The iCapital Advisor Survey 2025 reveals a notable shift in investment practices across the Gulf Cooperation Council (GCC), where advisors are increasingly integrating alternative investments into client portfolios. Drawing on responses from 50 senior financial professionals in Kuwait, Qatar, Saudi Arabia, and United Arab Emirates, each managing at least $400 million in assets and primarily serving individual and family clients, the survey offers a focused view into a market both ambitious and nuanced in its approach to private market investing.

Client interest in alternatives has grown steadily over the past two years, with a particular emphasis on private equity, private credit, and real estate. Respondents cited return potential, inflation hedging, and portfolio diversification, particularly into emerging sectors such as clean energy and infrastructure, as the primary motivations driving this trend. Nearly all advisors reported being either “very” or “somewhat” knowledgeable about alternatives, and three-quarters expect clients to hold 11–15% of their portfolios in evergreen strategies over the next two years.

Client Interest in Alternatives Holds Strong—With Signs of Growth

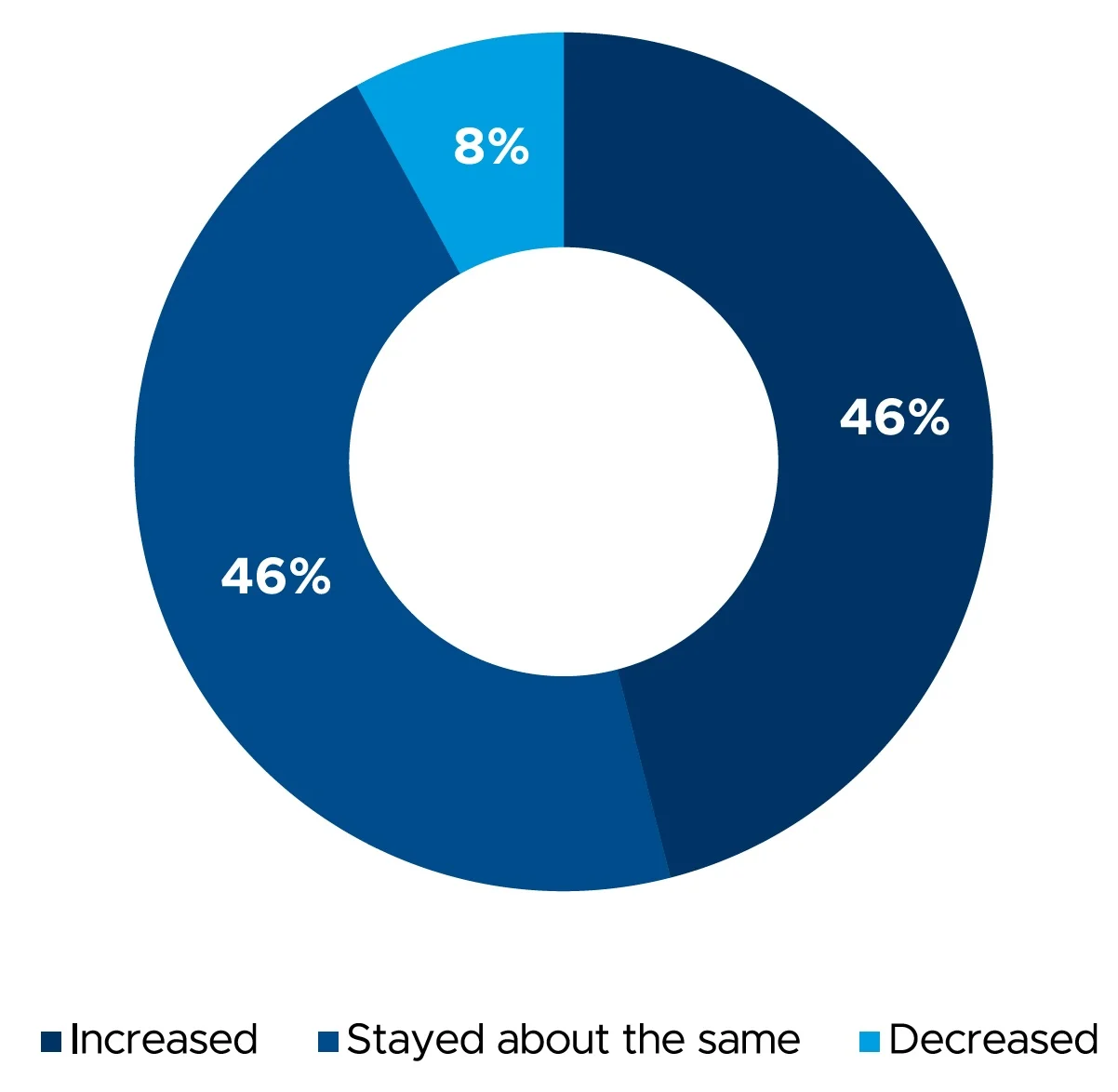

Compared to two years ago, has client interest increased in alternative investments?

