Key takeaways:

- Set client expectations appropriately: Venture capital is front-loaded in risk and back-loaded in returns, and value creation is concentrated in a small number of later-stage exits.

- Tilt toward smaller funds for return potential: Sub-$350 million funds have meaningfully outperformed larger vehicles on both internal rate of return (IRR) and total value to paid-in capital (TVPI).2

- Use larger funds for access: Larger funds provide exposure to scaled AI leaders and late-stage opportunities but face mathematical constraints that compress return multiples.

- Prioritize manager selection: Performance dispersion is wide, and access to top-tier managers is critical.

- Commit consistently to capture multiple vintage years: Venture outcomes are driven by a small number of investments, and predicting which vintages will outperform is challenging.

Investing in venture capital

Venture capital finances early-stage companies with the potential for rapid growth and significant value creation. Early-stage investing, typically Series A or Series B, carries more uncertainty because business models are still being proven, but it also offers greater potential upside. One reason is ownership: lead investors can often secure equity stakes of roughly 20%.3

Later-stage investing, by contrast, offers more visibility into product-market fit, revenue traction, and business durability, but usually with lower return potential. Competition for these deals can drive valuations higher and ownership stakes lower. That tradeoff is central to capturing power-law outcomes: larger equity positions in successful companies translate into greater upside.

The challenge of scale

The largest venture firms are highly sought after because of their capital base and long track records. But scale can work against performance. By the law of large numbers, bigger funds need multiple exceptional outcomes just to return invested capital, making it harder to generate outsized results.

In larger, later-stage funds, the math becomes more demanding. A $10 million investment that returns 10x has limited impact on a $1 billion fund, meaning a fund of this size requires multiple large wins to generate scaled returns. And because the largest venture funds can now exceed $10 billion, they must put more capital to work across more companies. Those larger check sizes usually target more mature businesses, where ownership stakes tend to be smaller and upside more constrained.

Smaller funds, by contrast, need fewer successful investments to generate strong returns. A $100 million fund with 40 investments can reach upper-quartile performance with just one or two major winners. The performance data reflects that advantage: funds under $249 million have generated a median IRR of 36%, versus 24% for funds above $250 million.4

