tighten policy too aggressively and you risk leaning against an investment cycle that may ultimately lift capacity. Ease too soon and the inflation embedded in that same investment becomes harder to contain. The paradox of the AI economy is that its benefits are long term, but its pressures are immediate. The Fed will have to act before it can fully measure either.

- International Monetary Fund, Demographic Decline, September 2024.

- Congressional Budget Office, An Update to the Demographic Outlook, 2025 to 2055, September 2025.

- Deloitte and The Manufacturing Institute, Taking Charge: Manufacturers Support Growth with Active Workforce Strategies, April 2024.

- Congressional Budget Office, An Update to the Demographic Outlook, 2025 to 2055, September 2025.

- International Federation of Robotics, Robot Density Surges in Europe, Asia, and Americas, April 8, 2026.

- Yahoo Finance, Amazon Has Over 1.56 Million Workers and 1 Million Robots. A Historic Robot vs. Human Contest Dropped a Hint on What Might Come Next, May 21, 2026.

- Martha Gimbel, Molly Kinder, Joshua Kendall and Maddie Lee, Evaluating the Impact of AI on the Labor Market: Current State of Affairs, The Budget Lab at Yale, October 1, 2025.

- Wells Fargo Investment Strategy, The New L(ai)bor Market: Fear vs. Reality, May 13, 2026.

- US Census Bureau, Business Formation Statistics, 2025.

- Quarterly Journal of Economics, New Frontiers: The Origins and Content of New Work, 1940–2018, August 2024.

- OpenAI, Anthropic, and Google official pricing pages (2023–2026); OpenRouter model listings (Meta Llama 4, DeepSeek); compiled in TokenCost AI Price Index (2026) and KickLLM LLM Pricing History (2026).

- U.S. Bureau of Economic Analysis, National Income and Product Accounts, 2025

- Gartner, Gartner Says Data Center Electricity Consumption to Grow 26% in 2026, June 10, 2026.

- U.S. Bureau of Labor Statistics, Producer Price Indexes – May 2026, June 11, 2026.

- S&P Global Market Intelligence, AI Memory Boom Squeezes Legacy DRAM Supply, Pushing Prices Higher, January 28, 2026

- TrendForce, Dell Reportedly Plans 10–30% Hikes on Commercial PCs From Dec. 17 as Memory Prices Surge, December 15, 2025.

- MacRumors, Microsoft Raises Prices for All Surface PCs, Making Them More Expensive Than Equivalent Macs, April 14, 2026.

- Monitoring Analytics, LLC, 2026 Quarterly State of the Market Report for PJM: January through March, 2026.

- Monitoring Analytics, LLC, 2026 Quarterly State of the Market Report for PJM: January through March, 2026.

Ibid. - Erin Donohue, PJM 2026/2027 Capacity Auction Results, Enel North America, July 24, 2025.

- Bloomberg, AI Boom Has European Buyers Paying Extra to Secure Gas Turbines, June 12, 2026.

INDEX DEFINITIONS

U.S. Producer Price Index: The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output. The prices included in the PPI are from the first commercial transaction for many products and some services.

U.S. Consumer Price Index: is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. Percent changes in the price index measure the inflation rate between any two time periods. Index captures roughly 88 percent of the total population, accounting for wage earners, clerical workers, technical workers, self-employed, short-term workers, unemployed, retirees, and those not in the labor force.

Import Price Index: The International Price Program (IPP) produces Import/Export Price Indexes (MXP) containing data on changes in the prices of nonmilitary goods and services traded between the U.S. and the rest of the world.

S&P 500 Index: The S&P 500 is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 of the top companies in leading industries of the U.S. economy and covers approximately 80% of available market capitalization.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. ("iCapital Network") or one of its affiliates (iCapital Network together with its affiliates, "iCapital"). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. "iCapital" and "iCapital Network" are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

© 2026 Institutional Capital Network, Inc. All Rights Reserved.