Nearly half of GCC advisors (46%) report increased client interest in alternatives compared to two years ago, while another 46% say interest has held steady. Only 8% see a decline, reinforcing that alternatives remain a core focus. This stability—paired with growth signals—suggests alternatives are moving from opportunistic plays to a permanent fixture in client portfolios, challenging firms to rethink how they deliver access and education at scale.

Yet while the enthusiasm is clear, structural and operational constraints persist. The most significant challenges to integrating alternatives include limited access to institutional-grade products, compliance and regulatory hurdles, and a lack of accessible model portfolios tailored to alternatives. These concerns are compounded by frustrations with due diligence and the high capital commitment often required for private assets; factors that have led some advisors to scale back in areas like real estate.

Portfolio construction practices across the region are varied and hybrid in nature. Many firms combine in-house research with investment team-led model portfolios or third-party offerings, reflecting the need for adaptable tools and workflows. Advisors also highlighted risk management, macroeconomic factors, and the pursuit of stable income as playing key roles in shaping portfolio design.

Looking ahead, the survey highlighted that advisors in the GCC are calling out for greater operational efficiency and improved data infrastructure. Standardized performance reporting, enhanced risk analytics, and automated onboarding processes are seen as essential improvements. The need for better education, particularly around implementation and regulation, remains an ongoing theme.

The survey suggests a region well-positioned for growth in alternative investing, but one that requires targeted support to overcome persistent operational friction. Firms that invest in flexible, scalable technology or partner with financial technology providers offering such solutions—and proactively address key advisor pain points—will be best equipped to serve a maturing, and increasingly sophisticated client base.

The material herein has been provided to you for informational purposes only by Institutional Capital Network, Inc. (“iCapital Network”) or one of its affiliates (iCapital Network together with its affiliates, “iCapital”). This material is the property of iCapital and may not be shared without the written permission of iCapital. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of iCapital.

This material is provided for informational purposes only and is not intended as, and may not be relied on in any manner as, legal, tax or investment advice, a recommendation, or as an offer or solicitation to buy or sell any security, financial product or instrument, or otherwise to participate in any particular trading strategy. This material does not intend to address the financial objectives, situation, or specific needs of any individual investor. You should consult your personal accounting, tax and legal advisors to understand the implications of any investment specific to your personal financial situation.

ALTERNATIVE INVESTMENTS ARE CONSIDERED COMPLEX PRODUCTS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. Prospective investors should be aware that an investment in an alternative investment is speculative and involves a high degree of risk. Alternative Investments often engage in leveraging and other speculative investment practices that may increase the risk of investment loss; can be highly illiquid; may not be required to provide periodic pricing or valuation information to investors; may involve complex tax structures and delays in distributing important tax information; are not subject to the same regulatory requirements as mutual funds; and often charge high fees. There is no guarantee that an alternative investment will implement its investment strategy and/or achieve its objectives, generate profits, or avoid loss. An investment should only be considered by sophisticated investors who can afford to lose all or a substantial amount of their investment.

In certain jurisdictions, iCapital operates a platform that makes available financial products to financial professionals. In operating this platform, iCapital generally earns revenue based on the volume of transactions that take place in these products and would benefit by an increase in sales for these products.

The information contained herein is an opinion only, as of the date indicated, and should not be relied upon as the only important information available. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance. The information contained herein is subject to change, incomplete, and may include information and/or data obtained from third party sources that iCapital believes, but does not guarantee, to be accurate. iCapital considers this third-party data reliable, but does not represent that it is accurate, complete and/or up to date, and it should not be relied on as such. iCapital makes no representation as to the accuracy or completeness of this material and accepts no liability for losses arising from the use of the material presented. No representation or warranty is made by iCapital as to the reasonableness or completeness of such forward-looking statements or to any other financial information contained herein.

Certain products and services can only be offered by the appropriate entities and only in jurisdictions where they may be lawfully offered. Security products and services are offered through iCapital Markets LLC (a registered broker/dealer, member FINRA and SIPC), Institutional CN (Europe) – Empresa de Investimento, S.A. (registered with CMVM), iCapital Hong Kong Limited (licensed by SFC) and iCapital SG Pte. Ltd (licensed by MAS), all affiliates of iCapital. Registrations and memberships in no way imply that FINRA, SIPC, CMVM, SFC or MAS have endorsed any of the entities, products or services discussed herein. Subject to certain exceptions, iCapital Canada acts as the investment fund manager and portfolio manager of the funds domiciled in Canada and is registered as a portfolio manager, exempt market dealer and investment fund manager where required in the applicable Provinces and Territories of Canada. Additional information is available upon request.

© 2025 Institutional Capital Network, Inc. All Rights Reserved