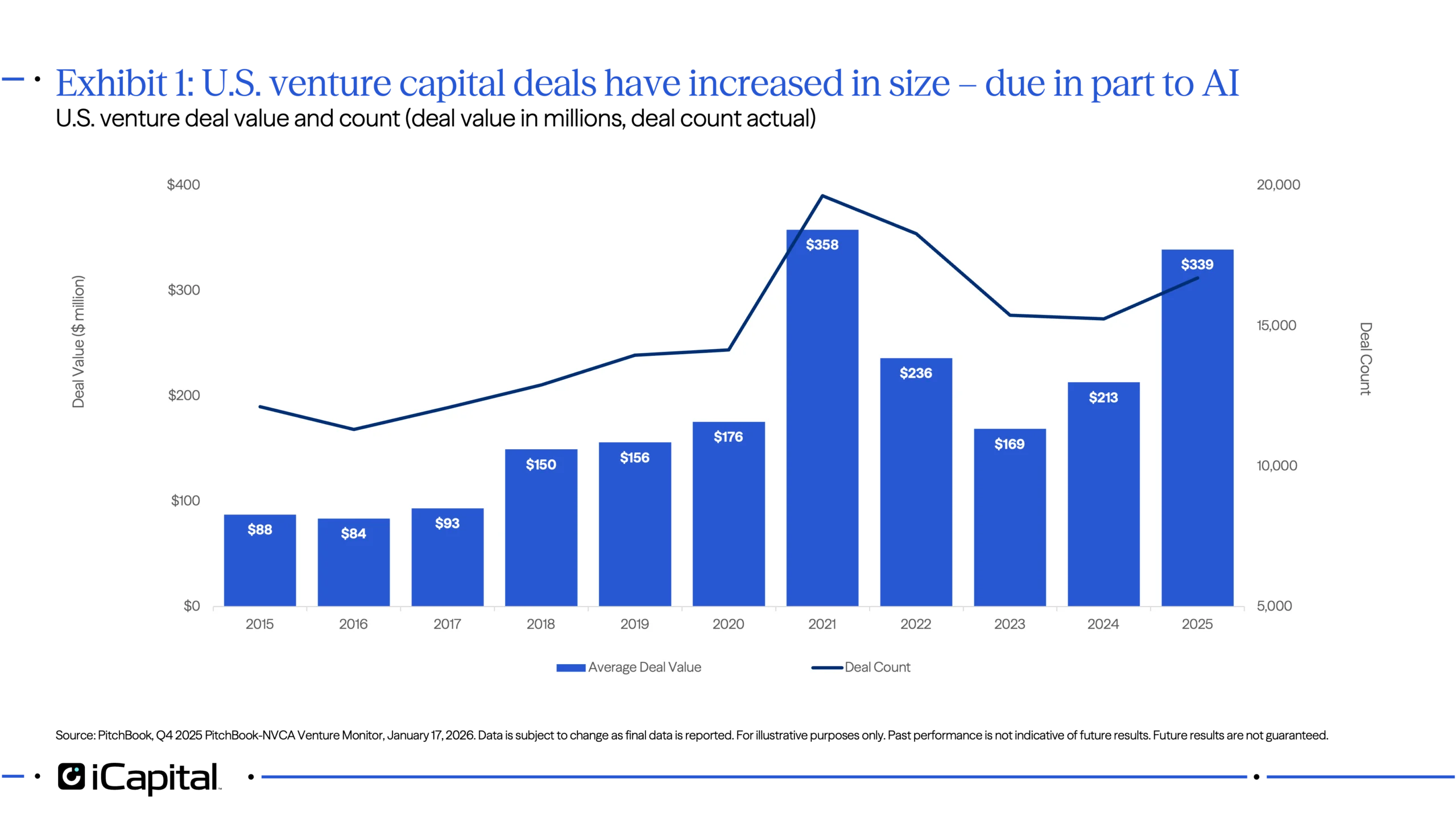

The AI tailwind

The surge in AI-related companies has arguably overshadowed some of these dynamics. In 2025, AI companies accounted for about 65% of total U.S. venture deal value, much of it concentrated in a small number of mega -rounds.5 That expanding opportunity set gives large funds more room to deploy capital, while rich valuations and the prospect of AI-driven hypergrowth have pushed deal sizes higher.

AI is also intensifying the power-law dynamics that define venture capital. This cycle’s biggest winners—companies such as SpaceX, Anthropic, and OpenAI—are so much larger than prior outliers that they are concentrating an even greater share of industry returns in a handful of outcomes. In 2025, mega-deals (rounds over $100 million) made up just 3.2% of deals but 67% of total deal value.6 These companies also have more venture rounds than prior cycles given their elongated pathways to IPO—in 2025, the venture growth stage deployed $126.9 billion across 937 deals.7 While further series of capital raises provides entry points for investment, skyrocketing valuations and smaller portions of equity captured result in difficulty generating an outsized return.

Accessing venture capital

Accessing venture capital

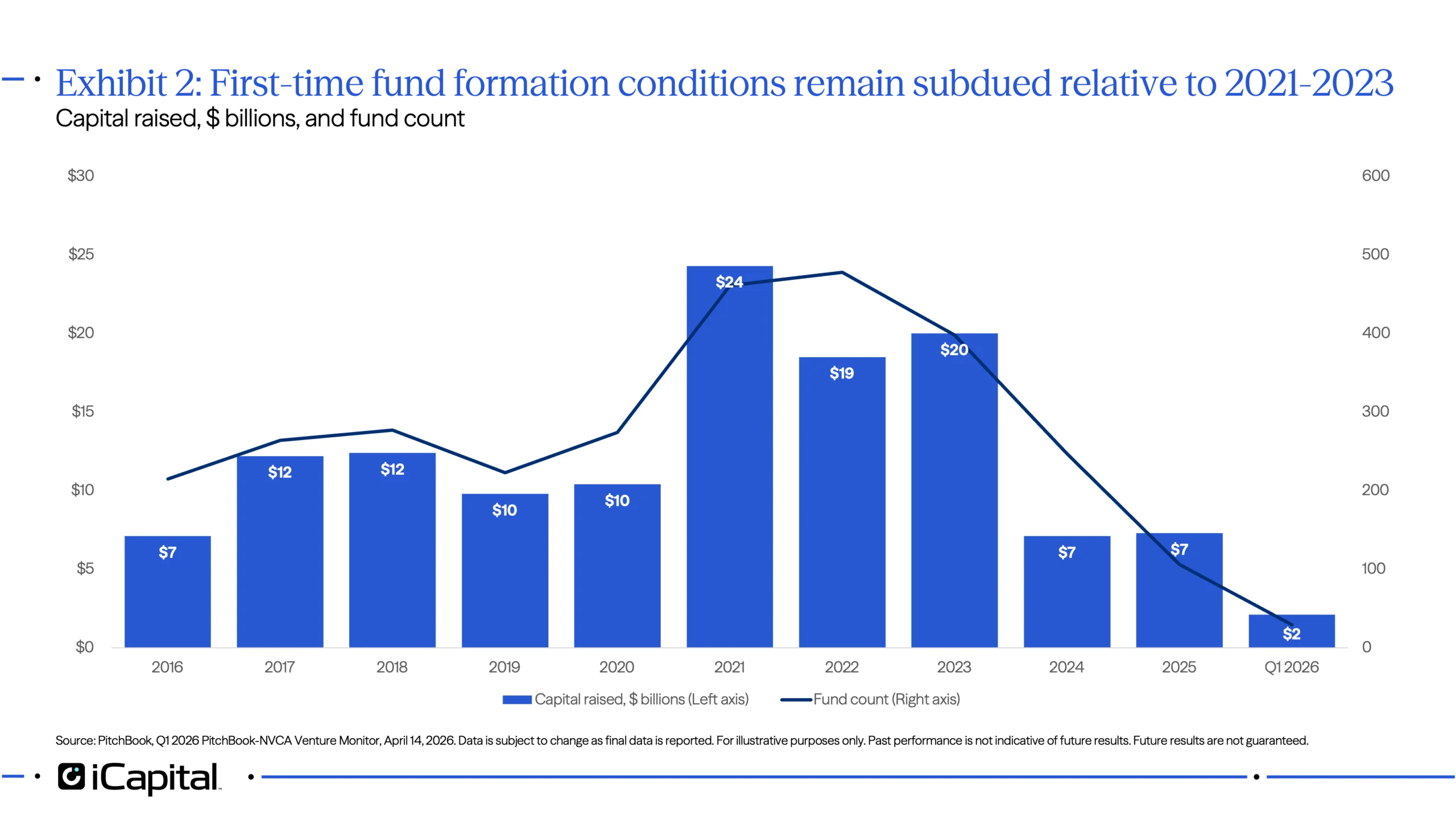

Access to venture capital, especially smaller funds with potentially higher return profiles, remains limited. First-time fund formation fell to 101 funds in 2025, the fewest since 2011 and nearly 78% below the 457 launched in 2021.8 At the same time, the top 10 funds captured 33% of all venture fundraising, up from 13% in 2021, further concentrating capital among larger firms.9 For advisors, that scarcity reinforces the value of relationships with emerging managers and curated emerging manager platforms. These channels can provide exposure to smaller, more focused strategies while helping reduce the sourcing and due diligence burden on individual practices.

Manager selection is even more critical in venture capital

Manager selection is even more critical in venture capital

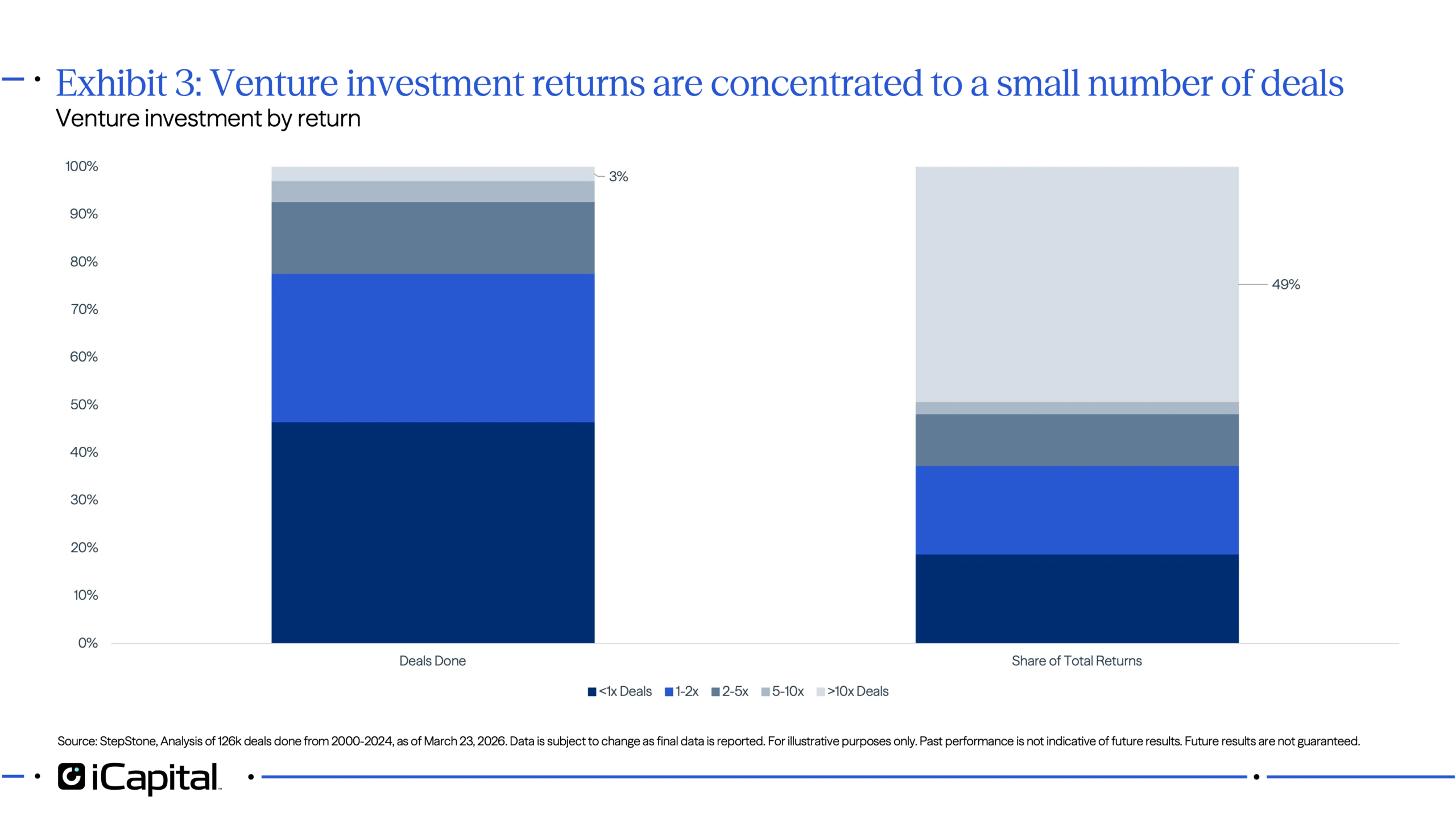

Manager selection matters more in venture than in any other private markets asset class. Roughly 3% of deals have generated nearly half of total returns, while almost half of deals were done at less than 1x (Exhibit 3). The gap between top- and bottom-quartile managers is also wider in venture than in any other alternatives category. Taken together, the data on fund size, ownership, and power-law dynamics point to the same conclusion: manager selection is critical.

Advisor due diligence should emphasize a manager’s ability to identify and capture outlier outcomes, not just produce modest gains, and should also assess:

Advisor due diligence should emphasize a manager’s ability to identify and capture outlier outcomes, not just produce modest gains, and should also assess:

- Sourcing networks

- Ownership discipline

- Portfolio construction philosophy

- Sector specialization

Trying to time venture commitments can be counterproductive. Instead, advisors should follow a disciplined pacing strategy by committing capital annually across multiple vintage years. That approach improves the odds of participating in the few vintages that drive most long-term returns, while also helping smooth the J-curve and create a more predictable distribution profile over time.

- StepStone, Analysis of 126k deals done from 2000-2024, as of March 23, 2026.

- Sante Ventures, Why Venture Capital Does Not Scale, November 2023.

- Carta, Capital Structure: A founder’s guide to ownership, February 12, 2026.

- PitchBook Benchmark Data as of 2025 vintage year for funds located in North America, accessed on May 26, 2026. IRR for funds under $249 million represent median calculation of eight constituent funds and IRR for funds over $250 million represent median calculation of nine constituent funds.

- NVCA 2026 Yearbook, as of April 9, 2026.

- NVCA 2026 Yearbook, as of April 9, 2026.

- NVCA 2026 Yearbook, as of April 9, 2026.

- NVCA 2026 Yearbook, as of April 9, 2026.

- NVCA 2026 Yearbook, as of April 9, 2026.

IMPORTANT INFORMATION

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax, and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

iCapital Markets LLC operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital Markets LLC generally earns revenue based on the volume of transactions that take place in these products and would benefit from an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection, or forecast on the economy, stock market, bond market, or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third-party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Securities products and services are offered by iCapital Markets LLC, an SEC-registered broker-dealer, member FINRA and SIPC, and an affiliate of iCapital, Inc. and Institutional Capital Network, Inc. These registrations and memberships in no way imply that the SEC, FINRA, or SIPC have endorsed any of the entities, products, or services discussed herein. Annuities and insurance services are provided by iCapital Annuities and Insurance Services LLC, an affiliate of iCapital, Inc. “iCapital” and “iCapital Network” are registered trademarks of Institutional Capital Network, Inc. Additional information is available upon request.

©2026 Institutional Capital Network, Inc. All Rights Reserved.